Empire Newsletter: SEC still ‘protecting’ investors from yield

The current crop of ETF issuers could’ve only made it this far by promising not to stake any ETH they hoover up

Satheesh Sankaran/Shutterstock modified by Blockworks

Yield too scary

The SEC has finally thrown a bone to crypto and made room for spot ether ETFs on US markets.

But the regulator is still addicted to “protecting investors” from spooky crypto yield.

In fact, the current crop of ETF issuers could’ve only made it this far by promising not to stake any ETH they hoover up.

Ether is a different beast to bitcoin. While Bitcoin and Ethereum, the blockchains, are both censorship-resistant networks — which awards them a certain inherent value — bitcoin the currency is like gold and silver, in that it’s not a productive asset.

You buy, hold it and hope it goes up in price (or at least, retains more value than whatever currency you bought it with).

ETH, however, can be put to work at the protocol level by staking it to the blockchain.

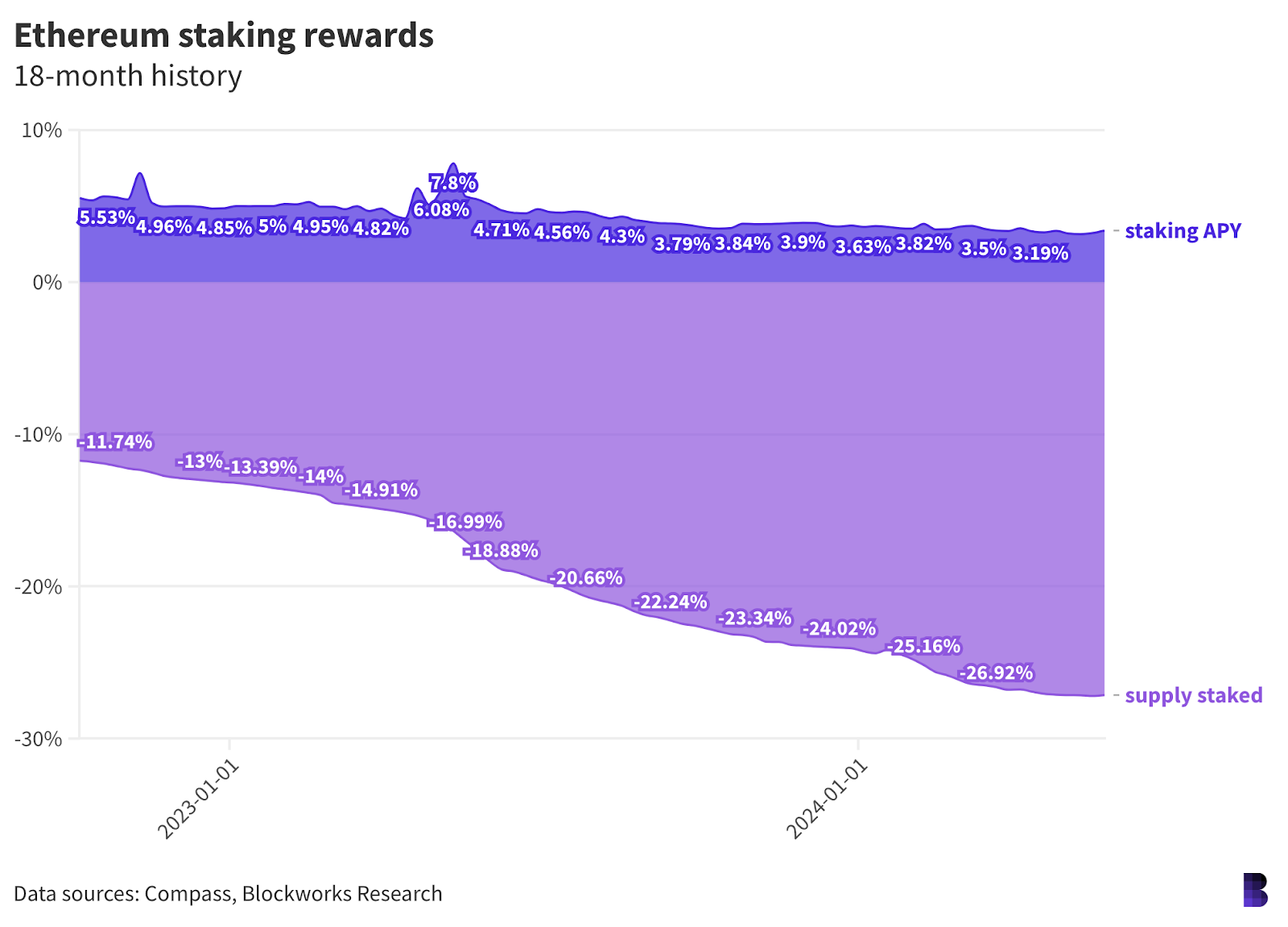

Staking directly takes running and maintaining a validator node, which requires some know-how (and a dedicated machine). The Ethereum network currently pays anyone who does about 3.4% APY.

That yield — staking rewards — is paid in ETH and varies depending on the number of validators and network activity.

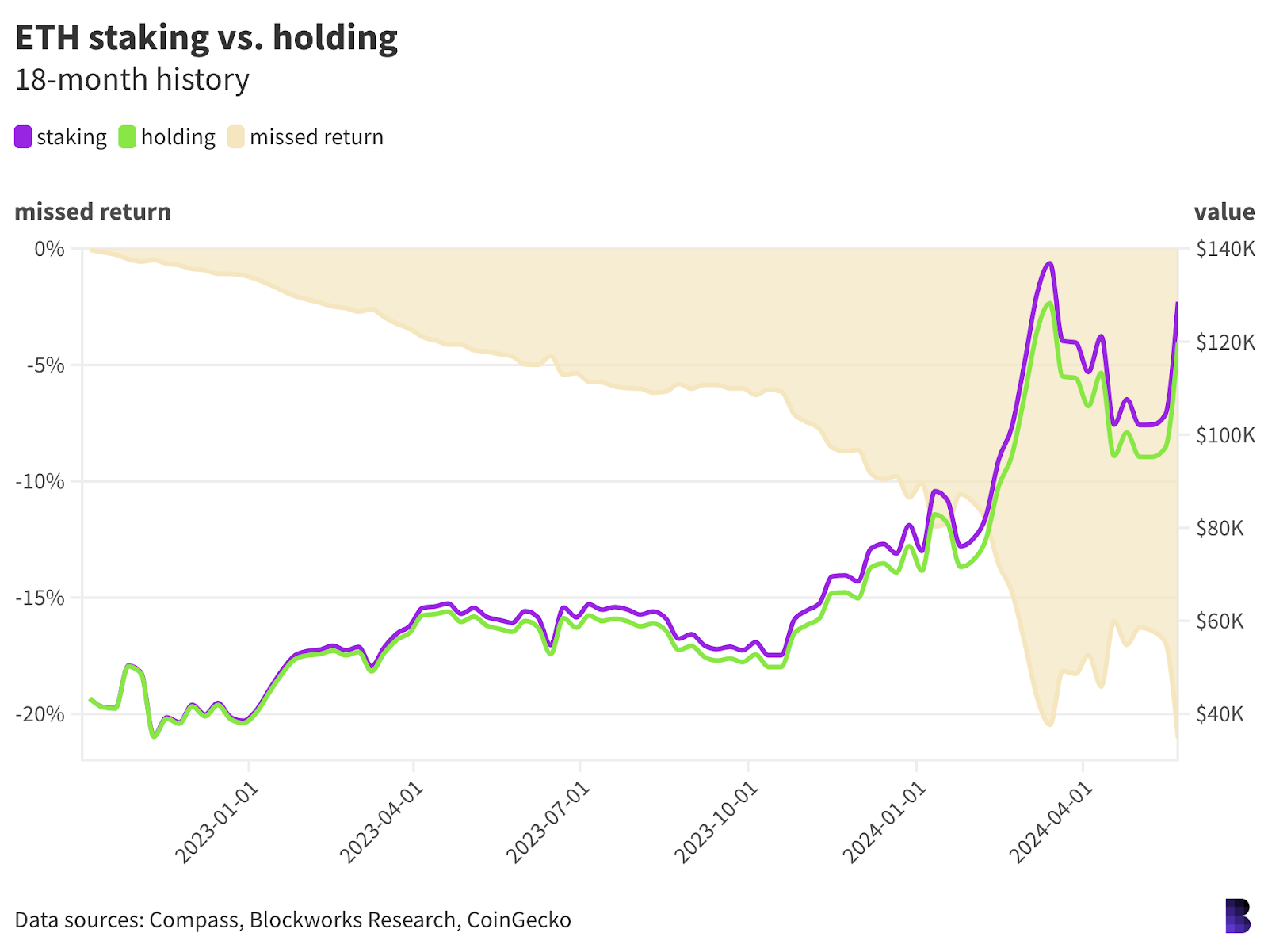

Missing out on a few percent doesn’t sound like much. But the lost returns are quickly amplified as the price of ether rises.

The green line on the chart below shows the value of 32 ETH — the stake of an Ethereum validator — over the past 18 months or so. It mirrors the portfolio of someone who bought and held ETH without staking it, which is how the US ETFs are set to operate.

The purple line otherwise maps the value of an Ethereum node participating in staking. What was originally 32 ETH turned into 34.36 ETH, the difference being the equivalent of $8,800 at current prices.

So, the holder spent about $42,000 to sit on 32 ETH, now worth almost $120,000 — 185% gains.

The staker contributed the same amount of dollars but now has $128,800 worth of ETH — 206% gains. (Activating MEV-boost on the node would also increase annual yield).

It could be that staking ETFs eventually get the green light. But in the meantime, the supposedly long-term ETF investor may be turned off by the first batch of ether-backed funds.

ETH, as an asset, can do so much more.

— David Canellis

Data Center

- More than 40% of all ETH validators are run by either Lido or Coinbase, down from 47% at the start of the year.

- Daily DEX volumes hit their highest point since March yesterday: $11.274 billion, up 56% week-on-week.

- Weekly Ethereum NFT sales volume has jumped almost 20%, now at $43.6 million and back above Bitcoin.

- After a 20% rally heading into the ETF news, ETH is now ahead of BTC for year-to-date returns: 58% to 53%.

- Most cryptocurrencies are down in the past 24 hours, with only five at the top end bucking the trend: ONDO leads with 18%, distantly followed by LDO, LINK, ZBC and XMR.

Mum is the word

I’ll admit: I was expecting more out of the SEC yesterday.

Specifically, I thought we’d get some kind of statement release on the level of what the agency’s leadership produced when they oversaw the approval of rule changes for spot bitcoin ETFs. Statements on their reasoning, the behind-the-scenes process, and how they agreed — or disagreed — with the ultimate outcome.

Last January’s statements were a fascinating window into a contentious policy decision, and given the recent hoopla around the ether ETF process — namely, the speculation that the very obvious and sudden turnaround was political in nature — one might have expected a similar body of discussion.

Except…nothing. Nada. Zip. Just the approval order and nothing else.

What gives?

The most likely explanation is that SEC Chair Gary Gensler wanted to avoid the perceived embarrassment of showcasing the broad disagreement among the agency’s leadership. Remember, the group of five commissioners vote on such matters. Gensler voted in favor of the bitcoin ETFs, describing the outcome as a “sustainable path” — not exactly an endorsement for someone who believes large swaths of the crypto sector are collectively thumbing their nose at the agency’s rules.

Buried in yesterday’s approval notice was the disclosure that the ETFs got the nod via “delegated authority” — that is, the Division of Trading and Markets was given the power to approve the products without a commissioner-level vote. As ETF analyst James Seyffart noted, this is normal and something the SEC does all the time.

But it’s also an intriguing direction to take if you wanted to, say, avoid providing a window into how political considerations shaped a crypto policy decision. The SEC is supposed to be an apolitical arbiter of markets. Revealing anything to the contrary would, well, blow a wide hole in efforts to maintain that perception.

Because the products were approved under delegated authority, any commissioner has 10 days to issue a challenge and force an actual vote. Whether that happens is anyone’s guess. It’s not impossible — remember, two commissioners voted against spot bitcoin ETFs on pretty vehement grounds — but to do so would certainly open up the SEC leadership to a fair bit of scrutiny.

The agency isn’t exactly Congress’ favorite right now, given the bipartisan repudiation of its crypto-related staff accounting bulletin.

As we like to say here when it comes to such things: Stay tuned.

—Michael McSweeney

The Works

- Congress’ crypto markets regulation bill now heads to the Senate. As Casey Wagner reports, House members who backed the measure are confident in its chances in the upper chamber.

- Speaking of Congress: The House yesterday also passed a measure blocking the Federal Reserve from issuing a retail CBDC.

- The FTX estate has wrapped up its sales of discounted SOL, Bloomberg reports.

- The London Stock Exchange saw half its ETF team depart, Bloomberg reports, a move that comes ahead of the market’s listing of crypto ETPs.

- Kabosu, the shiba inu who inspired the doge meme — which subsequently inspired dogecoin — has passed away. Rest in peace.

The Morning Riff

The spot bitcoin funds were a really big deal. The ether funds are too, but arguably more impactful is ether’s commodity classification.

If ETH is a commodity, then so, too, could be countless other similar assets for rival networks. Like Solana. Avalanche. Algorand.

It’s an exciting thought. But it’s likely that spot ETFs for other cryptocurrencies will still struggle on the path to approval.

CME listed bitcoin futures way back in 2017, and ether futures in 2021. Those offerings, sanctioned by the Commodities Futures and Trading Commission, largely laid the groundwork for the respective ETFs.

Crypto has for years squabbled with regulators over what constitutes a crypto security.

The real question is turning out to be: What is a crypto commodity?

— David Canellis

Start your day with top crypto insights from David Canellis and Katherine Ross. Subscribe to the Empire newsletter.

The Lightspeed newsletter is all things Solana, in your inbox, every day. Subscribe to daily Solana news from Jack Kubinec and Jeff Albus.