Are we at the start of a new business cycle?

Everything has been somewhat upside down in recent years, leaving many economists befuddled

Andy.LIU/Shutterstock modified by Blockworks

This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

Ever since COVID closed global economies in 2020, gauging where we stand in the business cycle has been a very difficult act.

The typical business cycle looks as follows, and historically, it’s been fairly easy to have a general idea of where we stood by contrasting it with interest rates and monetary policy:

However, everything has been somewhat upside down in recent years, leaving many economists befuddled.

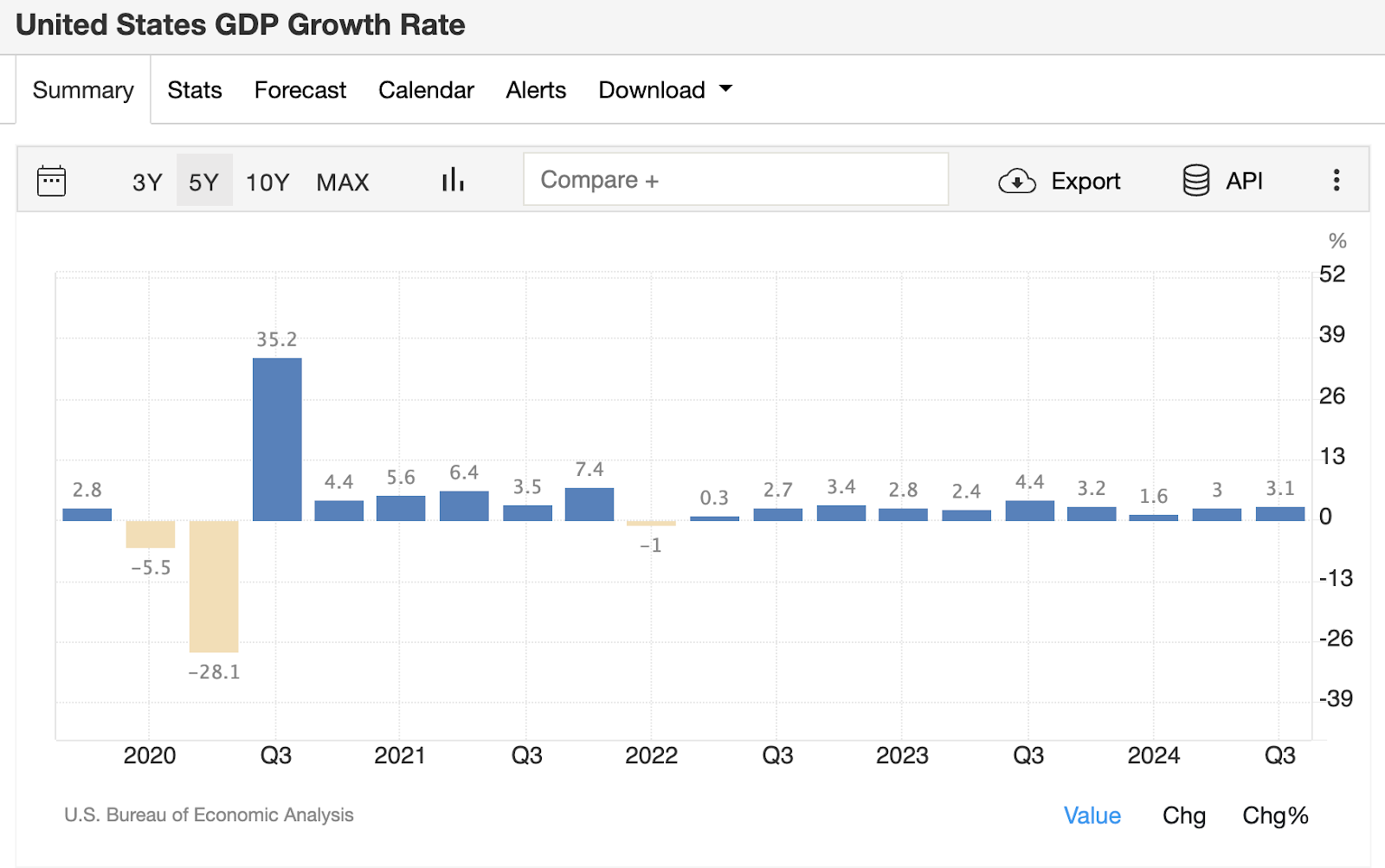

For example, in 2022 we saw negative real GDP prints (initially at two but then revised down to one):

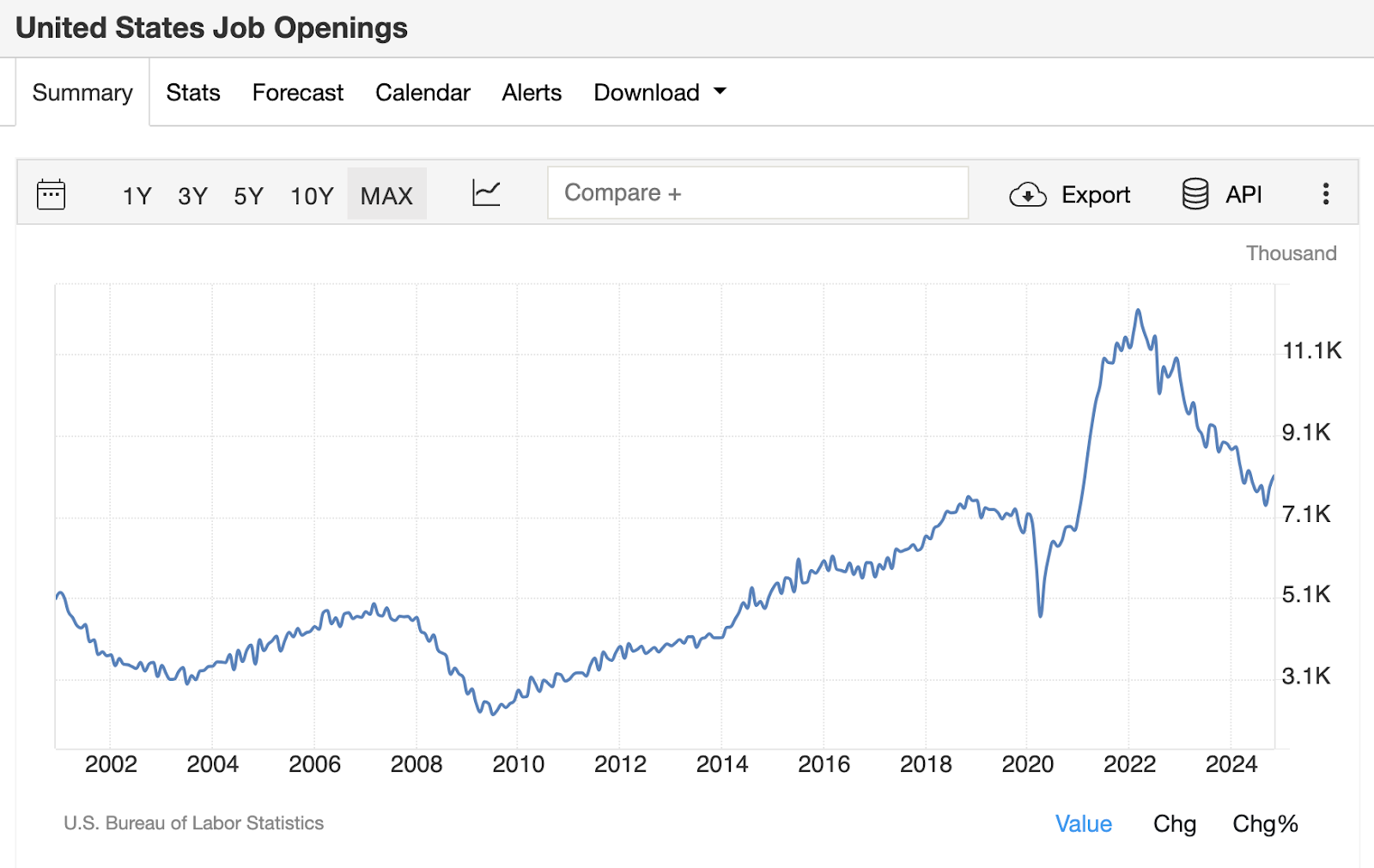

However, during that same time we saw one of the hottest labor markets we’ve ever seen, as per JOLTS data.

It’s hard to believe in a recession with a labor market that strong:

Since 2022, we’ve seen a major rate hiking cycle from the Fed that somehow also didn’t tilt the economy into a recession when looking at it on an aggregate basis. Stocks hit new highs everyday, the labor market cooled but remained resilient, and GDP growth powered ahead.

During that same time, however, if you honed in on the manufacturing and goods sector and set aside the services economy, it almost looks like we’ve just been through a manufacturing recession.

ISM Manufacturing PMIs have been in contraction territory for a couple years now:

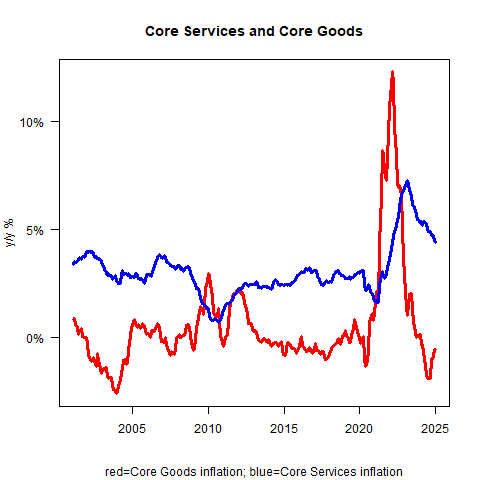

During that time, we saw significant disinflation leading to outright deflation in the goods sector of the economy:

Source: inflationguy.blog

Source: inflationguy.blog

Fast forward to today, and we’ve seen the Fed cut rates to frontrun concerns about the labor market and continue attempting a soft landing of the economy where we move into a new business cycle without a recession.

We’re now seeing leading indicators hinting that the manufacturing sector might be exiting the doldrums and heading toward a new upswing.

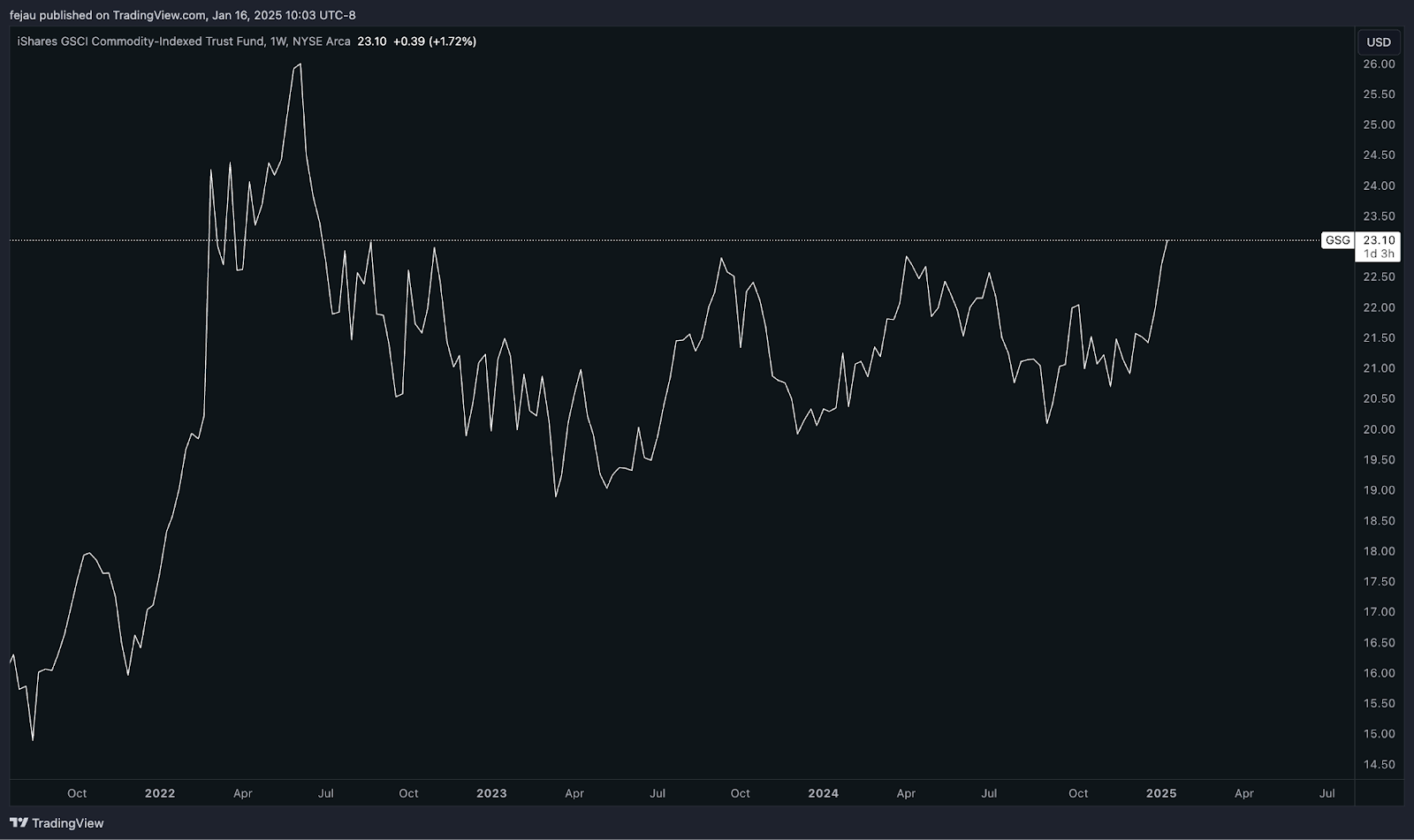

We’re starting to see commodities begin to break out after two years of consolidation, hinting at an upswing in economic growth:

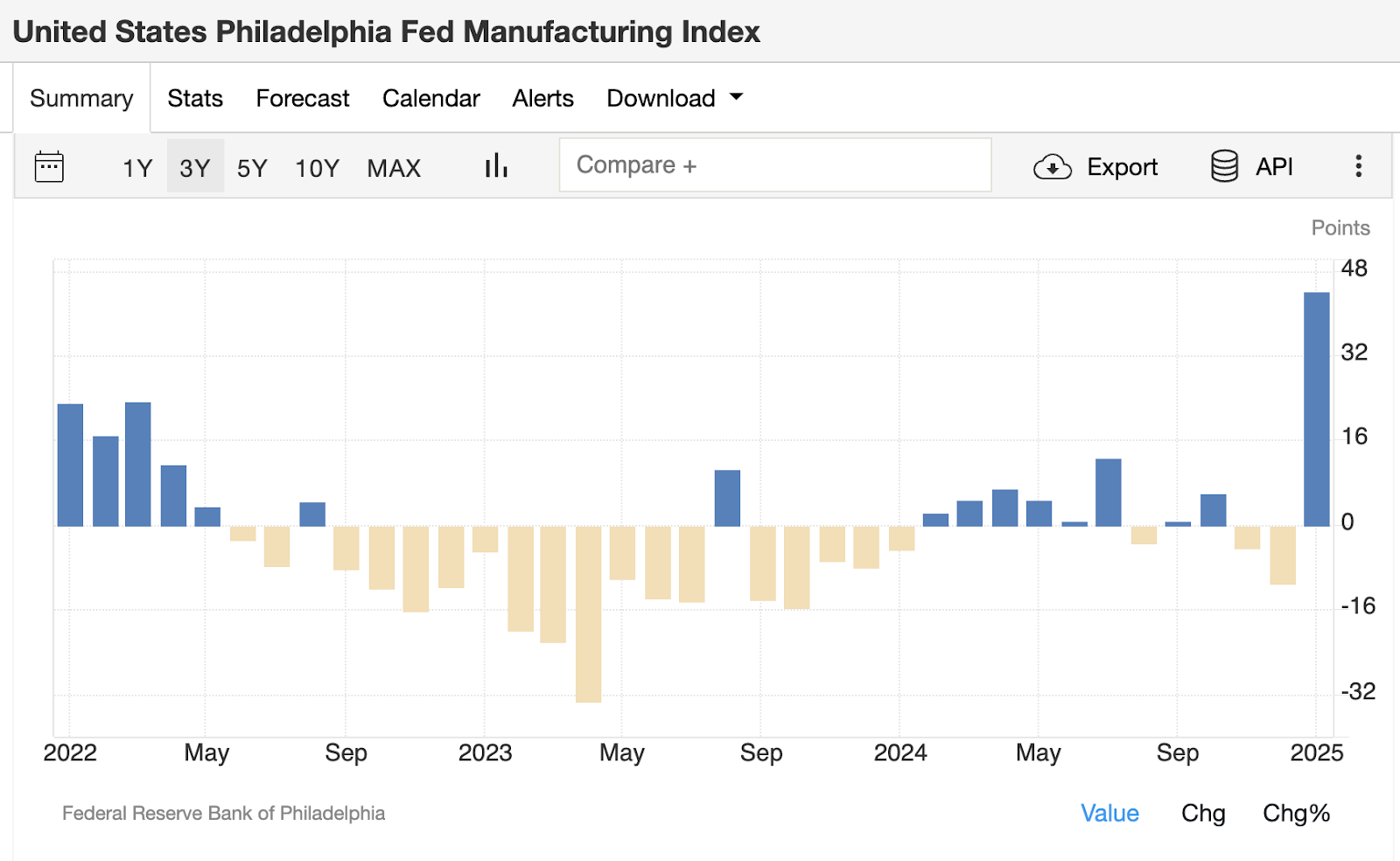

ISM new orders look to be breaking out, as well as the Philly Fed manufacturing index:

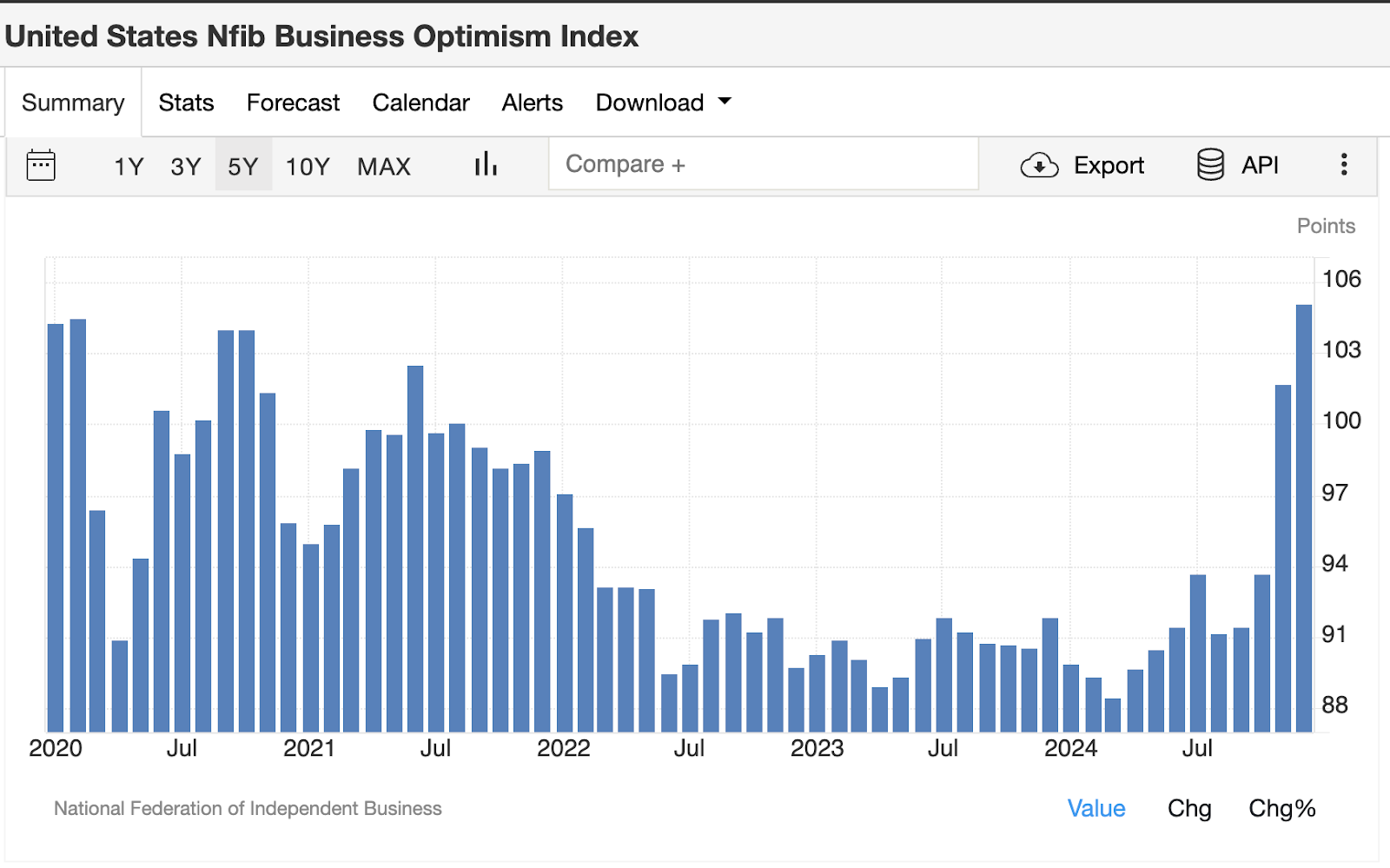

Per the survey data, it’s looking like much of this is being led by optimism from the business sector ever since the election:

So where does this chart-geeking journey lead us?

I think it’s safe to say we’re not late in the cycle. It increasingly looks like we are in fact in the early innings of a new business cycle that avoided a recession due to the huge fiscal stimulus and deficits during the last couple of years.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.