On the Margin Newsletter: Reading the FOMC meeting tea leaves

With the CPI having landed on the same day as last month’s FOMC meeting, there’s a lot to be learned from the meeting minutes

Federal Reserve Chair Jerome Powell | Brookings Institution/"Jerome Powell" (CC license)

Today, enjoy the On the Margin newsletter on Blockworks.co. Tomorrow, get the news delivered directly to your inbox. Subscribe to the On the Margin newsletter.

Today’s On the Margin Newsletter is brought to you by the Canadian working on this holiday, Felix Jauvin. Happy Fourth of July!

Today’s shortened edition will dive into the key takeaways from the Federal Open Market Committee’s minutes released yesterday.

June’s FOMC scoop

As usual, the release of last month’s FOMC meeting minutes on Wednesday provided a stale look at how committee members came to the decisions they made in June.

If you rewind the clock, you may remember that the last FOMC day was a weird one as we received the latest CPI readings only a few hours before the actual meeting outcome was announced.

Inflation came in soft and led many to speculate how much of that print was baked into their decision-making process.

So, I dug into the minutiae of the minutes. Here’s some notable things I found interesting:

Conflicting inflation prints

Some participants noted that despite a significant decline in inflation during the second half of 2023, there had been less progress than in early 2024. The May CPI reading provided some evidence of (modest) further progress, with monthly changes indicating improvement across various price categories, including market-based services.

AI productivity gains

For the first time, the FOMC acknowledged the potential for AI to be a boon to productivity and work as a deflationary force:

“Participants highlighted a variety of factors that were likely to help contribute to continued disinflation in the period ahead… or the prospect of additional supply-side improvements. The latter prospect included the possibility of a boost to productivity associated with businesses’ deployment of artificial intelligence–related technology.”

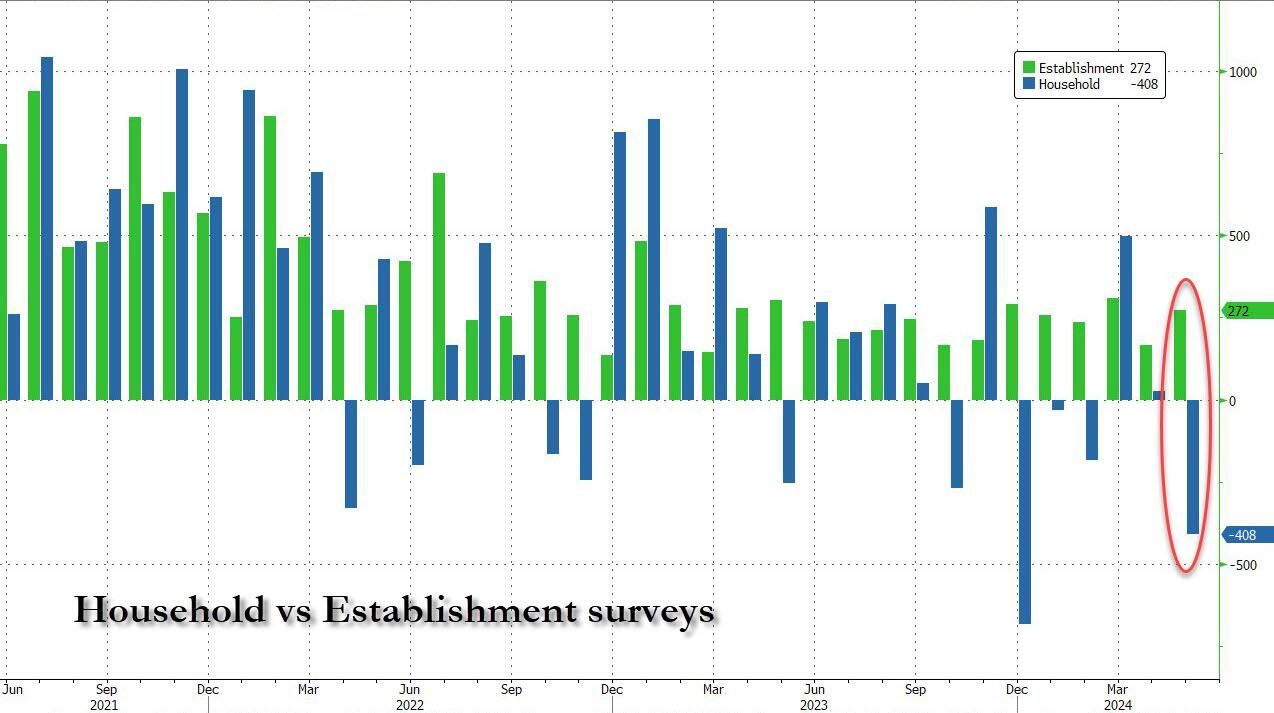

Broken labor surveys

There’s been a lot of talk about how the establishment survey has been overstating jobs gains compared to the household survey. Historically, the two are much more in line than they have been since 2022:

Interestingly, FOMC members are beginning to acknowledge that jobs gains might be overstated: “Several participants also suggested that the establishment survey may have overstated actual job gains.”

This is fascinating. It’s very rare to see FOMC members acknowledge that they’ve been looking at data that might be inaccurate. Further, it could mean that they’ve been more hawkish on the labor market than they should have been. This, paired with the dynamic that most job gains have been within part-time jobs whilst the economy keeps losing full-time jobs, could mean that the labor market is a lot colder than they thought.

Overall, these FOMC meeting minutes represent an outdated perspective on the economy that is no longer as relevant. Especially right now when it feels like we’re undergoing a bit of a regime shift in the economy. That said, I still found it generally dovish in terms of what they were looking at and discussing, especially in light of all the soft economic data we’ve received since.

Have a great long weekend all! We’ll talk on Monday.

— Felix Jauvin

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.