🟪 Friday Stayin’ Alive Charts

Markets need a new narrative and for a brief moment this week it felt like a retro narrative of "stagflation" was coming back into style.

Byron Gilliam

April 26, 2024

Brought to you by:

"Four dollars??? You know what four dollars buys today? It don't even buy three dollars!"

Friday Stayin’ Alive Charts

Markets need a new narrative and for a brief moment this week it felt like a retro narrative of "stagflation" was coming back into style.

Yesterday, Treasury yields rose to year-to-date highs after economic growth (Q1 US GDP) came in lower than expected and inflation (Q1 PCE) came in higher than expected.

The unusual combination of rising bond yields and falling growth estimates had a distinctly worst-of-both-worlds feel reminiscent of the 1970s: In the first quarter of 1975, US prices rose 11% while real GDP fell 2.3%.

But this is not the Tony Manero 1970s when four dollars didn’t even buy three dollars.

Yes, mortgage rates are back up to 7.5%, car loans are back up to 8% and the Fed is likely to keep the fed fund rate higher for longer than anyone had expected.

But that is mostly because things are good, not bad.

For a reminder of how bad things were in the ‘70s, rewatch Saturday Night Fever this weekend — you've probably forgotten (or never even noticed) how soul-crushingly bleak it is.

For a reminder of how good things are now, listen to what companies are saying (and doing).

This week, Microsoft, Alphabet and Meta all announced both booming profits and — even better — booming investment plans. Microsoft and Alphabet reported capex up 66 and 91%, respectively, and Meta, as aggressively as they’ve already invested, said they’ll be investing "significantly more over the coming years."

Business for Big Tech is so good, in fact, that Alphabet announced a $70 billion buyback — in 2015, Alphabet did $75 billion of revenue.

2015 was nine years ago!

In total, US corporations are expected to buy back about $1 trillion of stock this year — so things can’t be too bad.

It’s not just Big Tech that’s both earning and spending, either.

General Motors raised guidance on better-than-expected demand for (very expensive) trucks and SUVs, Lockheed Martin said demand for new missiles, air-defense systems, and space hardware is (unfortunately) booming, and Nucor said it would be building new steel mills in West Virginia and North Carolina to meet rising domestic demand.

Consumers appear to be feeling flush, too: This morning’s PCE data showed personal spending growth near a two-year high.

So, demand is better than this week’s GDP report suggests — and supply might be better than the inflation data suggests, too.

Yesterday, Walmart’s US CEO said that they "are now seeing prices that are in line with where they were 12 months ago."

And Costco noted recently that prices of many staples are falling, even.

There was good news for non-Walmart and Costco shoppers this week, too: Crypto might finally be ready to undercut credit card fees, robots will undercut personal chefs and AI is making large-scale sculpture affordable.

Ok, fine — none of those things are likely to lower your monthly expenses any time soon.

But after this week’s data, the debate is now whether inflation settles at 2% or 3%, and that is hardly the existential threat that inflation posed in the 1970s when people were mostly concerned with — wait for it — staying alive.

So what should we be concerned with in 2024?

Let’s check the charts.

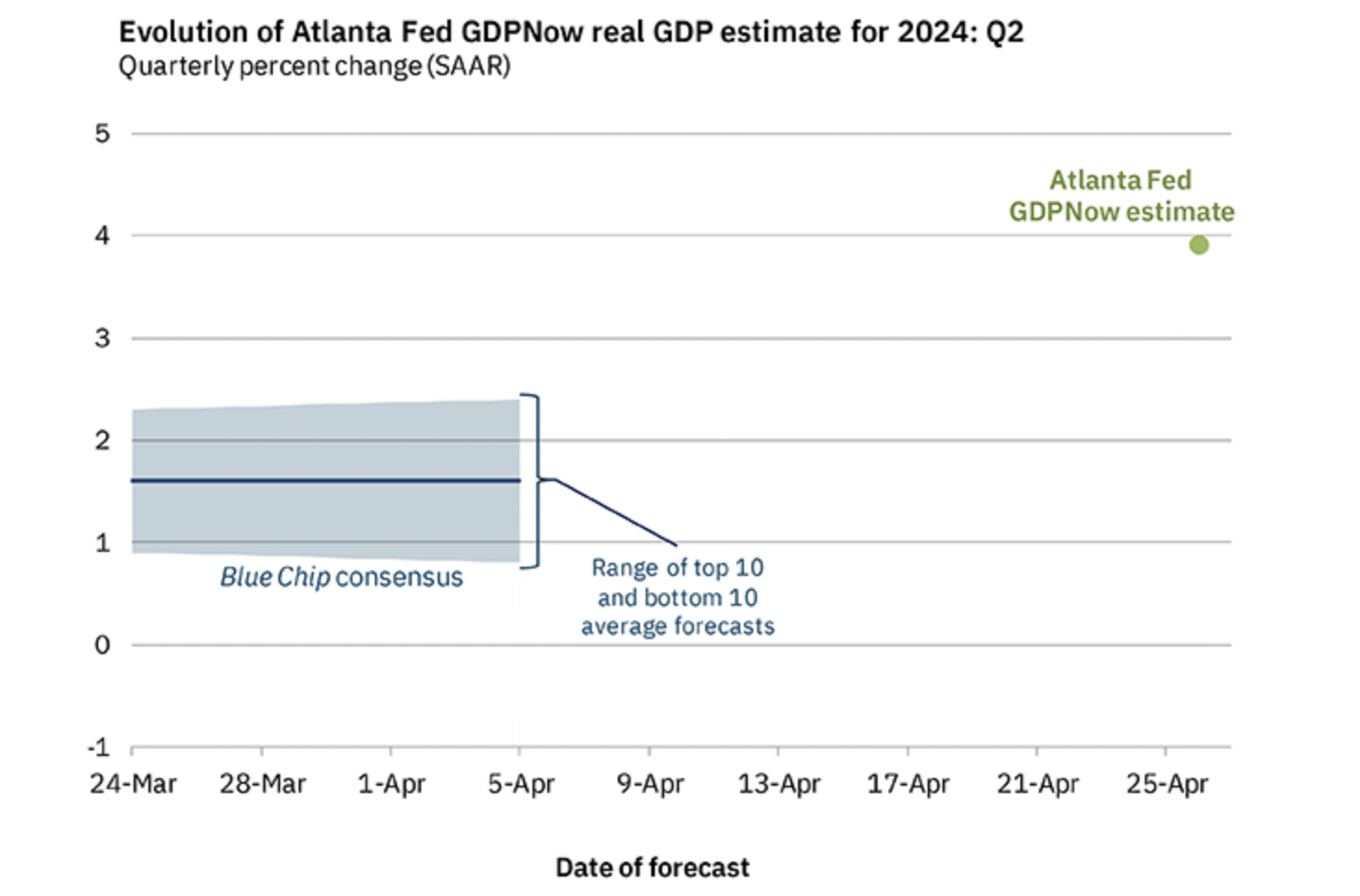

Taking the stag out of stagflation:

Q1 GDP was dragged down by volatile trade and inventories data, but the underlying trend (private demand up 3.1%) was solid, suggesting a quick bounce back in the current quarter. The Atlanta Fed’s first cut estimate for Q2 GDP is a robust 3.9%.

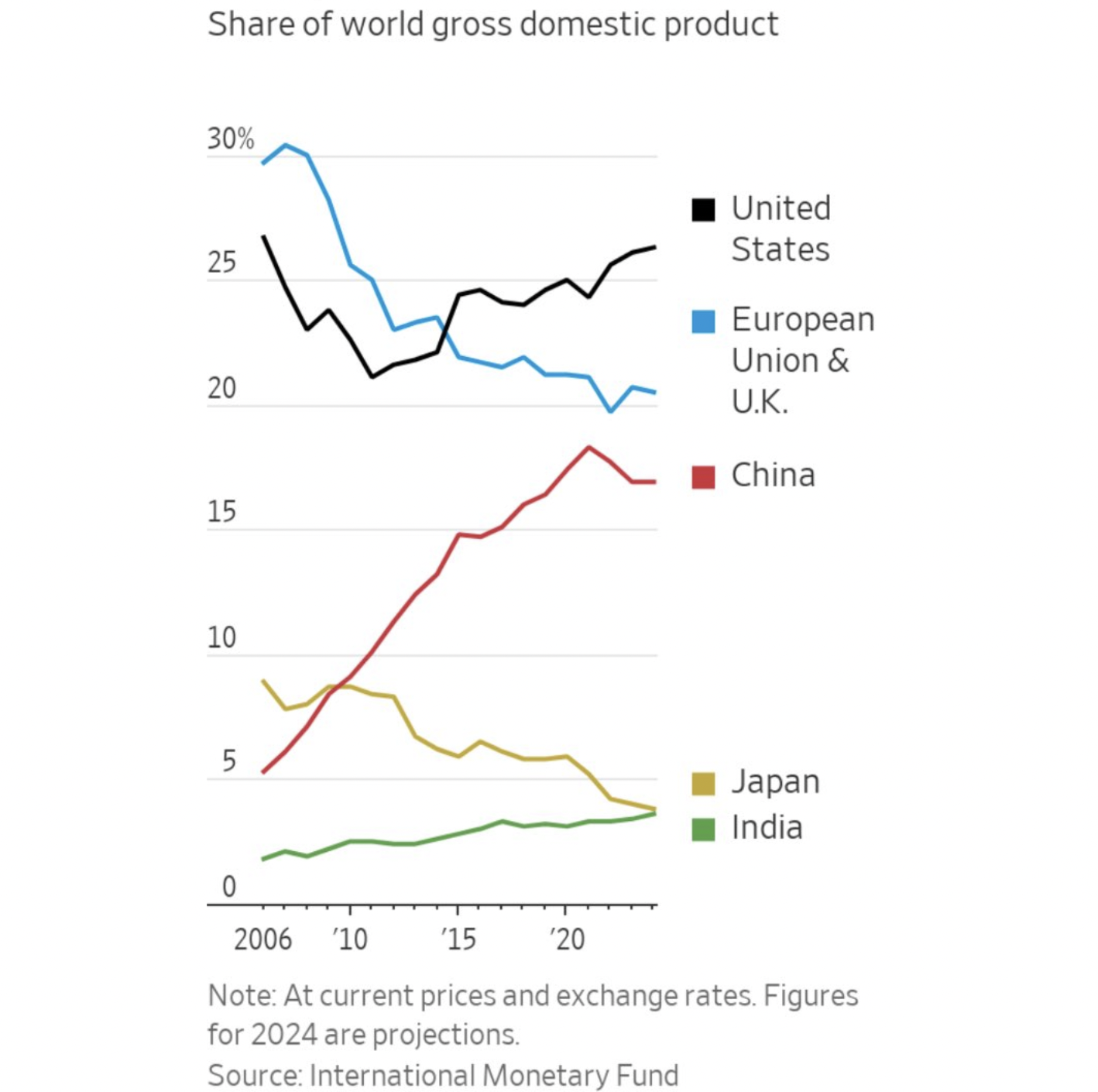

Best in the world?

The WSJ noted this week that, "This year, the US will account for 26.3% of the global gross domestic product, the highest in almost two decades."

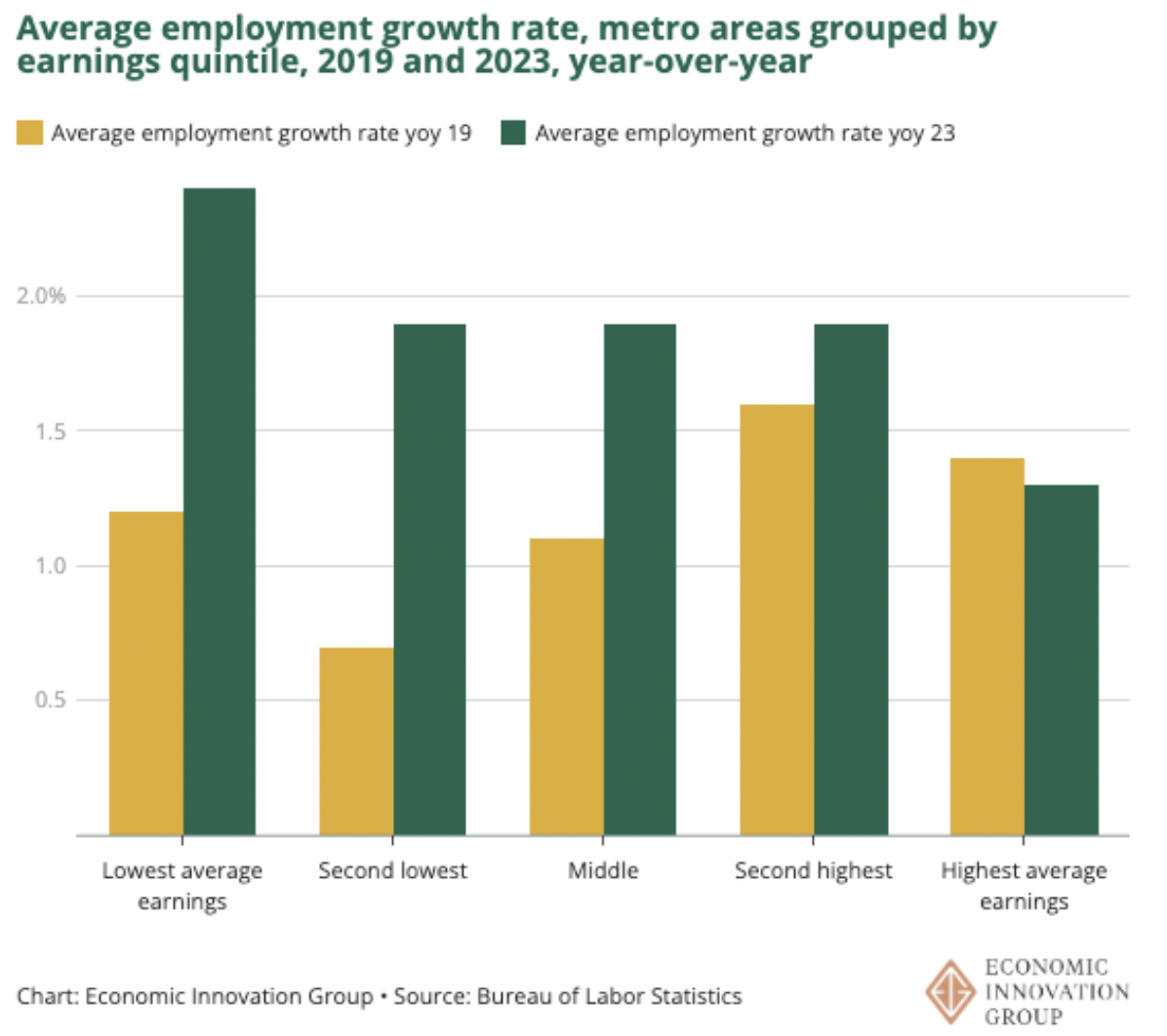

Jobs are going where they’re most needed:

Employment growth has been fastest in the areas of the US with the lowest average incomes.

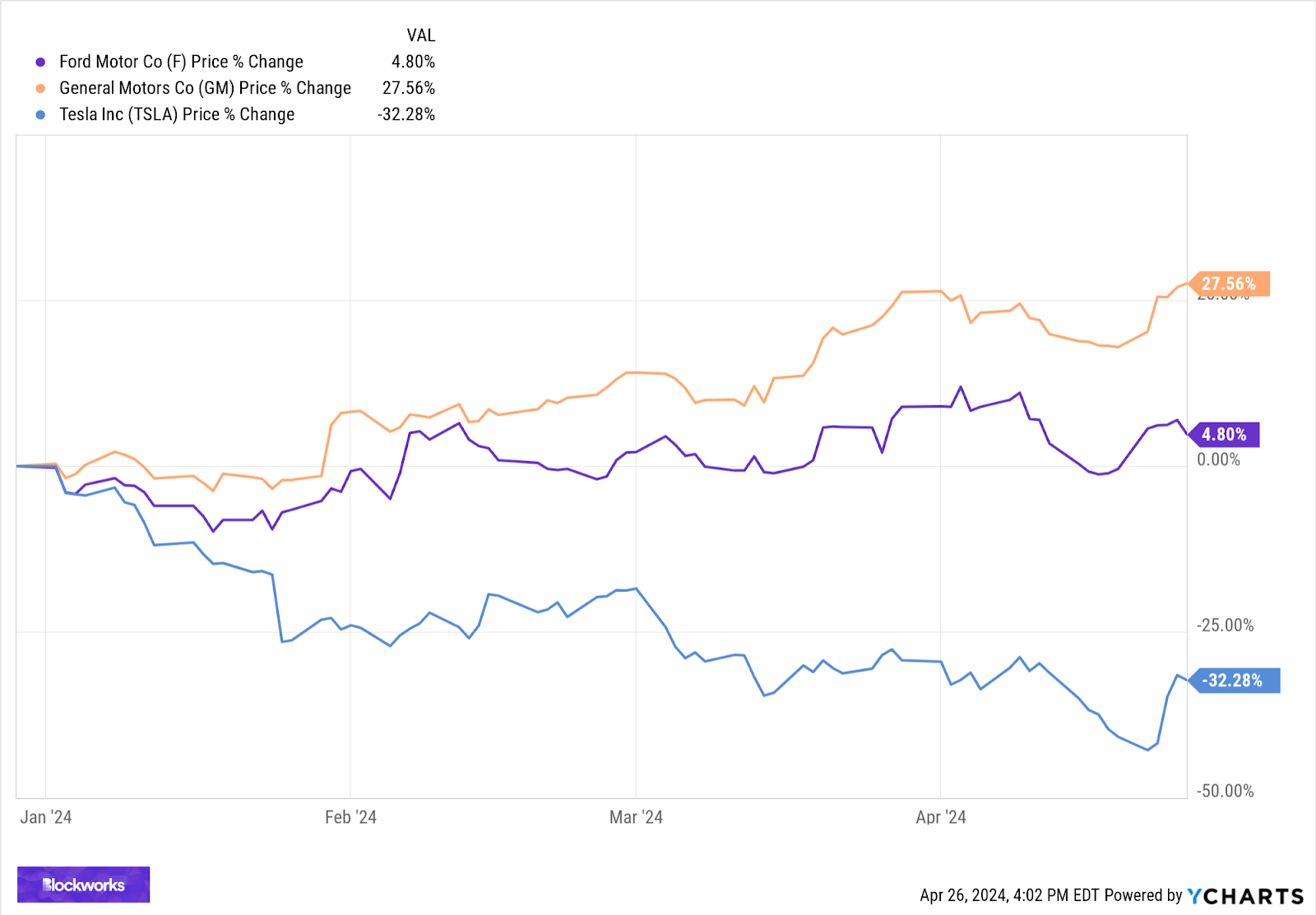

It’s not just a tech bubble:

Tesla shares are down 32% YTD vs. Ford up 5% and GM up 28%.

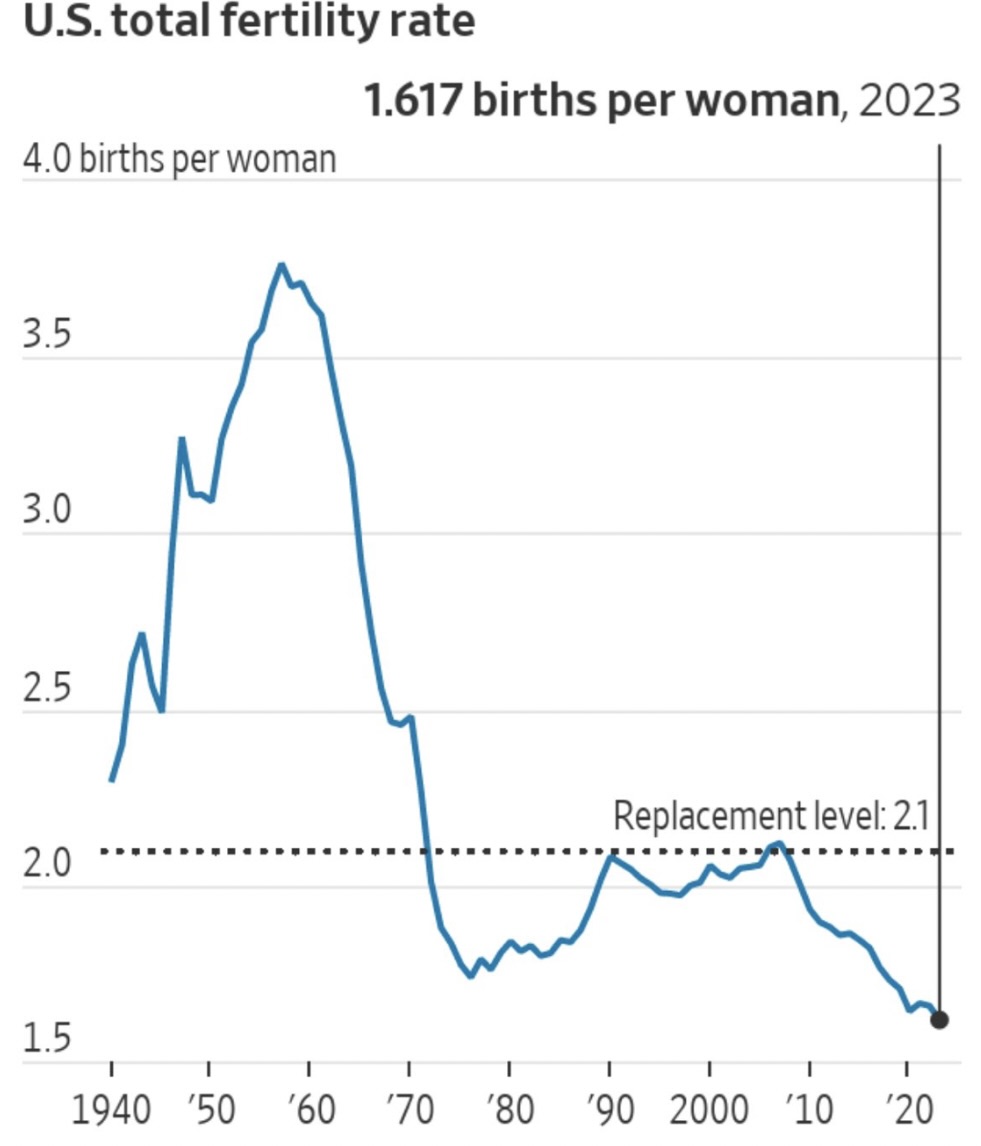

We’ll soon be begging robots to take the jobs:

The US fertility rate is down to 1.62 births per woman, the lowest rate since the government began tracking it in the 1930s.

Back on the radar:

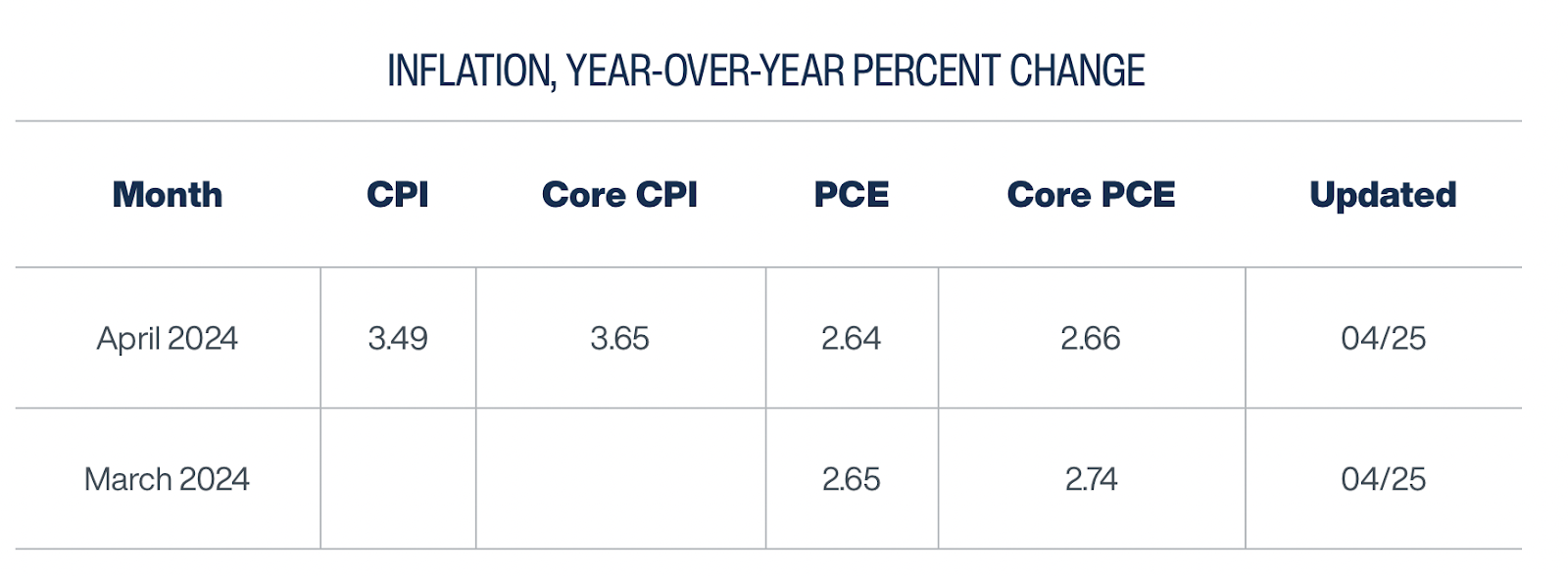

We might have to start paying attention to the Cleveland Fed’s InflationNow model again — they see Core CPI at an uncomfortably elevated 3.65% for April.

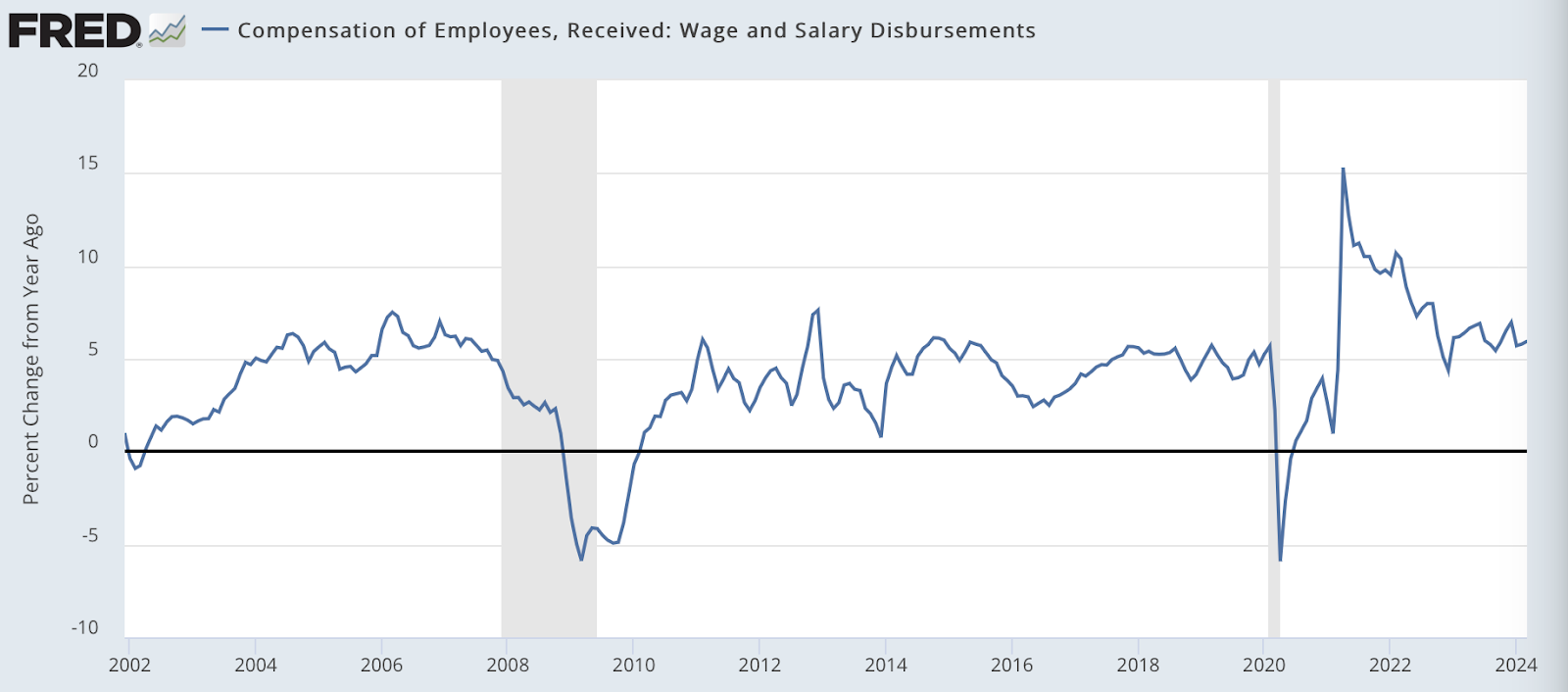

But wages still > prices:

Inflation may be plateauing at a higher level than we had expected, but wage growth is, too. Should we be annoyed that inflation is stuck at 3.5% when wage growth is stuck at nearly 6%?

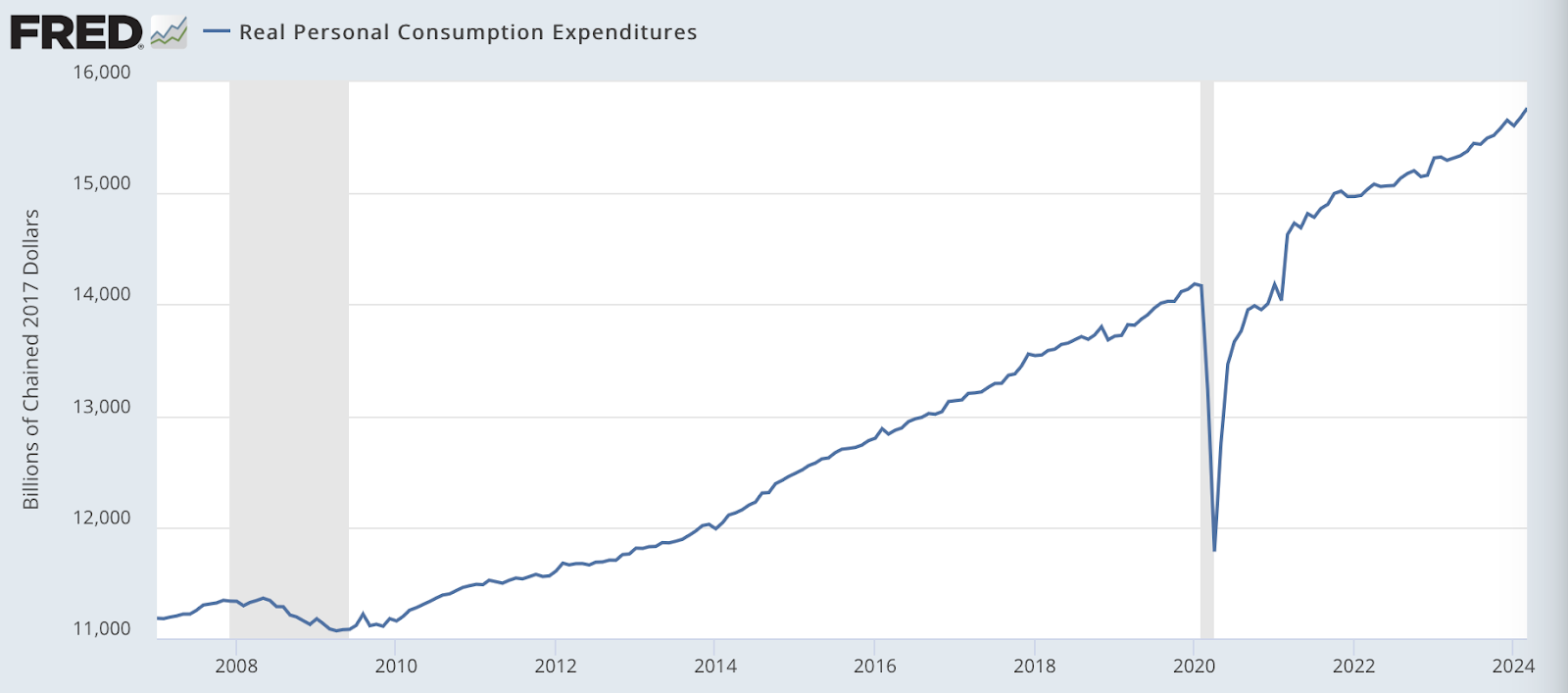

Spending inferno:

Even adjusted for inflation, our personal spending continues to trend relentlessly higher.

Yes, prices are rising faster than we’d like, but that’s more likely to lead to an "inflationary boom" reminiscent of the 1920s than a stagflation reminiscent of the 1970s.

That may not make you feel like dancing, but you have to admit that we’re doing far better than just stayin’ alive.

Have a great weekend, disco dancers.

Brought to you by:

Bitcoin is more than you think 🟧.

As Bitcoin enters its fully programmable era, L2s are leading the way for countless new use cases for the world’s most secure, decentralized and adopted cryptocurrency. Builders are writing the next chapter for Bitcoin with Stacks, the leading L2 for Bitcoin.

The Nakamoto Release, bringing Fast Blocks & Bitcoin Finality to Stacks, is currently being rolled out. Learn more about Stacks projects that are unlocking new use cases to activate the Bitcoin economy, like Zest, ALEX, and Xlink.

Crypto’s best use case? Buying goats on Twitter — Read

A bitcoin mining giant is ahead of schedule on its post-halving expansion — Read

Stocks bounce, cryptocurrencies trade sideways despite disappointing inflation data — Read

I bought an NFT and all I got was free coffee for a year — Read

Algorand courts Python devs in ‘seismic change’ — Read

The Rising Tide of Digital Asset Adoption in Asia

Join this webinar to learn from some of the top builders, investors, and market makers in crypto about what’s fueling the growth and trajectory of digital asset adoption in Asia.

How to Value L1s, L2s, and Crypto Assets

In this episode of Empire, Jason and Santi are joined by special guest Kyle Samani to dive deep into valuing L1 and L2 crypto assets. The conversation covers the importance of MEV as the primary value accrual mechanism rather than transaction fees, the challenges in standardizing valuations across different blockchain architectures, and the evolving fee market designs. They also discuss the true costs and benefits of token airdrops for bootstrapping ecosystems.

We just tagged more namespaces on @CelestiaOrg, and have now labeled 89% of the total data posted!

We noticed increased diversity in the data posted by sector. The Celestia userbase breaks down as:

- 34% DeFi

- 24% Gaming

- 23% General Purpose— Blockworks Research (@blockworksres)

Apr 26, 2024

Stripe is re-entering crypto.

I can't overstate how big this is.

Last time they tried crypto wasn't ready.

This time transactions are cheap & settlement fast.

They're not doing crypto for the hype. They're doing it because it makes sense for their business.

The most… twitter.com/i/web/status/1…

— RYAN SΞAN ADAMS - rsa.eth 🦄 (@RyanSAdams)

Apr 26, 2024

Coming out of our annual offsite and having reflected on reams of VC data, reminded that:

- Ownership matters

- 1-2 companies ultimately drive most of each fund’s returns. The exit magnitude of these 1-2 companies matters

- Ownership in these 1-2 companies is critical

- Being… twitter.com/i/web/status/1…— Amy Wu (@amytongwu)

Apr 26, 2024

recent research

Research

On May 4, 2024, Polygon developers met for the Polygon Protocol Governance Call (PPGC) #19 to discuss and finalize inclusions for the upcoming hard fork. The main focus was on PIP 22, PIP 36, PIP 30, and increasing the minimum gas price. With the inclusion list finalized, Polygon will target shipping these changes at the end of May or early June depending on testnet deployment timelines. The next PPGC meeting is tentatively scheduled for May 30 but may shift a week or two to align with the rollout.

by Boccaccio

/