How BlockFi Went From Tech Unicorn to Crypto Burnout

BlockFi was one of the fastest growing crypto startups in history, but bear market realities struck during a week of rapid calls before Bankman-Fried’s bailout

key takeaways

- Blockworks has mapped BlockFi’s tumultuous last 18 months via internal documents and conversations with current and former employees

- BlockFi is now fighting to boost company revenues, which have sunk nearly 70% since January

Just 12 months ago, BlockFi was going places. Fast.

The crypto lender went down as one of the most rapidly growing startups in the industry amid a roaring bull market and a slew of outrageous valuations in 2021, raising hundreds of millions of dollars from blue-chip financiers including Bain Capital, Tiger Capital and Peter Thiel’s Valar Ventures.

It seemed, for some time, nothing could slow CEO Zac Prince’s meteoric rise. And few could have predicted what was to come: a sudden $250 million dollar bailout in June, orchestrated at the eleventh hour by Sam Bankman-Fried of FTX.

The essence of what went wrong, and why, hold crucial lessons not only for BlockFi, but for all cryptocurrency firms navigating the ups and downs of a market cycle, sources told Blockworks. In Prince’s case, his company’s near-collapse can be traced at least as far back as last year, when a series of critical — and sometimes questionable — management decisions left the lender on shaky ground.

The impetus? BlockFi executives quietly pining for what would have amounted to the startup’s first down venture round from some of the biggest Wall Street players, even as crypto markets floundered.

In the days leading up to the FTX deal, which awarded Bankman-Fried the right to scoop up BlockFi for as little as $15 million, Prince scheduled a flurry of executive meetings in a bid to uncover other options — with ConsenSys, Binance, Fortress, JPMorgan, Galaxy Digital, as well as blockchain magnate Barry Silbert, among others — according to Prince’s Google calendar.

Blockworks spoke to three sources familiar with the matter for this account, including current and former BlockFi employees. Sources were granted anonymity to discuss sensitive business dealings. It also relies on internal company documents obtained by Blockworks.

One or two, perhaps inconsequential, mistakes, as it turns out, may have been the high-flying startup’s near-fatal flaw.

A spokesperson for BlockFi declined to comment.

A reversal of fortunes

One attempted capital-raise in question, the outcome of which has not been previously reported, was intended to be BlockFi’s Series E round in June 2021, with Prince setting the ambitious goal of raking in a whopping $500 million at a $4.5 billion valuation.

Prince shopped BlockFi to prominent crypto investors and traditional asset managers. Among them: Dan Loeb’s Third Point Management, under the strict condition BlockFi would go public or be acquired outright at a doubled $9 billion valuation. Another: Hedosophia of London, alongside a number of other high-profile venture capitalists.

The raise eventually closed at less than half of Prince’s target, at $225 million, without Third Point’s participation — albeit at the same valuation, sources said. A representative for Third Point declined to comment.

Reasons cited by sources for its derailment range from skittishness following BlockFi’s accidental bitcoin payouts just weeks earlier to the potential for future regulatory strife: One month later, state regulators in New Jersey, Texas, Alabama and Vermont ordered the startup to stop offering its interest-bearing crypto accounts in their respective regions.

Those accidental payouts refer to ‘fat-finger’ errors during peak bull market, which meant staking rewards were denominated in bitcoin (BTC) instead of dollar-pegged stablecoin GUSD, resulting in $10 million in mistaken transfers, according to Prince. Still, some users claimed to have received as much as 700 BTC ($28 million) instead of the intended $700.

At least one person was fired over the incident, according to two sources.

Still, the reduced Series E closed around three months after the startup brought home a $350 million Series D in March 2021, catapulting its valuation past unicorn status to $3 billion. BlockFi’s Series C, which closed in August 2020, valued the firm at $450 million.

Sources described BlockFi’s descent as a cautionary tale about tech startups that undergo exponential growth — but fail to buffer a balance sheet in preparation for an extended bear market.

But the threat of the bear was usurped by regulatory strife. Last November — one week after bitcoin peaked above a historic high of $69,000 — reports surfaced detailing the SEC’s beef with BlockFi’s interest-bearing crypto accounts, which the federal regulator deemed securities, echoing state watchdogs.

The SEC probe came as a blow to company morale, which sources categorized as slightly dented following the wrongful bitcoin payouts in May 2021, six months before the SEC showed up.

A settlement was reached in February 2022, with BlockFi agreeing to cough up $100 million in fines to federal and state regulators. The company also agreed to cease offering yield products to US retail investors — but not accredited institutions.

BlockFi has intended to register its interest-bearing accounts as securities, which would have given the go-ahead to roll out the product to US retail once more.

However, the move was delayed again as recently as late August, pending an audit, Blockworks has learned. Executives said they didn’t anticipate having more capital and less competition, according to a person close to the matter.

Internally, BlockFi employees said company leadership started spinning the SEC ordeal as a plus.

“The story was, ‘This is actually great, now we can be one of the first crypto companies to be registered with the SEC — we’re paving the way,’” one source said.

Despite the appeal of a potential SEC blessing, BlockFi, which had historically drawn around 70% of customer deposits from the US, weathered steady withdrawals.

The bigger downside?

Sources categorized the delay as a major contributor to the down round and a prerequisite for taking Bankman-Fried’s money — if only because mainstream venture capitalists would stay away.

A larger investor exodus ensued once BlockFi shut down accounts of US traders between February and March, roughly halving new sign-ups. BlockFi’s user deposits were, at peak last year, more than $10 billion — they briefly hovered at $8 billion before drying up to between $2 billion and $3 billion.

The decline was weighed by the crypto bear market, as digital assets shed nearly 60% of their value.

Series F to SBF

It’s clear Bankman-Fried’s cash injection — with the option to buy BlockFi outright — was an exclamation point on a rough and rocky 18 months for Prince’s firm.

Company insiders detailed a number of problems, ranging from a clunky tech stack powered by a relatively obscure programming language, Elixir (“writing a book in Latin”), to a mentality fueled by a relentless “number go up” attitude, focused on increasing customer deposits which double as liabilities.

“We were building with a bad tech stack which made us exponentially slower — slower to roll out products and updates than our competitors, and we had to hire more developers to compensate,” one source said.

BlockFi last year fired its chief technology officer, who joined in 2018. The firm also asked its chief growth officer to leave, sources said.

A number of other key employees have recently departed, including other growth and development leads and Mitch Port, vice president of strategy and finance.

Port took up an expert associate partner post at Bain & Company and declined to comment, outside of stating BlockFi was “an incredible company to work for with some of the most talented people I’ve ever worked with.”

Other executives are also on their way out, their own decisions, including David Olsson, Shane O’Callaghan and Samia Bayou. Key figures running the institutional side of BlockFi’s business remain, including Bank of America veteran Giles Colwell and Brian Oliver. Oliver joined in May, having spent a decade at private equity firm Red Devil Investors.

BlockFi had roughly 1,000 employees at most. And its growth trajectory moved the core of the company, in some ways, away from its crypto-native roots.

For instance, the firm’s most recent chief marketing and growth officers had no professional crypto experience, much like many new recruits — a shift deemed internally a good thing: Crypto outsiders would supposedly attract others of their ilk.

BlockFi sought liquidity — fast

Prince and other executives were buoyed in seeking a Series F at the tail end of 2021, with support from JPMorgan, by what they considered a covert ace: BlockFi’s interest-bearing accounts would soon be the first and only SEC-registered offerings, a status which would, in theory, attract retail investors en masse.

BlockFi initially sought to raise up to $500 million at a valuation between $6 billion and $7 billion (about 60% above its last round), sources said, but given the company was barred from servicing new US customers, it proved a difficult sell.

Staff were meanwhile told the company would soon go public. As negotiations dragged on, the would-be raise evaporated, eventually targeting a scant $85 million at a $1 billion valuation.

A qualifier of raising those funds was to cut 20% of staffers to bolster profits, which the company executed in June alongside the likes of Coinbase and Gemini.

BlockFi reassured staffers it was solvent, claiming it could’ve handled twice as many withdrawals throughout the market collapse of May and June, sources said. Customers pulled around 30,000 BTC ($568 million, now), 230,000 ETH ($292 million, now) and $1.5 billion in stablecoins between June and July, according to the company documents.

It’s not apparent just how close BlockFi came to the brink. But to its credit, the company never suspended withdrawals or other functionality during the widespread crypto reckoning. Sources dubbed the company a good, ethical actor stuck in an impossible situation. The acquisition-hungry and crypto-savvy Bankman-Friend would not have invested otherwise, so the argument goes.

Competitors Celsius and Voyager both floundered under the weight of cascading margin calls and tumbling prices, as mass withdrawals from a panicked market rendered both firms bankrupt and tens of thousands of users out of pocket to this day. Users took to social media to vent about a lack of communication and livelihoods hanging in the balance.

BlockFi has taken the opposite tack. The company could’ve — hypothetically, in a real pinch — sold its institutional customers’ collateral to service withdrawals, although such extreme measures would’ve surely upset its wealthy clientele.

Regardless, the looming threat of unmanageable withdrawals only made raising cash all the more pressing.

Selling BlockFi around the block

On Friday, June 10 — three days before BlockFi laid off 20% of its staffers — the New York-based Prince’s phone rang with a crucial 9:00 am notification: “Ping major investors,” coupled with a board meeting two hours later.

A week-long gauntlet of meetings were set to ensue, starting Sunday at 10:30 am with a 30-minute call with Kyle Davies and Su Zhu, co-founders of now-bankrupt crypto hedge fund firm Three Arrows Capital, alongside Brian Oliver (BlockFi’s general manager of institutions), as well as additional BlockFi executives.

Four days later, BlockFi said it had liquidated all of Three Arrows Capital’s positions.

Aside from private slots, the only scheduled meetings absent are a week-long series dubbed “Project Batman,” involving Prince, Amit Cheela (BlockFi’s senior vice president of finance), Matthew Chan (BlockFi’s corporate development strategist) and a number of JPMorgan fintech-focused investment bankers.

Wednesday, June 15

- 8:30 am: Mark Yusko (Morgan Creek, CEO)

- 9:30 am: Tony Lauro (BlockFi, CFO); Flori Marquez (BlockFi, co-founder); Jonathan Mayers (BlockFi, general counsel)

- 6:15 pm: Robby Gutmann (NYDIG, CEO; Stone Ridge, head of digital asset strategies); Ross Stevens (Stone Ridge, CEO); Marquez (BlockFi, co-founder)

Thursday, June 16

- 9:00 am: Marquez (BlockFi, co-founder); Lauro (BlockFi, CFO); James Fitzgerald (Valar Ventures, founding partner); Andrew McCormack (Valar Ventures, founding partner)

- 10:30 am: Yusko (Morgan Creek, CEO)

Friday, June 17

- 2:45 pm: Richard Chang (capital markets lead, FTX Ventures)

- 4:00 pm: Barry Silbert (Digital Currency Group, CEO)

Saturday, June 18

- 12:00 pm: Gutmann (NYDIG, CEO; Stone Ridge, head of digital asset strategies); Stevens (Stone Ridge, CEO); Fitzgerald (Valar Ventures, founding partner); McCormack (Valar Ventures, founding partner); David Heller (investor, former Goldman Sachs executive)

- 3:30 pm: Chris Ferraro (Galaxy Digital, CIO)

- 6:00 pm: BlockFi legal team

- 8:00 pm: Thomas Farley (Bullish, incoming CEO)

Sunday, June 19

- 8:30 am: Bankman-Fried (FTX, CEO); Caroline Ellison (Alameda Research, CEO); Ramnik Arora (FTX, head of product)

- 9:00 am: Brian McGrath (Ribbit Capital, general partner)

- 1:00 pm: Peter Briger (Fortress, principal), Mayers (BlockFi, general counsel)

- 2:00 pm: Cheela (BlockFi’s senior vice president of finance); Ellison (Alameda Research, CEO); Arora (FTX, head of product); Bankman-Fried (FTX, CEO); Mayers (BlockFi, general counsel)

- 5:00 pm: Cheela, Phil Rich (Binance, mergers and acquisitions); Kaiser Ng (Binance, senior vice president of finance); Ken Li (Binance, mergers and acquisitions); Michael Chan (Binance, head of mergers and acquisitions)

- 6:00 pm: BlockFi board meeting with three Haynes Boone attorneys (BlockFi’s external law firm)

- 8:00 pm: Cheela, David Merin (ConsenSys, head of corporate development), Matthew Gilmour (ConsenSys, corporate development associate)

Monday, June 20

- 8:30 am: Gavin Michael (Bakkt, CEO)

- 9:00 am: Howard Chen (JPMorgan, co-head of market infrastructure); Dan Pombo (JPMorgan, head of restructuring); Jeremy Sipzner (JPMorgan, executive director), Xavier Loriferne (JPMorgan, managing director, mergers and acquisitions); Keith Canton (JPMorgan, head of private capital markets)

- 9:30 am: Peter Smith (Blockchain.com, CEO)

- 4:00 pm: Tom Jessup (Fidelity, digital assets president)

- 5:00 pm: Marshall Beard (Gemini chief strategy officer)

- 6:00 pm: FTX executives

Tuesday, June 21

- 9:30 am: Marquez (BlockFi, co-founder); Lauro (BlockFi, CFO); Frederik Mijnhardt (SecFi, CEO)

- 11:00 am: All-hands BlockFi meeting to announce FTX bailout

- 11:30 am: Bloomberg journalist

While it’s not clear whether every scheduled call took place in the end, with all attendees present, Prince lined up meetings with major players from Binance, Ribbit Capital, ConsenSys, Fidelity, Bakkt and Gemini, in between a number of calls with Bankman-Fried and Alameda’s Ellison.

One source described the all-hands in which Prince revealed the bailout: “Zac comes in and tries to sell the SBF deal, cussing and swearing — no longer in corporate mode. He said, ‘This is freaking awesome, this is amazing,’ and, ‘Nobody else could do this, but we did it.’”

Prince claimed the bailout was better than a Series F, as they didn’t have to give up equity.

One month later, BlockFi offered 80% to 90% of the remaining staff (about 700) voluntary severance packages worth 10 weeks of pay. Some 200 accepted, per a source. The company now has between 400 and 500 staffers.

Some remaining staff were offered a separate, more complicated deal: 10% raises, with the potential to receive up to 20% of salaries in 6 months — if divisions met new, more-stringent metrics.

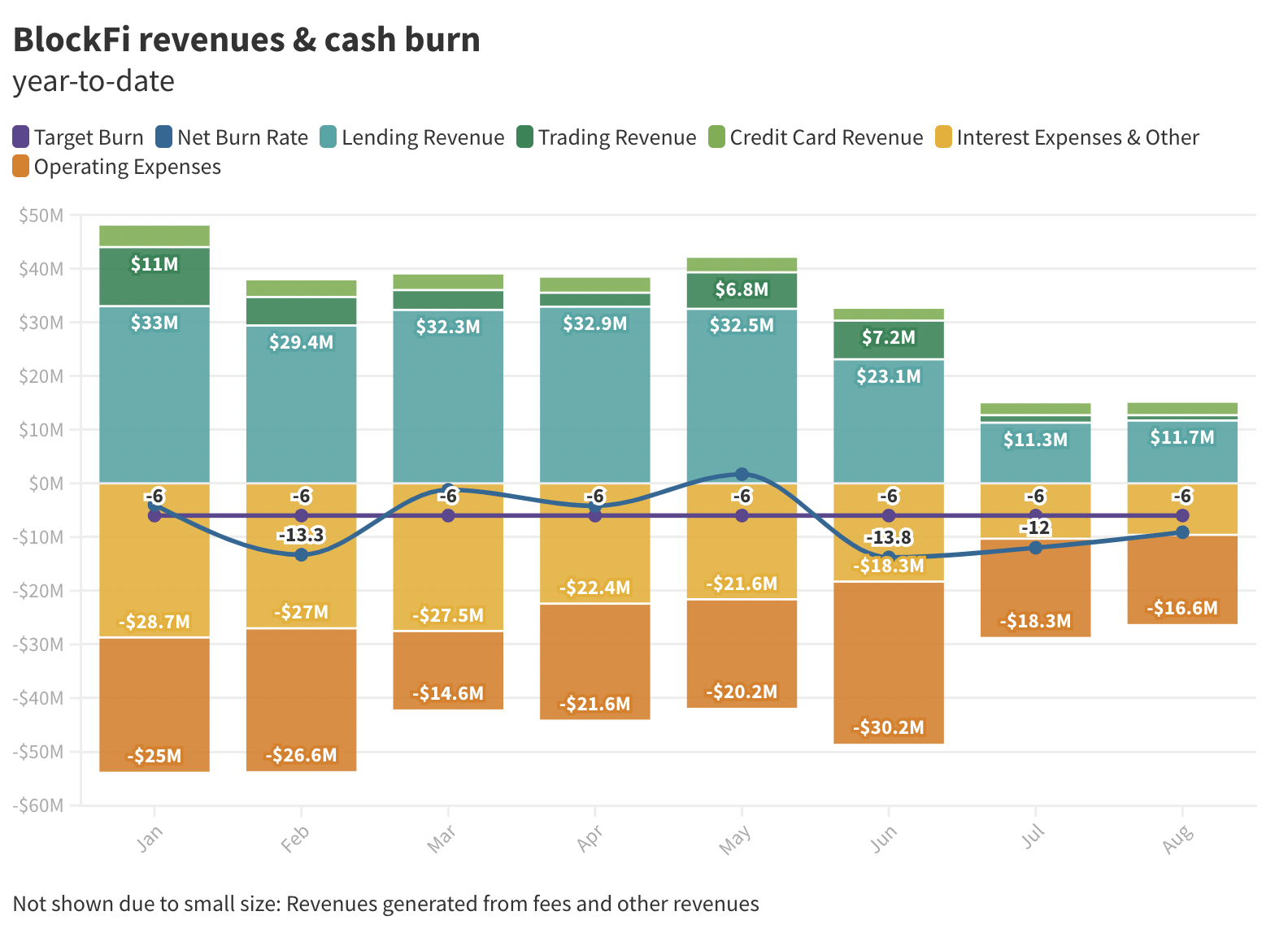

Those metrics included boosting the value of private client deposits in interest-bearing accounts by 40% by the end of January to $3 billion, as well reducing cash burn below $6 million by year-end.

Indeed, BlockFi, like many of its startup peers stuck in growth-mode, has rarely recorded net positive cash flows. The firm’s operating cash flow was in the red by $13.8 million in June, its worst month this year, and negative by $12 million in July and $9.1 million in August — averaging $7 million per month in 2022 — according to an internal document.

The documentation also showed BlockFi’s operating cash burn was positive just one month this year: May, good for $1.7 million in the green, an especially optimistic, hopeful showing.

BlockFi’s cash burn this year through August: $55.9 million in the red.

What does integrity cost, really?

What’s next for BlockFi today is far from certain. A number of prominent crypto players, while declining to talk on the record, praised their efforts and their integrity — and especially noted their willingness to dive headlong into alternative income streams, rather than doubling down on what didn’t work.

“Look, would I want to be BlockFi? No,” one source said. “The [execs] have made plenty of money. They could have cashed out and closed up. They could have exploited their investors. What they chose to do, and hopefully what they are still doing, is much harder.”

Adding fuel to the fire: the implosion triggered by stablecoin Terra’s depegging, alongside the crumpling of rival crypto lenders Celsius and Voyager. BlockFi monthly revenues dwindled to $15 million by July and August — a 70% drop from the start of the year.

The firm in January raked in $48 million between its lending ($33 million), trading ($11 million) and credit card ($4 million) income streams.

In both July and August, BlockFi attracted $15 million of monthly revenue across its three primary offerings, with lending making up close to 80%. Overall, it was less than half what the firm brought in during June’s $32.5 million.

BlockFi’s credit card has proven more resilient than its trading, generating up to $2.3 million per month of late, down from $4 million in January. Trading only amounted to $1 million in August, down from $6.8 million and $7.2 million in May and June, respectively.

The firm now hopes establishing international fiat on-ramps and Stripe payment support can help revive those numbers, alongside offering crypto derivatives to its institutional customers, per internal documents and sources. A spokesperson for Stripe declined to comment.

Although, such an integration wouldn’t exactly mean an explicit partnership with the payments giant, moreso BlockFi would be a customer alongside the likes of FTX and Coinbase.

Incorporating FTX custody services and launching derivatives products for institutions have also been floated, alongside campaigns to winback withdrawn customer deposits. BlockFi has targeted lending and trading revenue specifically as primary avenues for growth.

BlockFi’s US licenses, which take a long time to receive, seem the primary prizes for Bankman-Fried, along with its rock-solid institutional business.

Most company employees are still waiting to hear about what happens to their equity, one source said. It will likely morph into FTX equity, but under different and unknown fundamentals.

In a concerted effort to retain staff, BlockFi recently boosted the weight of its retention goals tied to the offered bonus packages — from 40% to 80% — reducing the importance for customer deposits and cash burn rate.

It’s not totally a happy story, the crescendo of BlockFi’s meteoric ascent, one that saw co-founders Prince and Marquez briefly transcend digital assets, beyond fintech and into wider tech nirvana, complete with conference circuits and mainstream TV appearances.

One could glean many a lesson from the BlockFi saga thus told, be it, “Don’t fly too close to the sun,” to “Customer deposits are a terrible growth metric for crypto lenders,” or, “Don’t lend cryptocurrency to Su Zhu and Kyle Davies.”

But, maybe, it’s this simple…

“Never accidentally send bitcoin instead of a stablecoin.”

Michael Bodley contributed reporting. Updated at 3:41 pm, ET to correct denomination of burn rate.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- Empire: Crypto news and analysis to start your day.

- Forward Guidance: The intersection of crypto, macro and policy.

- 0xResearch: Alpha directly in your inbox.

- Lightspeed: All things Solana.

- The Drop: Apps, games, memes and more.

- Supply Shock: Bitcoin, bitcoin, bitcoin.