What Is Tokenomics? The Investor’s Guide

Tokenomics explains why any digital asset has value — it is essential to building an investment thesis

Graphic by Crystal Le

To an outsider, the word “tokenomics” can evoke images of a wholesome gear box in an arcade token machine. But for the crypto native, it is an emergent science for studying a new asset class that often fits somewhere between a currency and a security. It blends monetary policy with company valuation models and can cast a shadow of suspicion as some integrate so-called ponzinomic elements.

This investor’s guide to tokenomics will provide a deeper analysis of this new field of study. Readers will learn what exactly tokenomics is, the key attributes of tokenomics, and several green and red flags when analyzing different projects. The following article in this series will explore the dark side of tokenomics and explain how to identify the predatory tactics of token issuers and their often conspirators of venture capitalists.

What is tokenomics?

Tokenomics, short for token economics, is the science that explores the elements that make a cryptoasset valuable. It studies the relationship between an asset’s supply, inflation rate, distribution, utility and accessibility to analyze and predict its success.

Projects typically include great detail in the philosophy of their tokenomic model to persuade potential investors. Best-practice opinions differ on issues such as issuance schedules, use cases and staking incentives, but the goal is (with some exceptions) to create a favorable outcome for most token holders.

Understanding the first tokenomics model: Bitcoin

Because it was the first, the Bitcoin white paper is the industry guide stone to this topic. It offered a rubric for later projects to follow and iterate. Its simple tokenomics model is categorized into three components: supply, distribution and utility.

Supply

The leading cryptocurrency has a maximum supply of 21 million coins. Miners receive freshly minted coins as an incentive for producing transaction blocks, while users pay a fraction of their transfer amount as network fees. The fees discourage spam transactions and provide an additional revenue source for miners even when Bitcoin’s block rewards dry up.

Distribution

Bitcoin’s distribution follows a predictable and code-enforced schedule. Miners receive new coins approximately every ten minutes with each newly mined block, while the reward reduces in half every 210,000 blocks (roughly four years). Unlike Ethereum and later ICOs, no premine or presale was allocated to early insiders. Every token in existence today has been mined.

After four successful halvings that have seen Bitcoin’s block rewards drop from 50 BTC, 25 BTC, 12.5, and now 6.25 BTC, the number of newly circulating coins continues to dwindle. Yet, the certainty of future halvings means that the entire Bitcoin supply will not go into circulation until sometime around 2140. This built-in economic scarcity makes BTC attractive to investors and has been a vital driver of Bitcoin’s growth over its existence.

Utility

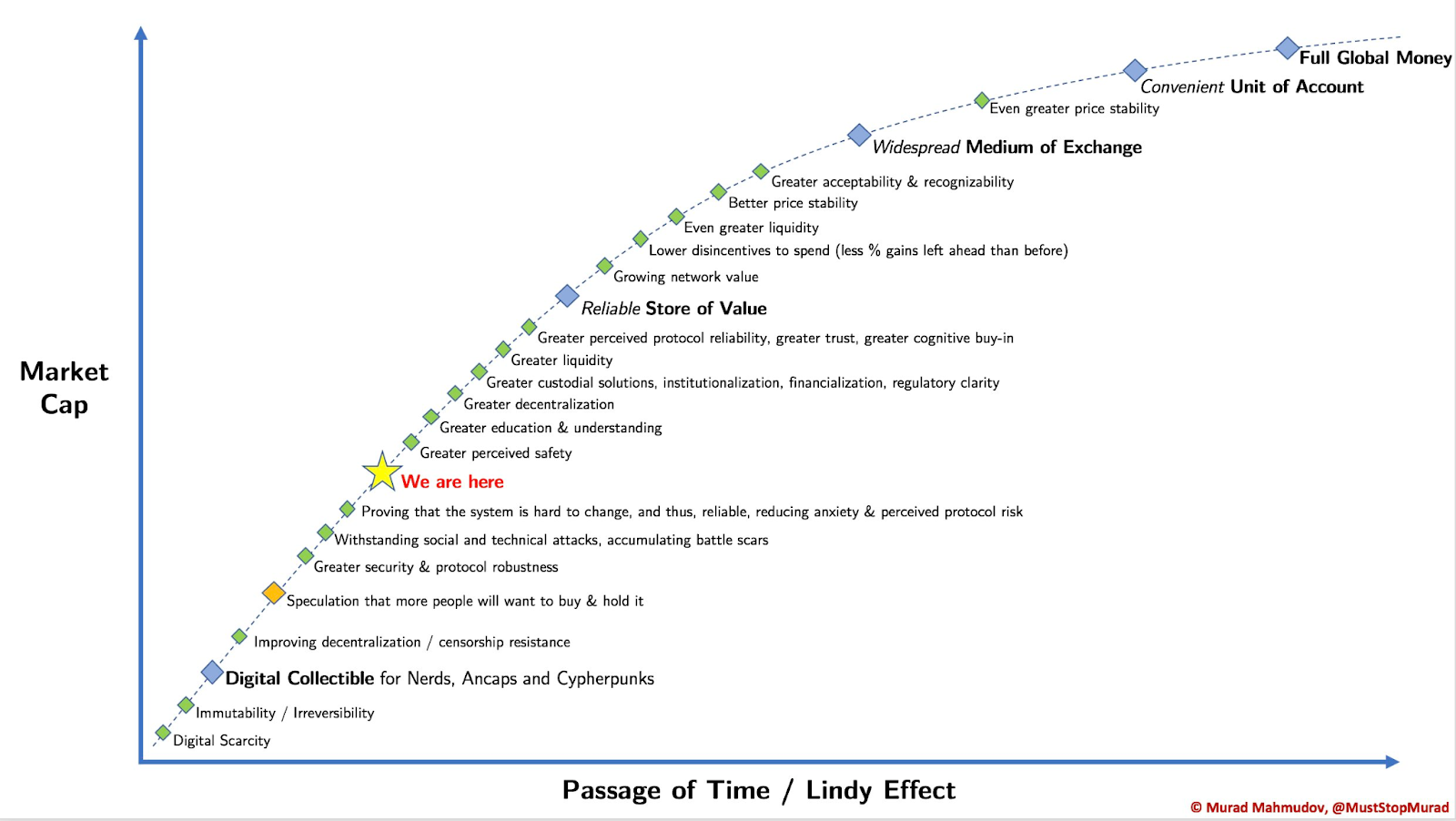

The Bitcoin white paper states that the token’s utility is intended to be peer-to-peer digital cash. However, nothing in its tokenomics directly forces or incentivizes that use case. Since the token has no formal governance structure and development is mainly crowd-sourced and decentralized, its transaction throughput has yet to evolve to meet the complete demand of that use case. Instead, user behavior treats it more like a censorship-resistant digital store of value than a currency.

Many believe that the decentralized and organic development and adoption of bitcoin will inevitably transform it into digital cash. The bitcoin advocate Murad maps the trajectory in his version of Bitcoin’s Lindy Effect:

With this tokenomics meaning and example in mind, the following section explains why it is essential for investors to understand tokenomics. It also considers why project teams must implement the proper token mechanics.

Why is tokenomics important?

Tokenomics plays a defining role in the success or failure of a cryptocurrency project. A fundamental way it does this is by shaping an investor’s perception of a cryptocurrency’s market value. For instance, the idea of a scarce asset resonates with many experienced investors.

Many investors consider tokenomics to be one of the most critical factors when evaluating a crypto project. A project with a failed tokenomics structure could struggle to gain traction even if it has the most innovative product or development team. It is often easy to discern whether a cryptocurrency project would succeed by carefully examining the different features of its tokenomics model.

Core tokenomics features

The fundamental idea behind creating a token is to bring value to most holders. Striking a perfect balance between the different features listed below makes it easier for projects to achieve the desired outcome.

Feature 1: Token supply

Most cryptocurrencies have a maximum supply, referring to the hard cap on the number of coins or tokens that will ever exist. During the initial release, a portion of a token’s maximum supply goes into circulation and is thus referred to as the “circulating supply.” The release of more coins into circulation sometimes follows a transparent and predictable schedule. But projects can often delay their unlocking roadmap with little justification. We explain how this pattern can turn predatory in our next article on bad tokenomics.

Many factors, including the project’s fundamental product and objectives, determine the maximum token supply. For instance, layer-1 blockchain projects that offer smart contract functionality often choose a relatively large supply to ensure enough for different ecosystem use cases, such as staking. At the same time, the token remains a viable unit of account.

For investors, comparing the maximum token supply and the circulating supply provides a quick way to determine whether a token is worth holding. It is common for a token with a high maximum supply and low circulating supply to drop in value as the release of new tokens dilutes the concentration of the total supply. This pattern is explained in greater detail in the following explainer.

Feature 2: Token utility

The number of stated and achievable use cases for a token within a crypto project’s ecosystem contributes immensely to its market value. Some standard token utilities in crypto include:

- Serving as a means for users to access exclusive benefits on the platform (lower trading fees, discounts on purchases, participating in new token sales, etc.)

- Serving as a means to incentivize miners or validators for maintaining security and verifying transactions on the underlying blockchain. Users also pay fees to transfer assets between addresses.

- Providing a way for token holders to govern the protocol by voting on critical decisions.

- Rewarding active users and new depositors with tokens through a liquidity mining program or gamified mechanism, as used in Web3 games.

Use cases drive demand for an asset when speculation fades. It also increases investor confidence that the asset’s value will continue to grow as long as the offered product or technology onboards new users.

Feature 3: Token distribution

This tokenomics feature focuses on how the token’s supply is distributed to different stakeholders. Stakeholders typically fall into three categories: large institutions, retail investors, and the founding team.

Most cryptocurrency projects fall into the category of pre-mined tokens. The founding team creates the tokens and sells a portion of the supply to early investors (usually venture capital firms) to raise funds for building the product. Popular cryptocurrencies such as ether (ETH), binance coin (BNB), and solana (SOL) are prominent examples of pre-mined tokens.

Investors investing in pre-mined tokens must be wary of the token distribution across different holders. A large concentration among early-stage institutional buyers without a carefully crafted release schedule could result in a downtrend in the token’s value when these holders exit their position at a significant profit.

The same principle applies to the portion of tokens allocated to the core project team. Investors prioritize investing in tokens where the core team receives a moderate allocation of the total supply and shows “skin in the game” by following a long-term vesting schedule for allocated assets.

Fair launch token distribution

Meanwhile, other projects take a fair launch approach where a significant amount of the supply is distributed to investors that meet certain criteria. For instance, Uniswap’s UNI token was initially airdropped to investors who had used the decentralized exchange before the token release. Another fair launch method is opening up the token sale to retail and institutional investors so that everyone buys in at the same price.

An efficient token distribution model ensures a reasonably fair release schedule and an ideal allocation to stakeholders. It also eliminates or reduces market fears around possible hyperinflation in the circulating token supply that will dilute the value of assets held by participants.

Feature 4: Token inflation

Introducing a deflationary mechanism is another way cryptocurrency projects drive long-term value for investors. The opposite of inflation, the goal of a deflationary token supply is to reduce the token’s total supply and make circulating tokens worth a lot more.

Coin burning — permanently removing tokens from the maximum supply — is the most prominent way most cryptocurrencies achieve deflation. Leading cryptocurrency company, Binance, spends 20% of its quarterly profits on buying back and burning its BNB supply.

Ethereum implements a different approach, burning a portion of ETH transaction fees paid by network participants. Still, other projects like Nexo (NEXO) perform periodic token buybacks, temporarily reducing the circulating supply. These assets vest for one year and are subsequently used by the platform to pay interest on customer funds.

Feature 5: Base layer and cross-chain accessibility

In a multichain world, the meaning of tokenomics has expanded to include measures that make a token accessible to users across different networks. The tokenomics design clarifies if the token is created, perhaps using the Ethereum network as its base layer and accessible to other blockchains via a bridge infrastructure.

For instance, Ethereum-based crypto tokens follow the ERC-20 standard, making them easily transferable on all Ethereum network infrastructures, such as wallets and decentralized applications. However, token creators may subsequently choose to make the token accessible on other networks like Polygon (MATIC), Solana (SOL), or BNB Chain (BNB) by creating a pegged version of the assets on these secondary networks.

Many projects factor this essential feature into the tokenomics design with an eye on boosting interoperability.

Green and red flags when considering tokenomics

Most crypto startups include information about their tokenomics in the project white paper. Studying the tokenomics data and other related information can help investors avoid investing in poorly-structured projects. This section covers the most common green and red flags while researching tokenomics for crypto projects.

Green Flags

Security audits

It is customary for projects with legitimate tokenomics to enlist a third-party security firm to audit its token code or core smart contracts (especially for DeFi projects). Such audits guarantee that the core project team does not reserve the right to issue new tokens outside the publicly disclosed amount or suddenly assume control of user tokens.

A classic example of why such audits are essential is the failure of the alleged community-theme crypto project Save The Kids. Several influencers promoted the tokens as being safe from whale manipulation. However, the core team changed the token’s code near its public release and rugged unsuspecting investors.

A security audit provides third-party assurance that minimizes the possibility of such an occurrence. It also ensures that functionalities such as vesting contracts and token distribution addresses match publicly available information.

Existing user base

A tokenomics designed to serve an existing user base would have greater longevity than one targeting new customers. For instance, a project with hundreds of thousands of existing users before releasing its tokenomics arguably has an existing business model that would last into the foreseeable future. In this model, existing users (also referred to as early adopters) can receive a sizable portion of the token allocation as a reward for supporting the project in its early years. Uniswap’s UNI token launch was a classic example. The founding team developed a working platform in November 2017, nearly three years before issuing a token.

Token disclosures

It is a green flag if the project team discloses the influencers and third parties it has hired to promote the project and the number of tokens given to each influencer. These disclosures also include the number of tokens sold to early-stage investors and their prices to subsequent investors. Unfortunately, such data is not always publicly available, making it difficult for investors to make more accurate decisions.

Red Flags

Skewed token allocation

A balanced token allocation is one where all stakeholders receive a fair portion of the token supply. This allocation should match the stakeholders’ contribution to the project’s continued growth.

Suppose a tokenomics distribution is skewed towards the core project team, with 40%-50% of the total allocation with a short vesting period. In that case, it could signal a red flag for potential investors, as it can enable price manipulation.

The same principle applies to a distribution heavily concentrated on early-stage investors, who usually buy in at a discount and can sell at massive profits even if the asset’s price drops.

Bogus use cases

Without a clear use case, tokens will struggle to find demand aside from pure speculation. Our next explainer on this tokenomics series will explain often predatory tactics associated with this lack of utility.

Investors should consider how stated use cases are core to the primary product offered by the crypto project. Wary investors might be concerned if the core product can exist without the token, or has no precise method of driving demand for the asset.

Opaque release schedule

If a project’s tokenomics does not disclose the release schedule for non-circulating tokens, it may be considered evidence that the project intends to dump tokens on unsuspecting investors. Such token release schedules must be publicly disclosed and updated frequently to ensure that all stakeholders keep track of key dates.

Tokenomics examples

Blockchain-based tokens introduced a new way for individuals and businesses to raise funding for their projects and build closely-knit online communities. The following tokenomics examples cover some of the most popular cryptocurrencies beyond Bitcoin.

Ethereum

Source: Quadency

Source: Quadency

Distribution

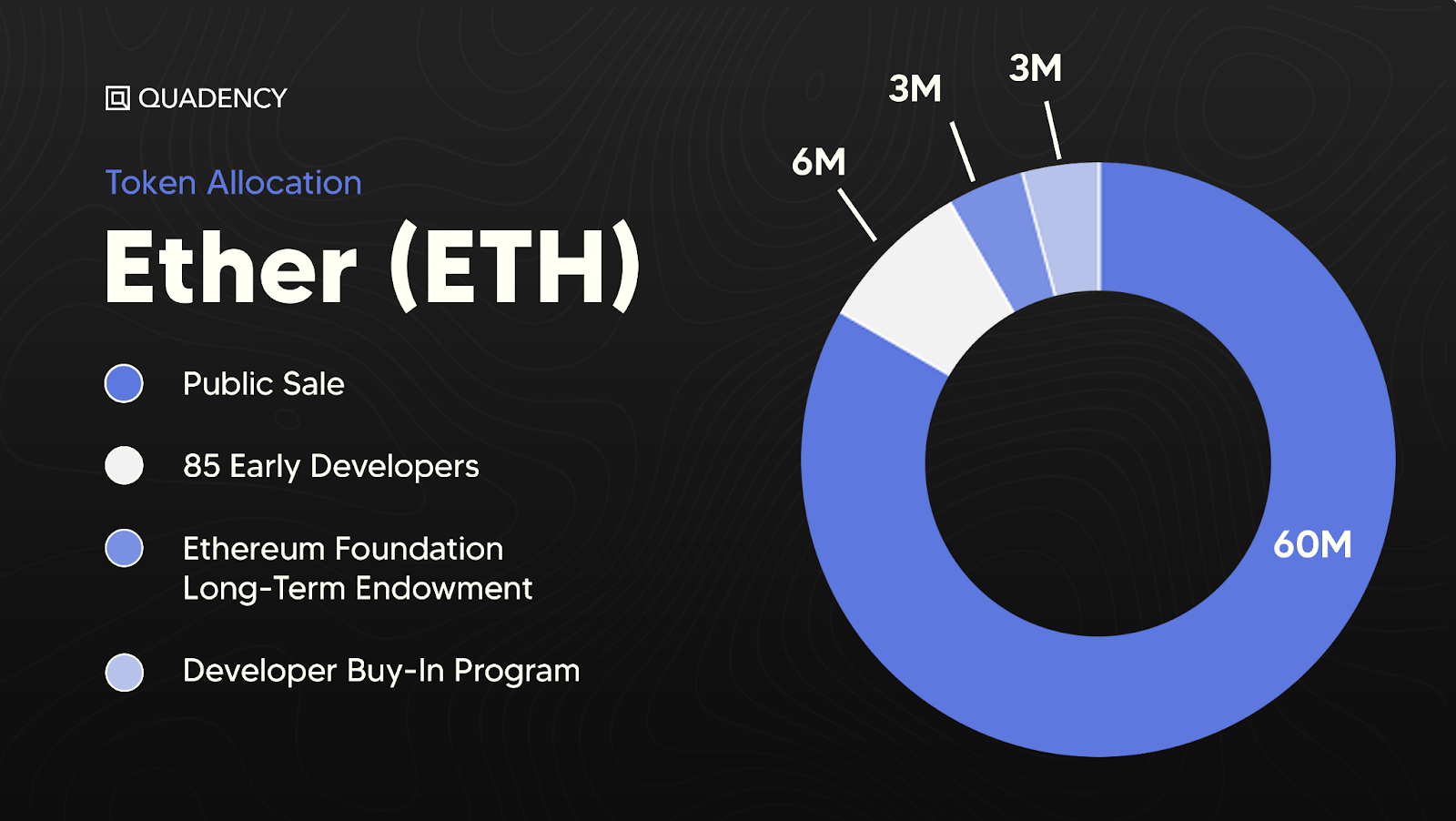

Ether (ETH), the second largest cryptocurrency by market capitalization, was pre-mined for early insiders and eventually sold to a global audience through an initial coin offering (ICO) in 2014.

Utility

ETH primarily serves as a means for users to pay transaction fees for moving assets on the Ethereum network.

Supply

Unlike Bitcoin, ETH does not have a maximum supply. Instead, the token’s supply is designed to perpetually increase at a controlled pace, with new tokens coming into circulation as the network expands. According to Blockworks research:

“The genesis token supply for the Ethereum network was 72 million ETH. 12 million of the genesis supply, or ~20%, were allocated to the Ethereum Foundation and early network contributors. The remaining ~80%, or 60 million ETH, were distributed via a public sale that took place between July 22, 2014, and September 2, 2014. The crowd sale led to 31,725 BTC being raised, however none of the ETH purchased was transferable before the launch of the Genesis Block on July 31, 2015. The funds were equal to $18.3 million at the time of the raise.”

Recently, Ethereum developers are moving towards achieving a deflationary ETH supply. The Ethereum ecosystem introduced a transaction fee-burning mechanism to control inflation. The long-term goal is an environment where the amount of ETH burned is greater than newly issued coins.

Read More: Ethereum tokenomics with Blockworks Research

Binance coin (BNB)

Source: Figment

Source: Figment

Distribution

Cryptocurrency exchange platform Binance launched its BNB tokens to raise funds for its business in 2017. 40% went to the founding team, 10% went to angel investors, and 50% was sold in a public auction.

Utility

The token enables users to enjoy low trading fees and access new token sales conducted on the Binance platform. BNB use cases have rapidly expanded with the Binance empire and are currently used to pay fees on the Binance-affiliated BNB Chain.

Supply

Binance commits a portion of its company’s profits to buy back and burn BNB tokens. Additionally, the Binance team burned its allocation of BNB tokens, which comprised 40% of its initial circulating supply.

Uniswap (UNI)

Source: Uniswap

Source: Uniswap

Distribution

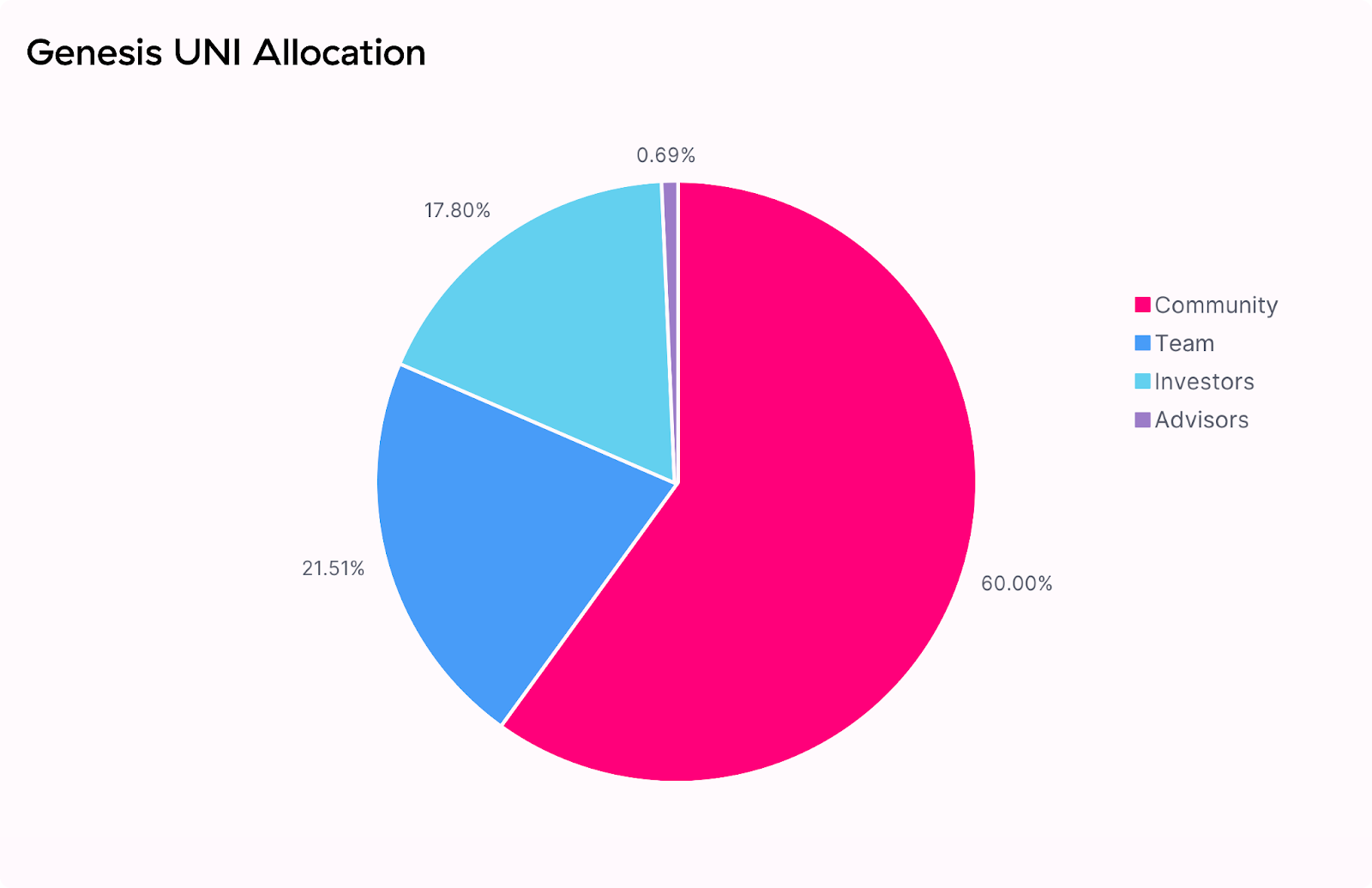

Ethereum-based decentralized exchange Uniswap released its UNI token in September 2020. Early adopters received a significant portion of the token through an airdrop, while another allocation was dedicated to liquidity mining programs to attract more users.

Utility

UNI primarily serves as a governance token, allowing stakeholders to shape the protocol’s development and earn rewards from trading fees. UNI holders participate in governance by proposing and voting on crucial protocol changes.

Supply

According to Blockworks research, “There is a total supply of 1 billion UNI that were minted at genesis and became accessible over the course of 4 years. After this, a perpetual inflation rate of 2% per year will begin to ensure continued participation and contribution to Uniswap at the expense of passive UNI holders.”

Read more: Uniswap tokenomics with Blockworks Research

The future of tokenomics

Tokenomics has evolved since Bitcoin’s creation. Cryptocurrency projects have tried several tokenomics models with varying degrees of success. New tokenization models such as non-fungible tokens (NFTs), soul-bound tokens (SBTs), and tokenized assets are also coming to the limelight and will shape the future of tokenomics.

However, the cryptocurrency industry is still in its early phase and is still light years away from deciphering the best ways to implement tokens into decentralized applications.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- Empire: Crypto news and analysis to start your day.

- Forward Guidance: The intersection of crypto, macro and policy.

- 0xResearch: Alpha directly in your inbox.

- Lightspeed: All things Solana.

- The Drop: Apps, games, memes and more.

- Supply Shock: Bitcoin, bitcoin, bitcoin.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- Empire: Crypto news and analysis to start your day.

- Forward Guidance: The intersection of crypto, macro and policy.

- 0xResearch: Alpha directly in your inbox.

- Lightspeed: All things Solana.

- The Drop: Apps, games, memes and more.

- Supply Shock: Bitcoin, bitcoin, bitcoin.