Why value accrual matters for tokens

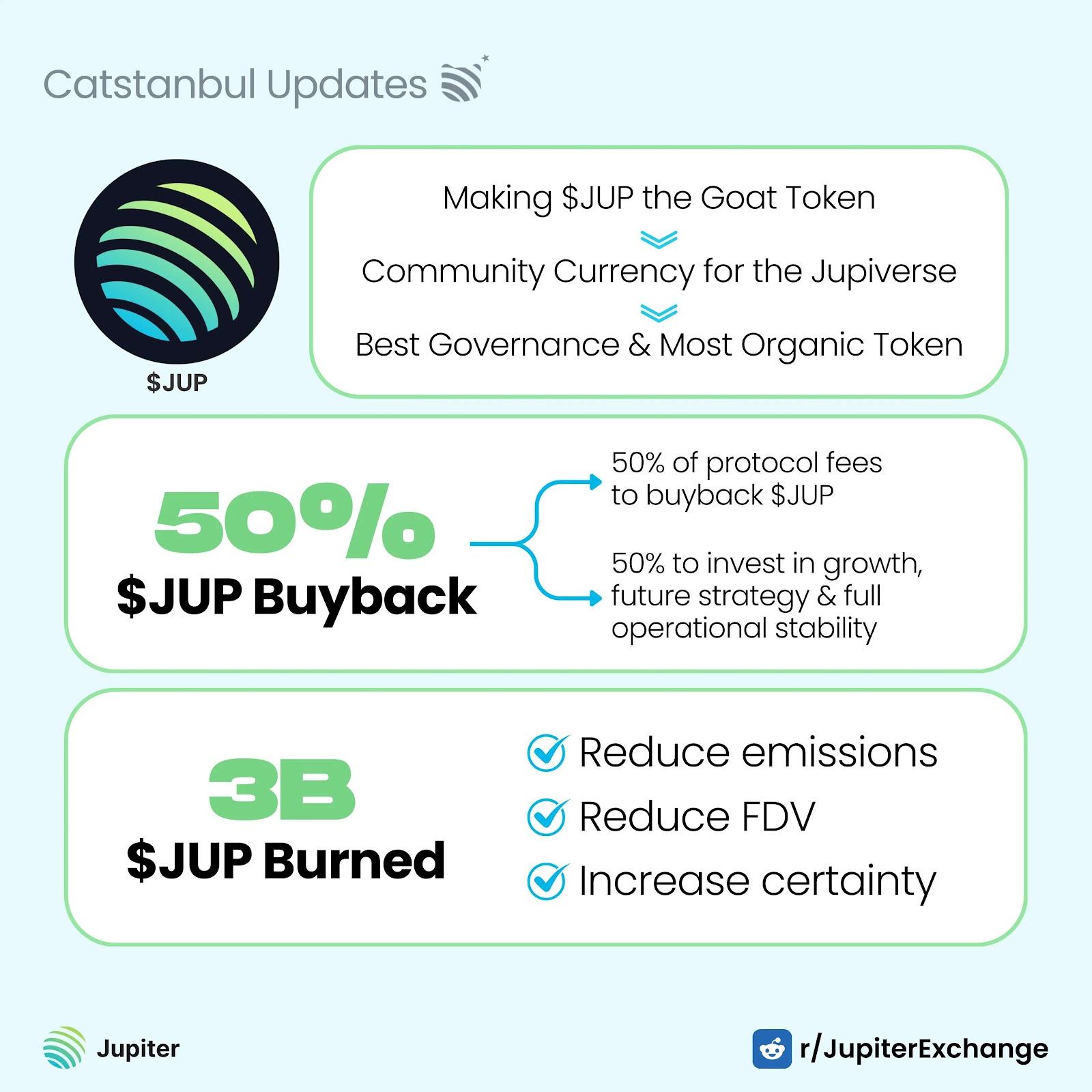

Based on Blockworks Research estimates, JUP buybacks comes up to ~40% of total supply

CryptoFX/Shutterstock modified by Blockworks

This is a segment from the 0xResearch newsletter. To read full editions, subscribe.

When crypto projects make big announcements using words like “buyback,” “burn,” or “revenue sharing,” that’s usually taken to mean there are bullish investing tailwinds at play.

But I have questions. How much does an annualized 10% buyback yield actually matter when these tokens can plummet 20% in a day?

Does value accrual matter because it is valuable for reasons of fundamental analysis (i.e. cash flows), or merely for narrative optics?

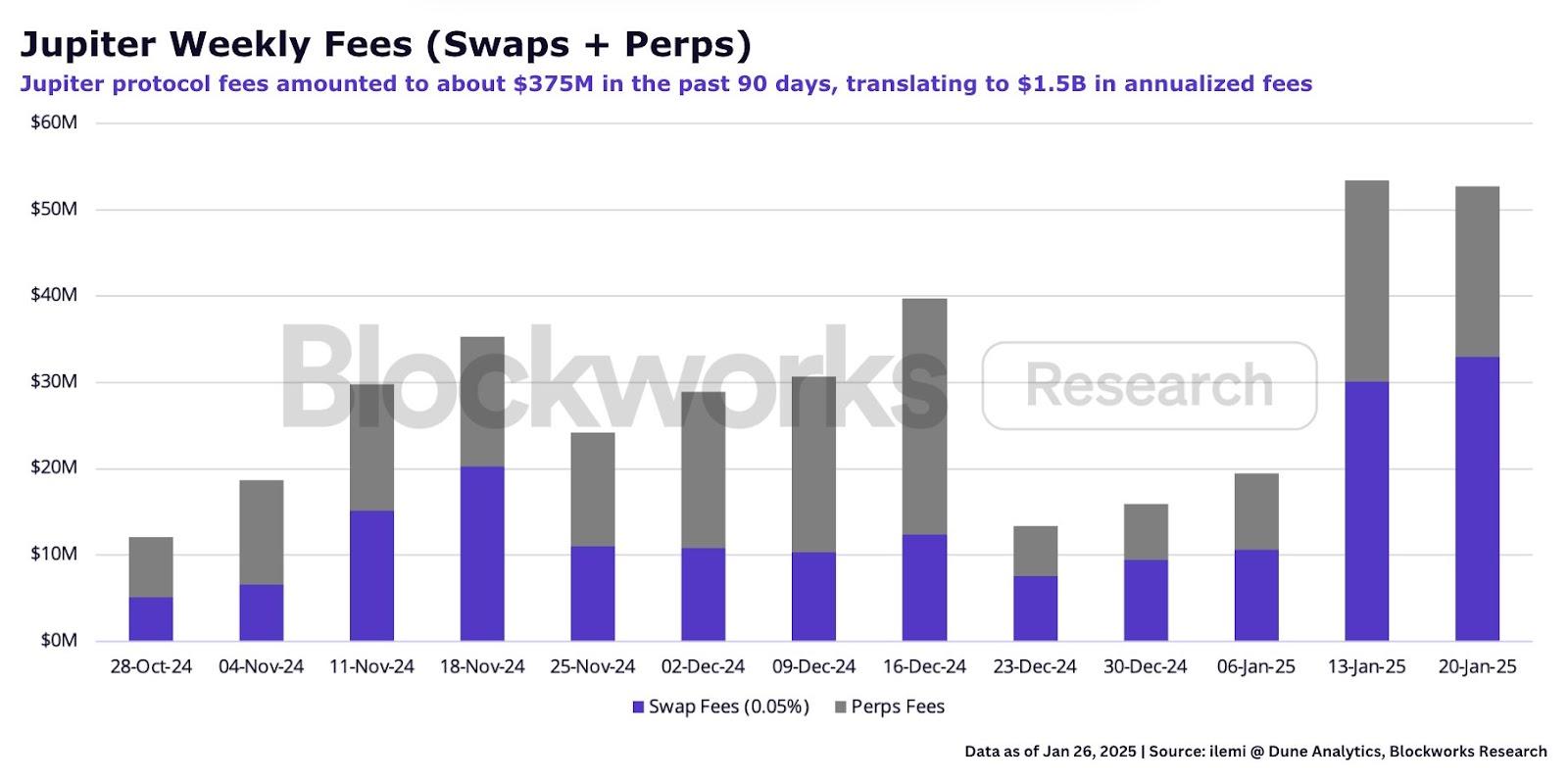

Over the weekend, Solana DEX aggregator Jupiter announced a significant JUP buyback program with 50% of fee revenues.

Based on estimates by Blockworks Research analyst Carlos Gonzalez, that translates to about $750 million in annualized JUP buybacks, or about a significant 40% of JUP’s circulating supply in a year.

Source: Blockworks Research

Source: Blockworks Research

That’s a pretty impressive annualized buyback yield of about 42%.

But what does 42% matter when token prices can tank 90% in a week?

Well, it’s not a flash in the pan solution, but it helps to sustain against selling pressure. Carlos pointed to Raydium’s successful experiment with buybacks:

“Raydium has accumulated 20% of RAY’s supply since the start of their buyback program. In terms of market structure, it adds buying pressure to the token and RAY has outperformed most of Solana DeFi. Fundamentals matter but of course you could also find examples to argue that buybacks aren’t that bullish. For instance, Maker.”

Virtuals, the leading AI agent launchpad on Base (now expanding to Solana), also committed two weeks ago to an estimated $40 million in buybacks and burns for 10k+ agent tokens over a 30-day TWAP.

Since the buybacks were announced on Jan. 15, the five largest agent token buybacks by far are GAME, CONVO, AIXBT, SEKOIA and MISATO, all of which have given up all their gains as of yesterday’s market crash.

Over the last year, many blue-chip DeFi protocols with actual product-market fit have also sought to return revenues to token holders.

Compound, for instance, proposed in August a fee switch to allocate 30% of its reserves to COMP stakers.

Marc Zeller of Aave proposed last July a “Buy & Distribute” proposal to buy back AAVE on the open market with “net excess revenue of the protocol.”

Then there’s Uniswap, which planned to implement a UNI fee switch for stakers, but quickly abandoned the proposal after receiving an SEC Wells notice two months later (Uniswap is again attempting some form of value accrual on its upcoming Unichain).

Major L2s like Arbitrum, Starknet and Gnosis have floated proposals last year to return value to token holders who stake their tokens.

Starknet voted last September to enable Starknet staking (12.94% APY) and Gnosis passed a proposal in June to spend $30 million of the DAO’s treasury to buy back liquid GNO over a six-month period.

As far as I can tell, out of all the above-mentioned value accrual proposals, only Starknet and Gnosis have actually implemented their value accretive mechanisms.

Yet from the time these value accrual mechanisms were put in place, GNO has seen a 46% decline, while STRK has stayed flat.

So what are the right mental models to think about value accrual mechanisms? They’re not a magic bullet. But they’re a key ingredient in the recipe of getting a successful token launch right.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.