ETH as money? Exploring ether’s unique role

Ethereum Foundation researcher Mike Neuder argued that ETH can serve as a secure, global currency

Akif CUBUK/Shutterstock modified by Blockworks

Ethereum circles are endlessly debating whether ETH should be seen as “money” in the same way bitcoin is embraced as a commodity currency.

In a Devcon talk Thursday, Ethereum Foundation researcher Mike Neuder laid out his case for ether’s foundational attributes both as a permissionless and programmable asset, and as a resilient form of decentralized money. Neuder explored how ETH can serve as a secure, global currency— one with intrinsic safeguards for property rights, censorship resistance, and self-sovereignty across the multi-layered Ethereum ecosystem, eventually including its rollups.

To explain Ethereum’s “permissionlessness,” Neuder referenced Hayek and Friedman on property rights, emphasizing the unique ownership Ethereum provides to holders of ETH being permissionlessly transferable, storable, and programmable.

To distinguish ether from assets whose access can be limited by third parties, Neuder included a critique of centralized stablecoins such USDC and USDT, noting that despite their similar programmability, they lack true property rights. Issuers can, and do freeze funds. For Neuder, this capacity marks ETH as a distinct asset within onchain finance.

A pivotal part of Neuder’s presentation highlighted the expanding property rights of ETH across layer-2 rollups.

But there’s a caveat: Rollups haven’t yet reached a Stage 2 decentralization classification. Once they do, they will allow users to bridge ETH in and out, permissionlessly, maintaining Ethereum’s property rights.

The ability to force withdrawals ensures that users can always reclaim their assets even if a rollup’s sequencer, or central operator, attempts to censor or disrupt transactions. It’s a core feature of what it means to be a layer-2 network. Arbitrum One and OP Mainnet have already reached Stage 1.

Neuder detailed Ethereum’s commitment to this mechanism as a way to enhance scaling while protecting users’ autonomy in Ethereum’s rollup-centric strategy.

The talk also addressed Ethereum’s inflation model compared to other cryptocurrencies, situating it alongside Bitcoin as an increasingly “sound” currency.

Since Ethereum’s transition to proof-of-stake in the 2022 Merge, supply growth has significantly slowed, with inflation sitting near 0.9%. This is comparable to Bitcoin’s current 0.8%, which it will maintain until the next halving in 2028. Ethereum achieves this balance through a combination of issuance, staking rewards, and an ETH burn mechanism that fluctuates with network demand, effectively absorbing inflationary pressures during periods of high transaction volume.

Neuder argued that this adaptive model is crucial for long-term security, contrasting with Bitcoin’s fixed supply cap, which may pose challenges for future network security once block rewards vanish.

In response to a question about the stability of the ether issuance curve, Neuder acknowledged that adjustments to issuance rates over time — from changes to the block reward under proof-of-work, to current proposals of tweaking the curve — have sparked ongoing debate over the importance of maintaining “strong assurances” regarding ether’s total supply.

While Neuder noted that altering the curve could offer benefits — such as averting risks associated with high staking rates or the emergence of a dominant liquid staking token (LST) — he cautioned that frequent changes might undermine confidence in stability.

This uncertainty could in turn impact “credible neutrality,” another core value vital for Ethereum’s long-term resilience. Assessing the long-term trade-offs will require careful analysis, ideally involving input from macroeconomists, Neuder said.

Source: Mike Neuder

Source: Mike Neuder

One crucial component of Ethereum’s deflationary mechanics is the blob burn effect resulting from layer-2 activity. Ethereum rollups post transaction data to the Ethereum mainnet in “blobs” — bundles of data stored efficiently to reduce costs. As these blobs are published on the mainnet, they incur fees, a portion of which is burned, contributing to the overall ETH burn. This design enables Ethereum to absorb more L2 transaction activity without overwhelming the base layer, maintaining lower L1 gas fees.

As L2 usage grows, so does the blob burn effect, intensifying Ethereum’s deflationary pressure during periods of high activity, such as we are seeing this week.

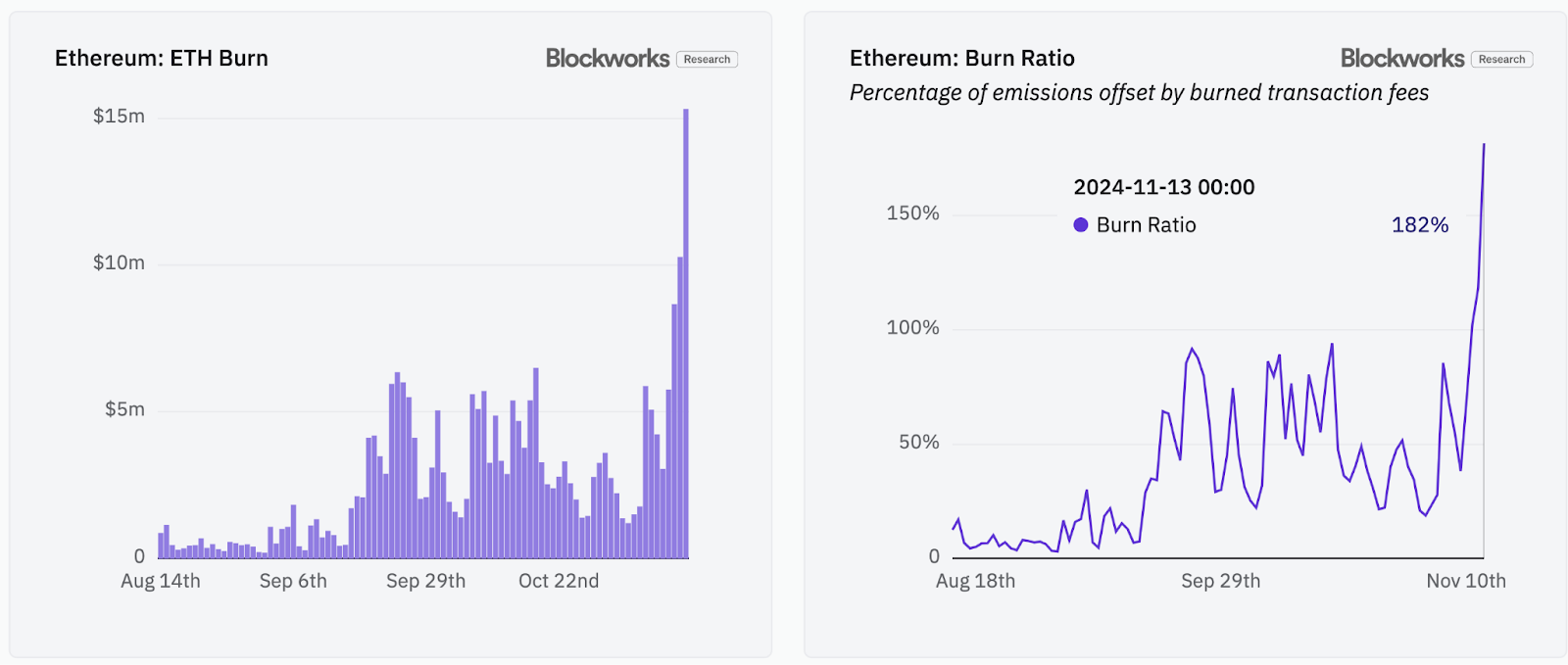

Source: Blockworks Research

Source: Blockworks Research

The total dollar value of ETH burned, over time, spiked dramatically beginning in early November to nearly $15 million. This increase in burned ETH is due to heightened network activity, as transaction fees contribute to the burn rate. As a ratio, the burn ratio reached 182%, resulting in a net reduction of ETH supply in recent days.

Some within the Ethereum community prefer to de-emphasize the role of ether as “sound” money, or even dismiss it outright.

For instance, Ethereum co-founder Vitalik Buterin tends to discuss Ethereum’s value in terms of its programmability, flexibility, and commitment to decentralization rather than focusing on ETH as a purely monetary asset.There’s a balance to be struck, and Neuder underlined Ethereum’s prime aim, to retain credible neutrality and censorship resistance, positioning ETH as a form of digital money grounded in the ethos of self-sovereignty.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.