Unichain mainnet is live with value accrual for UNI

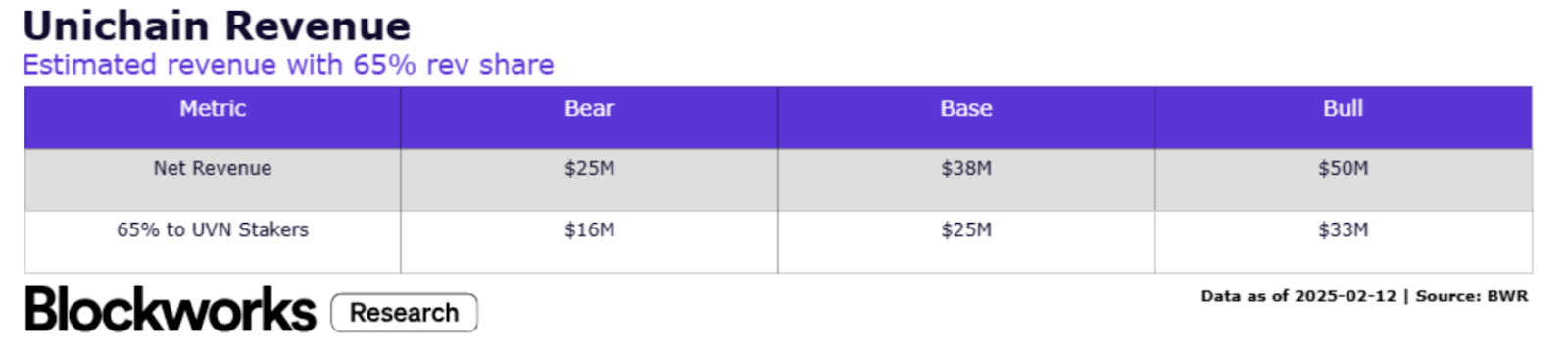

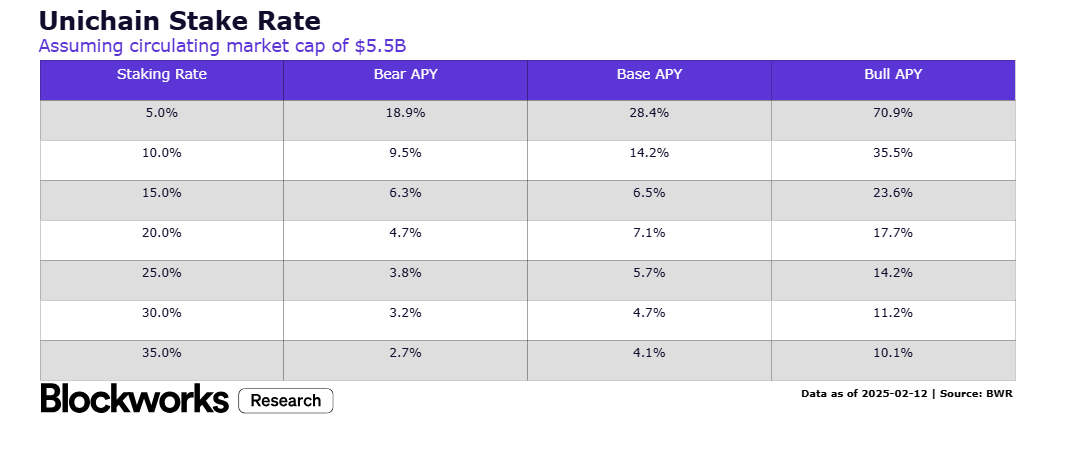

Expect $16 million to $33 million in annualized staking yields, Blockworks Research estimates

ARTEMENKO VALENTYN/Shutterstock modified by Blockworks

This is a segment from the 0xResearch newsletter. To read full editions, subscribe.

Four months after its initial announcement, Uniswap’s L2 rollup mainnet went live yesterday.

Despite its name, Unichain is a general purpose L2 rollup. At least a dozen applications have already been deployed on the chain, including Euler, Renzo, Morpho, Lido and more.

So it’s another L2. What makes Unichain different?

For one, Unichain has quicker finality at 200-250 milliseconds, a significant upgrade over Ethereum’s 12-second block time or most OP stack chains’ block time of two seconds.

Second, Unichain is a Stage 1 rollup right out the gate. This means a permissionless fault proof system has been deployed that allows anyone to verify or challenge transactions independently, unlike Stage 0 rollups such as Base.

When Unichain was first announced late last year, it threatened to exacerbate ETH’s value accrual problem. Why? Uniswap is still one of the largest gas guzzlers on Ethereum L1, which contributes to a higher burn rate of ETH i.e., value accrual.

The silver lining is that a significant number of v2 and v3 users will probably not migrate to Unichain immediately. Users are sticky. Uniswap v3 will have been live for four years in May and yet its v2 deployment still enjoys a deep moat of liquidity (~$1.5 billion in TVL).

Expecting Uniswap LPs and users to bridge to a rollup chain looks to be fraught with even more friction, let switching between frontends.

Peter Thiel famously said that customers accept switching costs when product innovation is at least a 10x upgrade from existing options, not mere incremental improvements.

Does Unichain, the L2 rollup, offer that tenfold improvement? I don’t think so. Perhaps Uniswap v4 and hooks do, but v4 is also already live on eight other chains.

Should the bulk of liquidity and users migrate to Unichain, however, it would at least appease one group of stakeholders: UNI token holders.

Last week, Uniswap Foundation announced a revenue-sharing structure that would allocate 65% of net chain revenue to validators and stakers on the Unichain Validation Network (UVN).

It’s hard to overstate the importance of this development.

For years, UNI token holders have lamented the lack of value accrual. The UNI airdrop was a “last resort” move that served to stave off the infamous SushiSwap vampire attack in 2020.

And it worked. Uniswap re-established itself as the top DEX. But then UNI existed as a meme token with no productive cash flows.

On a recent Bell Curve podcast, Felipe Montealegre of Theia Research likened UNI’s treatment as a “second class citizen” compared to Uniswap Labs equity.

So the UNI fee switch is finally here. How much cash flows should UNI stakers expect?

About $16 million to $33 million in annualized net revenue, Blockworks Research analysts Luke Leasure and Daniel Shapiro told me.

“Estimating the fees and APY that will accrue to UNI stakers on Unichain’s UVN requires a few assumptions. Firstly, the 65% of net earnings that accrues to the UVN are a function of base fees, priority fees and MEV paid to transact on the L2, less the expenses of posting data to the L1 and the Optimism Collective’s take rate on gross and net chain revenue. With this, the Base L2 may be the most appropriate comparison to estimate Unichain’s financials,” Leasure and Shapiro said.

“DEX activity is the largest driver of fees by a significant margin. Over the trailing 30 days, Uniswap did ~$100b in trading volumes, whereas Base is around $50b with around $100m in annualized net revenue. Assuming Unchain captures 9-25% of Uniswap’s volume, this would put Unchain L2 activity at 25% to 50% the activity of Base.”

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.