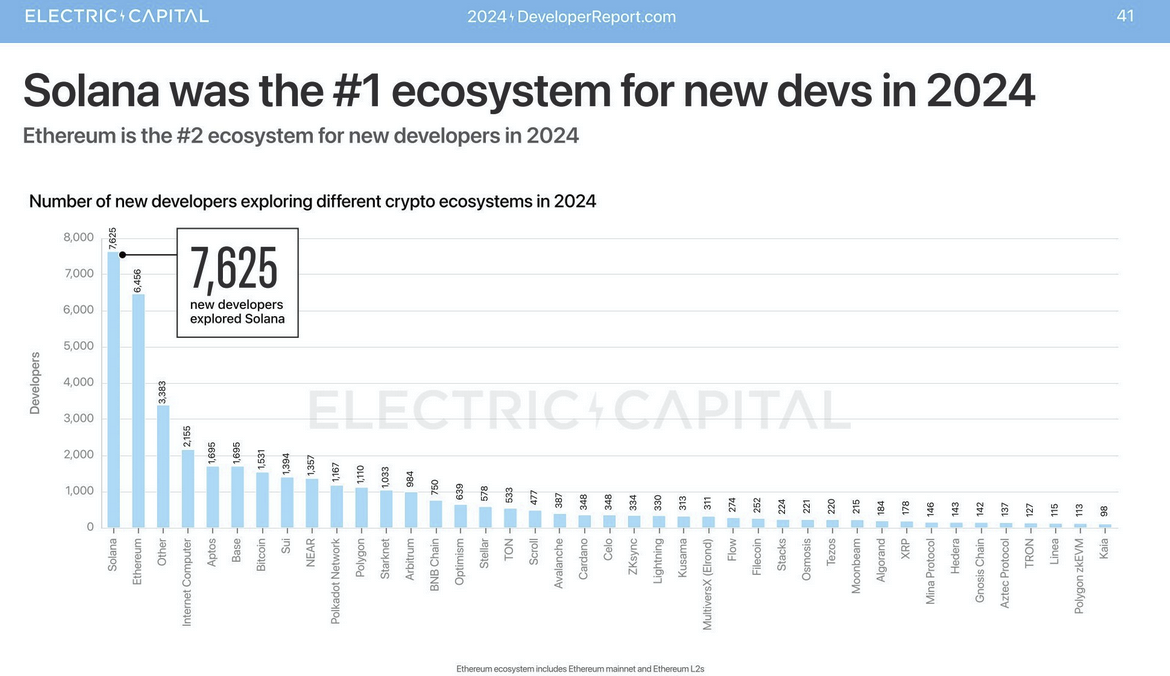

Solana gained highest share of new devs in 2024: Electric Capital

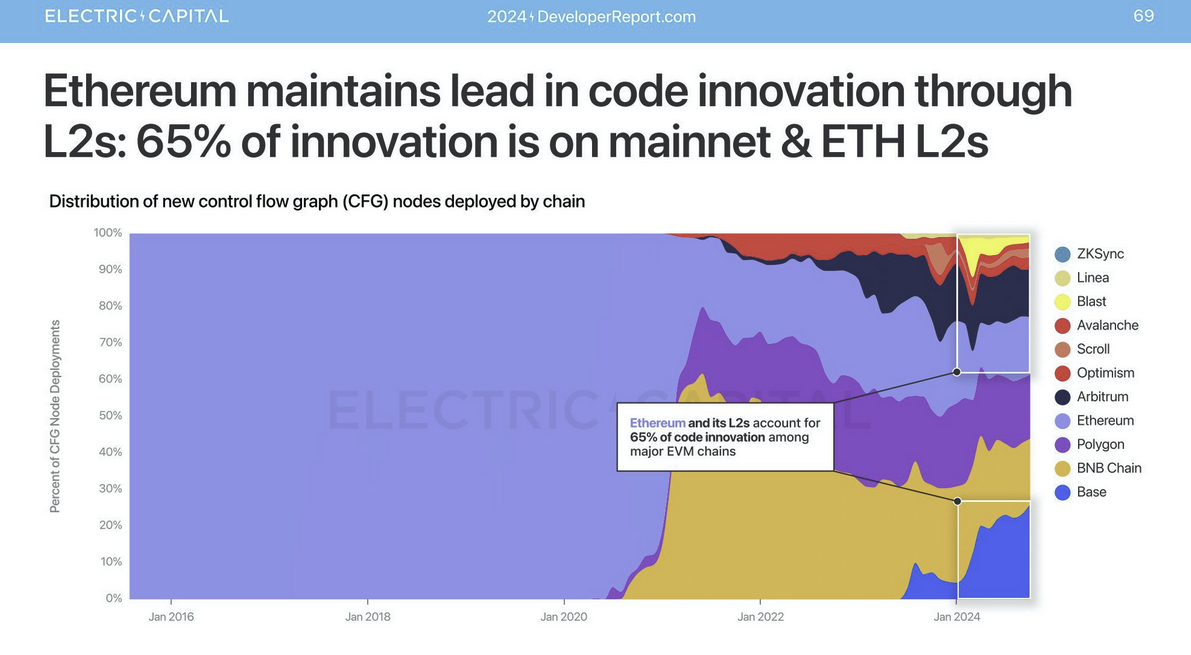

EVM remains the most active tech stack with the most code innovation

Kolonko/Shutterstock modified by Blockworks

If developer mindshare is any indication of innovation, then knowing something about developer activity matters.

It’s why the industry pays attention when Electric Capital releases its annual developer report.

As of November 2024, crypto had about 23,613 monthly active developers, a sliver (0.0875%) of the 27 million population of global software devs. It’s an impressive 2000% increase over the last decade, but numbers are still down from the industry’s highs of about 31,000 in 2022.

One notable trend among crypto developers is the increasingly global distribution of talent today compared to years past. In 2015, 80% of devs worked out of North America and Europe. Today, both continents have seen their share of developers decline to 24% and 31%, respectively, while Asia now leads with 32% of developer mindshare.

Read more: The Solana ecosystem has a lot to be thankful for this year

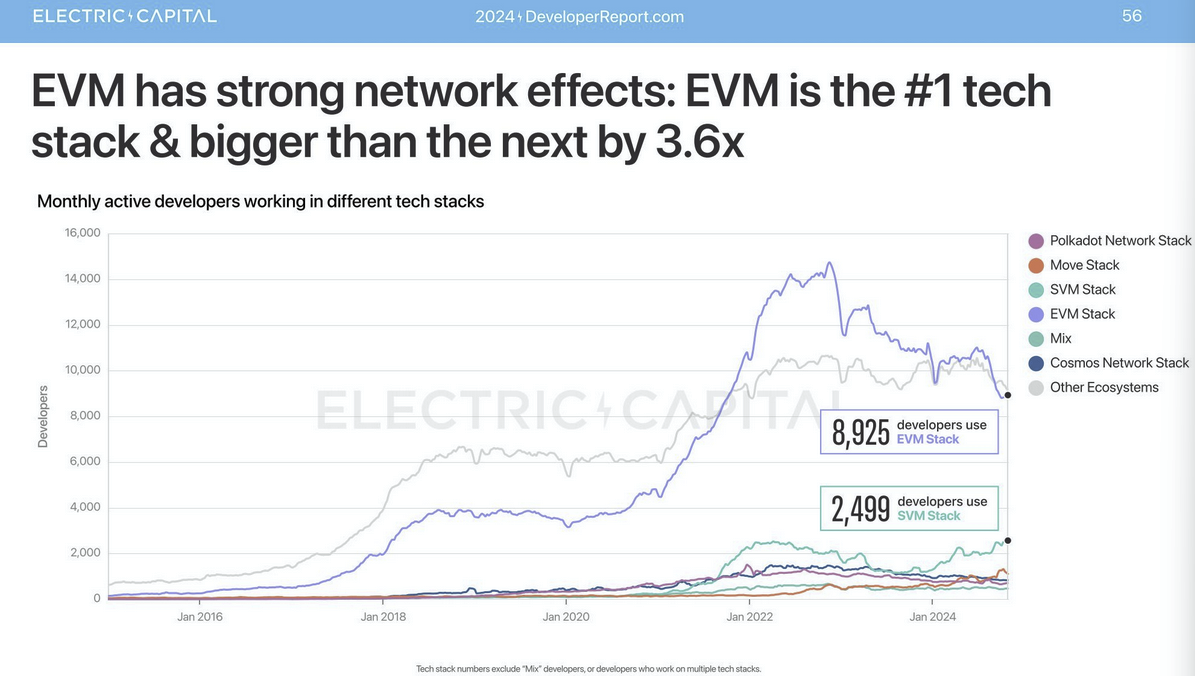

The Ethereum Virtual Machine (EVM) remains the leading tech stack, boasting a robust network effect with 8,925 developers — roughly 3.6 times the size of the Solana Virtual Machine (SVM) stack, which has 2,499 developers.

What stands out however, is Solana coming in as the number one ecosystem for new developers over the past year. This is an impressive lead, especially considering that Ethereum — which is a close second in attracting new developers — is bolstered by an ecosystem that includes dozens of layer-2 rollups.

Solana developers dominate in India, accounting for approximately 27%. Notably, it is the only country where new developers are joining the Solana ecosystem at a higher rate than they are any other blockchain. India also ranks second in developer share, trailing only the US.

Read more: Electric Capital finds veteran Web3 devs are on the rise

The highest developer activity doesn’t always directly translate to code innovation. For this reason, the Electric Capital developer report also considered which chains have the most new code written.

Ethereum maintains its lead with about 65% of new code written across its layer-1 and layer-2 ecosystems.

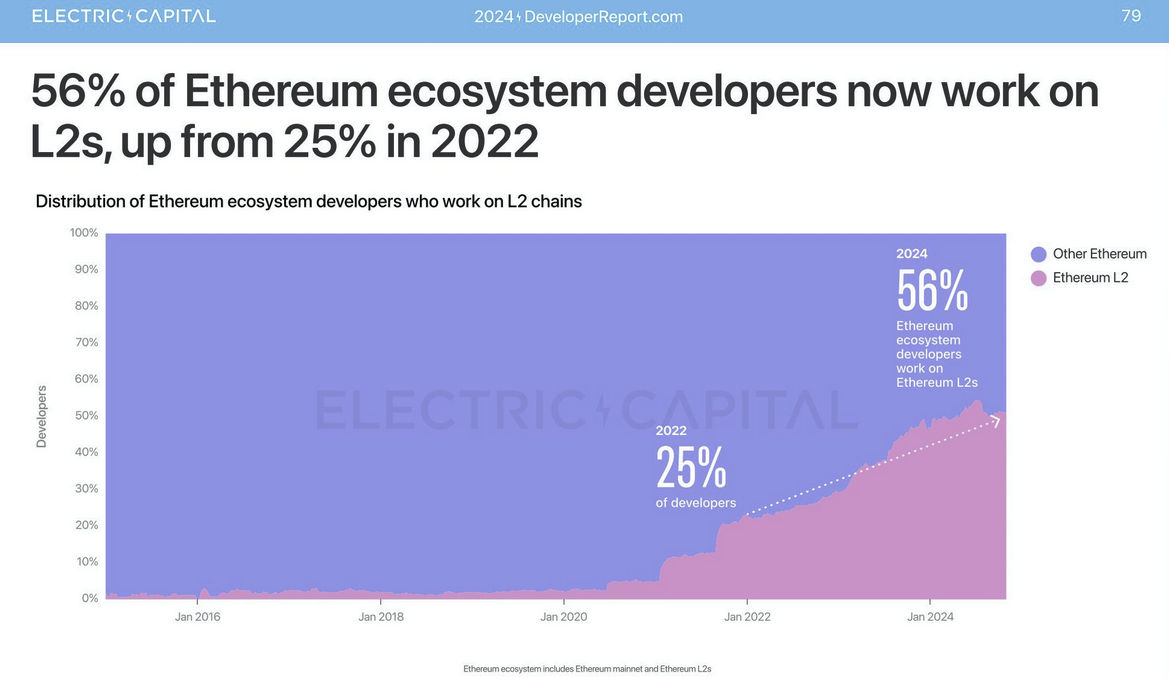

According to the report, liquidity isn’t the only thing fragmenting in Ethereum — scarce developer talent is too. Since Ethereum adopted its rollup-centric roadmap, the share of developers working on layer-2s has grown from 25% to 56%.

Out of all active layer-2s, Base has the largest active developer base of 4,287, followed by Arbitrum (3,450), Starknet (2,548), Optimism (2,416), Scroll (1,517) and zkSync (1,115).

If developer activity is any indication of increased chain activity, Starknet’s developer lead is perhaps somewhat surprising, especially in contrast to an older chain like Optimism. Based on transaction count, Starknet’s activity has languished in comparison over the past year.

Source: Growthepie

Source: Growthepie

What about Bitcoin?

The Bitcoin network has about 1,200 monthly active developers; a number that has stayed fairly constant over the last 12 months.

Yet with the rise of Bitcoin layer-2s, NFTs and various scaling solutions, at least 42% of bitcoin developers are now dedicating their efforts to those areas.

Finally, zero-knowledge developers saw a slight reduction. Today, there are 2,054 monthly active developers working in zk. About 823 of them hold full-time positions.

Yet, zk contract deployments grew from a mere 40 in 2020 to 639 in 2024, with the largest share coming from Ethereum, Base and Optimism.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.