Berachain mainnet debuts as BERA token hits $1B market cap

The L1’s unique “proof-of-liquidity” consensus attracted $3.1 billion in pre-deposits

Berachain and Adobe stock modified by Blockworks

This is a segment from the 0xResearch newsletter. To read full editions, subscribe.

The world’s longest testnet is at an end. The Berachain L1 blockchain is officially launching its mainnet and BERA token today.

People are very excited! But that was already obvious. Berachain has attracted a ridiculous $3.1 billion in liquidity on its pre-launch liquidity platform Boyco, making Bera the 8th largest chain by TVL.

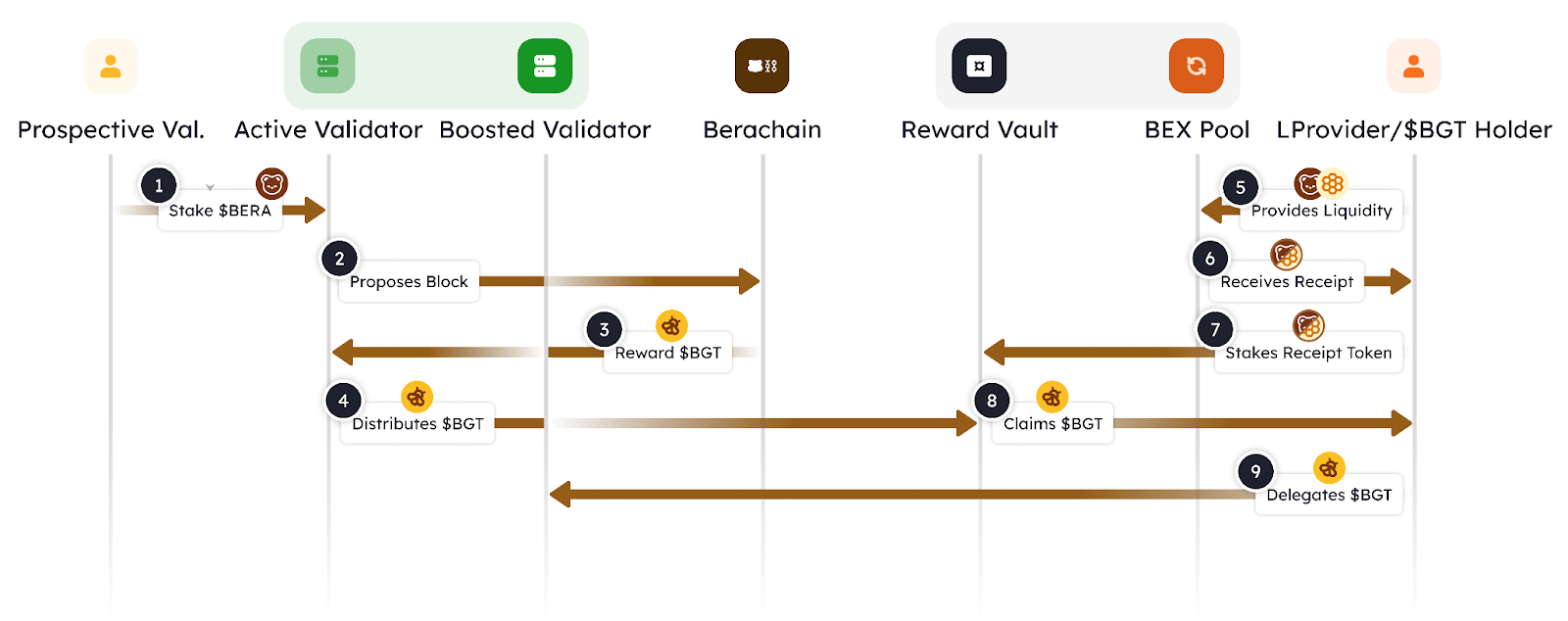

Bera’s early liquidity rush is thanks to its somewhat complex “proof-of-liquidity” (PoL) consensus mechanism.

Here’s the gist of it:

Your average proof-of-stake (PoS) network has a general-purpose native token (e.g. ETH or SOL).

Berachain splits that token into a dual token model:

- BERA serves as gas and a bond for validator staking.

- BGT is an inflationary but non-transferrable governance token.

The Berachain protocol emits BGT, and validators decide which dapps receive BGT emissions. Users who interact with these dapps (e.g. providing liquidity) can earn BGT.

But why do users want to farm a non-transferrable token? Because BGT is a veTokenomics-style bribe token.

You delegate BGT to validators, and this gives validators the governance power to direct future BGT emissions to whichever liquidity providers they like (hopefully, to the dapp you’re staking your liquidity on).

Source: Berachain

Source: Berachain

This, at its core, is what makes Berachain unique: the creation of a direct relationship between liquidity providers and block validators.

On traditional PoS chains, validators merely stake a bond (e.g. ETH/SOL) and secure the chain. On Berachain, validators are actively deciding which dapps/LPs should be rewarded with BGT for their capital provision.

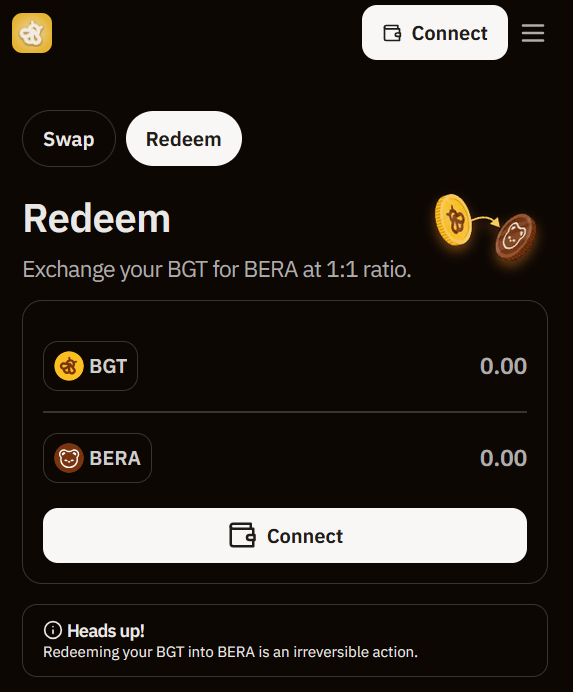

Now here’s the kicker. Calling BGT “non-transferable” is a bit misleading because BGT can be irreversibly burned at a 1:1 ratio to BERA. This means market values inevitably show up in the BERA token.

In contrast to the multiyear lockups on other veTokenomics models, such as Curve’s or Aerodrome’s, Berachain lets you exit when you like. But the exit is permanent.

You can’t buy your way back in like with CRV (BGT is a soulbound token). You’d have to farm BGT all over again.

This may explain Berachain’s early liquidity rush. Bera’s tokenomics are excellent at solving the cold-start TVL problem, because validators — who are already committed participants in the ecosystem — are internalizing the risks of liquidity provision, as opposed to the traditional playbook of dapps using their own native tokens.

But it also produces a flywheel effect that heavily privileges early participants in the Berachain ecosystem over later ones.

It may also explain why Bera has made the unusual choice to enshrine native applications — like its AMM DEX (BEX), money market (Bend) and perps DEX (Berps) at launch — as opposed to most L1s which outsource these efforts to third-party builders.

The earlier to this game you are, the bigger warchest of BGT you’ve already built, which in turns means the largest power you have to control future BGT emissions.

It’s the Curve wars all over again. Except now it’s taking place at the Berachain protocol level

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.