Understanding the Biggest Institutional Adoption Bottleneck: Poor Settlement

When trading is executed on a blockchain ledger, clearing and settlement can happen simultaneously

Source: Shutterstock

Institutions want to get into crypto. No one argues this point much anymore. The thing is, it’s not easy for traditional finance players to participate in blockchain-based digital asset markets.

And while regulation is often cited as the main problem holding back institutional adoption, there are other, more logistical issues that need to be addressed as well.

The most significant bottlenecks faced by TradFi traders looking to trade digital assets include:

- Counterparty risk

- Collateral management

- Balance sheet control

Today’s stock exchange process dates back at least 100 years, with things gradually becoming digitized within the last 50.

Due to the way blockchain ledger technology works, crypto trading looks a little different. Namely, crypto exchanges require traders to prefund every trade.

This creates an operational nightmare for trading firms because it requires them to manage spreadsheets that track trades across multiple exchanges and custodians as well as bilateral settlement with OTC desks. Many firms claim that over 40% of their staff focus on the sole task of sorting out this problem.

Why do things work this way, how does it create a problem, and what are some potential solutions?

The nature of the problem

Blockchain tech has led to an inherent restructuring of the clearing and settlement process.

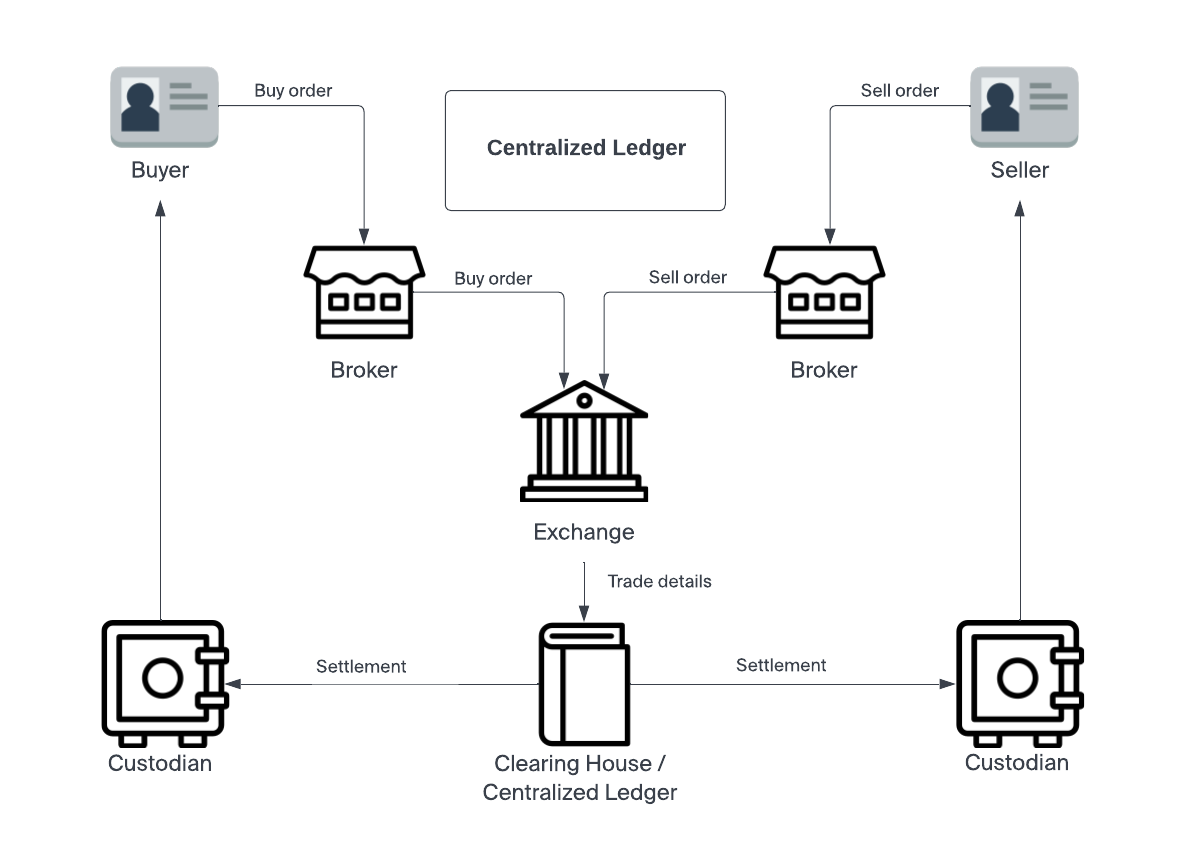

In traditional finance, this process involves three steps: execution, clearing, and settlement. These are handled by an intermediary known as a clearing house.

Execution is when a broker fills an investor’s order to either purchase or sell a security. It is the broker’s responsibility in this process to fill the order at the best price possible. Once the order is filled, it enters the clearing stage. It is at this point that another party called a clearing house takes the responsibility of validating the identity of the other party and confirming that they have the asset in question. Once all necessary parties are cleared, the trade enters the settlement stage. It is here that the asset officially changes hands between the clearing house and the investor’s custodian.

The clearing house exists to provide a neutral party to the transaction between the exchange and custodian. And it marks the key difference between blockchain settlement. Since traditional settlement requires trust, the opposing parties use neutrality of the clearing house to represent both parties’ interests fairly. It is what ultimately permits the clearing house the authority to officially transfer deeds of ownership.

But it is important to note that the clearing house does not exchange assets with the custodian on an individual basis. This would make the process exponentially more inefficient. Instead, the clearing house and custodians net transactions across their balance sheets in a way that reduces the number of individual transfers. For example, a pending transaction from the custodian to the clearing house can cancel out or net an equivalent pending transaction from the clearing house to the custodian.

This type of accounting permits the investor the ability to fund the trade after it is settled with the custodian. This creates capital efficiency for all parties involved – which increases the volume of total trades.

Settlement on the blockchain

But when trading is executed on a blockchain ledger, clearing and settlement can happen simultaneously. Parties already have their identities verified and the price and volume of a trade has been agreed upon in the form of a transaction on the ledger. But this expedited process is a double edged sword. Since there is no clearing house managing a balance sheet with regulated custodians, exchanges are forced to require prefunding for every trade. There is no T + 2 settlement time which allows a window of time for funding to occur. Blockchain-based transactions can happen on a T + 0 basis. When using a crypto exchange, “you have direct access to the market,” as Gary Gensler put it in a 2018 lecture at MIT on post trade clearing, settlement, and processing.

The requirement for institutions to adapt to this model has slowed the pace of adoption to a crawl. Instead of having transactions handled by a clearing house, the blockchain-based model makes it necessary for institutional desks to track trades between multiple exchanges using spreadsheets.

About 68% of trading firms state that inefficient funding and settlement workflows were the primary obstacles they faced when it came to scaling their business.

What can be done to mitigate this monumental roadblock?

The solution

Fortunately, the team at Apifiny has been working on ways to solve this problem.

With the Apifiny platform, users create a single account with a single set of onboarding and APIs. The platform is connected to over 20 exchanges, allowing users to manage all of their trades in one place. Fund transfers can also be managed from the main account to an external exchange, or between different exchanges, all from Apifiny.

This solution addresses the capital efficiency obstacles from a different angle. Instead of instituting a trusted third party for netting, it makes direct access to the market more approachable.

Apifiny clients can transfer between their sub-accounts without having to maintain reserves on multiple platforms. This flexibility makes the operational bottlenecks less inconvenient and opens the door to greater institutional interest. The platform also supports secured transfers via Fireblocks and instant transfers on select exchanges.

While these technological innovations make the funding cycle more streamlined, Apifiny is also working on developing solutions to address the systemic challenges. They believe that a regulated clearing system can be instituted in a way that leverages the efficiency of blockchain technology without forcing custodians and exchanges into bilateral settlement with OTC desks and market makers. Haohan Xu, founder and CEO of Apifiny said,

“We’re focused on building the infrastructure for professional traders or institutions to access the complete route to the market in the most seamless way possible.”

A comparison between the current fragmented market illustrates their approach.

Haohan Xu went on to add, “So, our end goal here is using strong infrastructure as a method to consolidate and glue together a complete crypto market so that traders can have one-stop access from price discovery and liquidity; cross-trading venue fund rebalancing and management; to post-trade reporting and analysis.”

This content is sponsored by Apifiny.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.