Meteora’s TGE: What is fair value for MET?

Weakness prevails across the board for crypto — however, it’s not all gloom and doom

Art by Crystal Le

This is a segment from the 0xResearch newsletter. To read full editions, subscribe.

Hi all, happy Tuesday. While Monday opened strong, weakness prevails broadly across the board. Under the surface, spot DEX volumes and active loans remain near highs. There’s a new token launching this week with Meteora’s MET: Where may fair value lie?

Indices

The week began with strength as BTC moved 7% higher from the low set this past Friday. Launchpads were the top performing sector on Monday’s trading session, while AI was the top loser, reversing some of the relative strength and weakness exhibited by each over the past week.

Zooming out to the weekly, the recent strength in launchpads positions this sector as the relative winner, only outperformed by Gold, which closed Monday again near a record high. Broadly, most indices remain negative on the weekly following the historic liquidation event. Within the launchpad index, AUCTION, a launchpad on BSC, is the only ticker to show positive gains on the weekly, up 46%.

While shorter timeframes show some green, the monthly demonstrates that almost every crypto index is down over the trailing 30 days. The Oct. 10 liquidation has left broad weakness across the board, with Gold, Crypto Miners, AI and Equity indices being the only areas of strength.

The VIX has retraced significantly, down to 18 after Friday morning’s pop to 29. Both the S&P500 and the Nasdaq traded higher during Monday’s session, closing just a stone’s throw away from a new all-time high.

Market Update

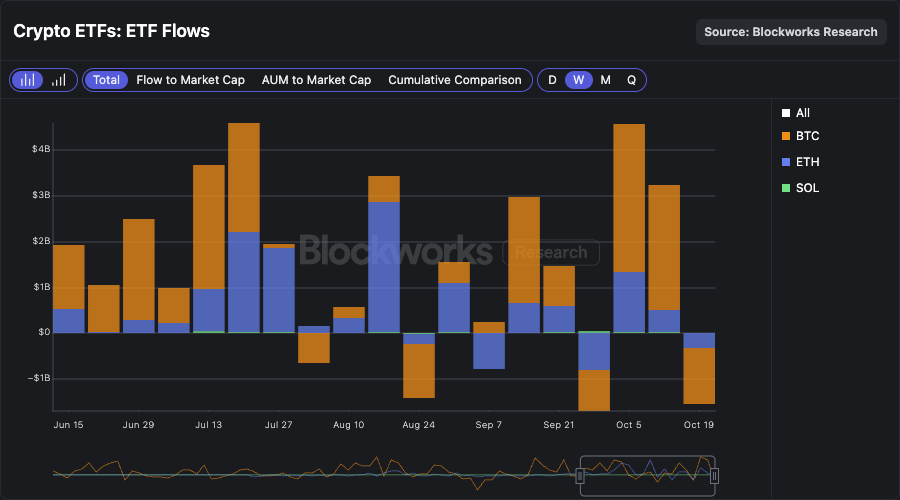

ETF flows remain muted and negative. Monday shows -$40 million from BTC, -$145 million from ETH, and +$27 million into SOL ETFs. Looking at the weekly, last week saw -$1.5 billion in net outflows across the ETFs, reversing some of the accumulation from a very strong open to October. SOL ETFs were the only product to show net inflows, adding +$14 million.

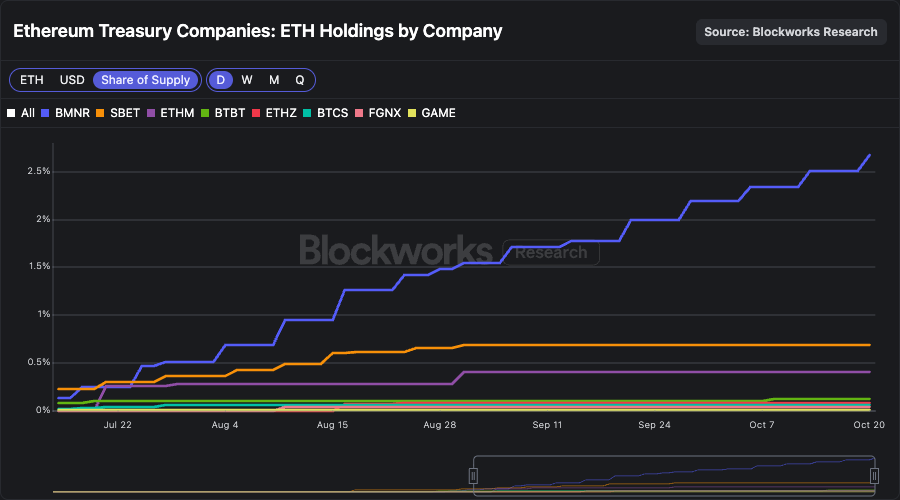

Within DATCOs, BMNR is running away with it. The vehicle now holds 3,236,014 ETH, more than the holdings of all other ETH DATCOs combined, and 2.67% of the total ETH supply. Notably, BMNR has continued to grow its stack of ETH nearly ~70% since the end of August, while most other ETH DATCOs have flatlined. In doing so, BMNR’s market share of the ETH held by DATCOs grew from 50% toward 65% now.

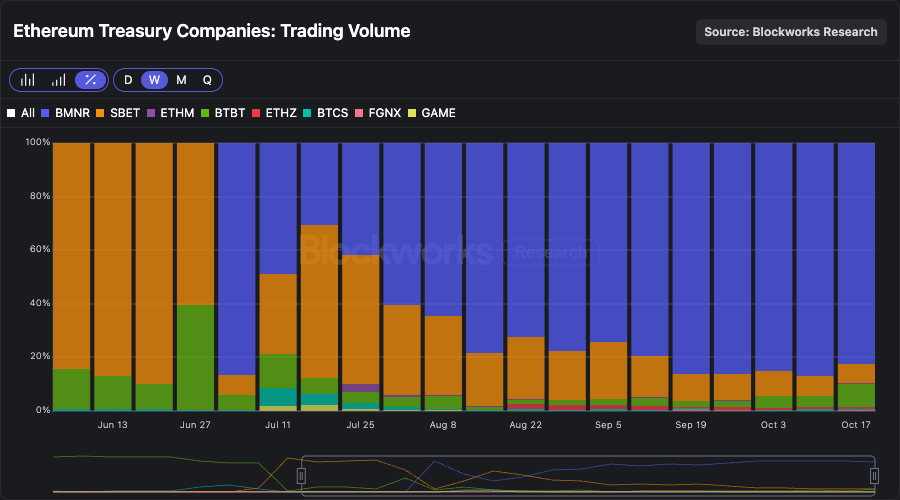

This story is mirrored in trading volumes of ETH DATCOs. BMNR has accounted for 60-85% of the trading volume of ETH DATCOs, allowing its stock to be the most liquid. This liquidity feature gives the vehicle preferential appetite from bigger allocators, and also reduces the marginal impact on price from ATM share offerings. BMNR seems to be the clear winner in this sector for ETH treasury companies.

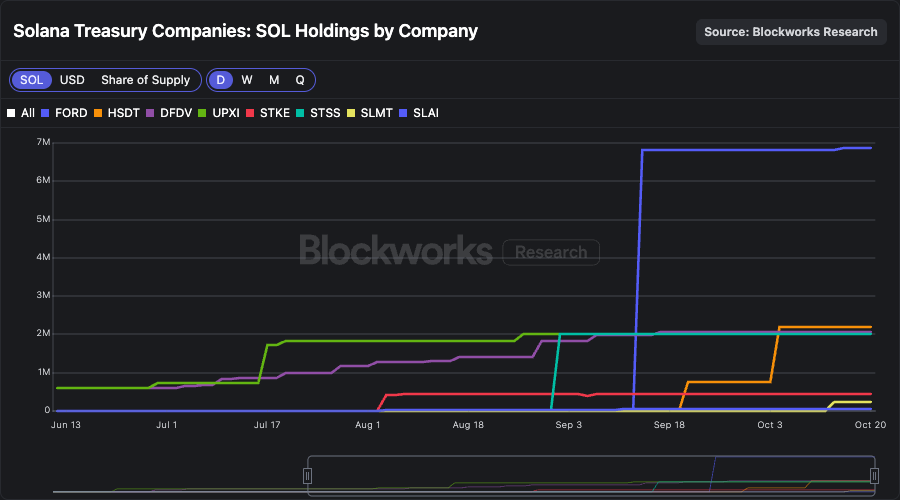

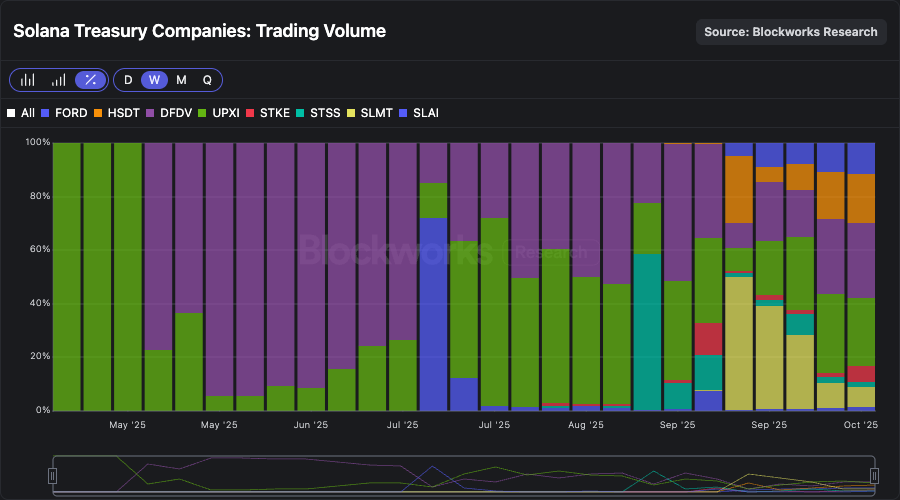

Within SOL DATCOs, the picture is less clear. FORD remains the largest vehicle by holdings, with almost the entirety of this size acquired through the proceeds of the PIPE offering. The vehicle has yet to grow its stack meaningfully through ATM share offerings, despite a $4 billion ATM offering program having been authorized.

Going down the list, growth in holdings remains muted, with HSDT recently moving into second place.

Trading volumes for SOL DATCOs tell a similar story. While DFDV was once the majority of this sector’s volumes, the picture has moved towards more of an even split across the top names. While FORD accounts for ~43% of the SOL held by DATCOs, it only accounts ~10% of the sector’s trading volume, showing relatively little turnover in the stock. This data could be good grounds to justify why very little SOL has been stacked through FORD’s ATM offering.

While BMNR is emerging as a clear winner for the ETH names, the leader in the SOL sector may still be up for grabs. Over the coming month, I would expect volumes to increasingly concentrate around the top names, and funnel the cream to the top.

Meteora’s TGE: What is fair value for MET?

Meteora’s (MET) highly anticipated TGE will take place on Thursday, Oct. 23. Unlike the recent trend of projects conducting an ICO sale, Meteora is not fundraising before TGE. Instead, it’s airdropping to eligible recipients, including Mercurial stakeholders, Meteora LPs, JUP stakers and launchpad partners. Airdrop recipients will receive unlocked MET by default or choose to provide liquidity at launch to earn trading fees (up to a limit of 10% of the total supply of 1 billion tokens).

As historical context, Meteora was launched in February 2023 by the team behind Jupiter, Solana’s largest DEX aggregator and perps trading platform. When Meteora launched, the previous iteration of the protocol, Mercurial Finance, was sunsetted. The reason for shutting down Mercurial, along with its governance token (MER), was that there were significant amounts of MER involved in FTX/Alameda, so the team decided that the best course of action was to rebuild the platform with a new token (MET).

Back in 2023, the team announced that 20% of MET tokens would be distributed to Mercurial stakeholders at TGE. As seen below, the team has kept its initial promise, with 15% allocated to Mercurial stakeholders and 5% to Mercurial Reserve (those directly affected by the FTX insolvency). In addition, the DEX has been running a points program since Jan. 31, 2024, for which a total of 15% of MET will be allocated. At launch, 48% of MET’s supply will be circulating, a high float compared to other notable token launches in the Solana ecosystem, such as JTO, KMNO, or JUP itself (13.5% float at launch).

Source: https://met.meteora.ag/

Source: https://met.meteora.ag/

As mentioned previously, 10% of the total supply (100 million MET) will be used to bootstrap the initial liquidity via a dynamic AMM pool, with a starting price of $0.5 ($500 million valuation) and liquidity spread across to $7.5 billion valuation. Early on, the liquidity pool will be single-sided (MET only), and early buyers will swap their USDC for MET. Note that the pool fees start high and drastically decline over time through a fee scheduler.

Source: https://met.meteora.ag/

Source: https://met.meteora.ag/

Napkin math valuation

DEXs, particularly on Solana, lack a significant moat since they historically do not own the frontend. The best example of this dynamic is Raydium losing millions of dollars in volume and revenue after Pump decided to redirect graduated coins to its own AMM, PumpSwap. Meteora has attempted to mitigate this issue by vertically integrating, expanding its distribution capabilities via Jupiter and select launchpad partners.

As mentioned, the DEX is operated closely with the Jupiter team, which has become the gateway for less sophisticated retail users to trade onchain. In addition, Meteora partnered with Moonshot in August 2024 to introduce a launchpad and has onboarded new partners over time, including Believe, BAGS and Jup Studio. The chart below shows that launchpad activity has contributed between $200K-$800K in weekly revenue for Meteora in recent weeks, with most flows coming from Believe and BAGS.

Looking at overall financials, Meteora has generated $8.8 million in revenue in the past 30 days across all of its pools, with weekly revenue consistently nearing $1.5 million, even in periods of relatively low onchain activity. To note, over 90% of Meteora’s revenue comes from memecoin pools, which generally have higher fee tiers than SOL-stablecoin, project tokens, LST and stable-to-stable pools.

Regarding valuation, we can look at Raydium and Orca as comps. The chart below shows RAY and ORCA’s price-to-sales ratio year to date on a 30-day annualized basis. We observe that both assets have been priced at relatively similar ratios up until September, when RAY began trading at a premium. Zooming out, both assets have seen a median P/S of 9x in 2025.

The table below compares RAY and ORCA’s P/S ratios across various lookback periods. We observe that ORCA is trading very similarly across all annualized timeframes, at around a 6x P/S ratio. In contrast, RAY has become more expensive over recent months as revenues have declined. On its part, we see that Meteora’s annualized revenue falls between ~$75 and ~$115 million, depending on the lookback period.

Finally, below we show MET’s potential valuation across various revenue and P/S ranges. In our view, a P/S between 6x and 10x is most likely based on how RAY and ORCA have been historically priced. As such, we could reasonably expect MET to trade between $450 million and $1.1 billion after launch (circulating market cap). Note that based on the figures below, valuation starts getting a bit expensive over $1 billion relative to comps, and over $2 billion MET would be almost definitely overvalued, unless it can increase its revenue run rate.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.