Fed Meeting Preview: Will Powell Go For Yield Curve Control?

As the world looks toward central banks’ responses to the pandemic-induced recession, the Federal Reserve’s two-day Open Market Committee (FOMC) meeting began yesterday. Fed Chair Jerome Powell is anticipated to remain dovish on economic policy, although he said in June that […]

Jerome Powell, Chair, Federal Reserve

- Chairman Powell said in June he was open to yield curve control

As the world looks toward central banks’ responses to the pandemic-induced recession, the Federal Reserve’s two-day Open Market Committee (FOMC) meeting began yesterday. Fed Chair Jerome Powell is anticipated to remain dovish on economic policy, although he said in June that he was open to considering yield curve control efforts.

Yield curve control is a central bank’s attempt to reach a target interest rate by buying or selling as many bonds as necessary. Proponents argue that keeping long-term interest rates in check is effective in stimulating the economy.

“In my opinion, Powell and the Fed will likely eventually be forced into explicit yield curve control,” said Luke Gromen, founder and president of Forest for the Trees LLC. “But in my opinion, they likely will not do so until they absolutely have to.”

The Fed has indicated that they plan to keep interest rates near zero percent for the foreseeable future. Last month, they committed to keep buying bonds until employment reaches a maximum and inflation stays at two percent.

Source: Crescat Capital, Tavi Costa

Source: Crescat Capital, Tavi Costa

“What we’ve done is, we’ve laid out a path whereby we’re going to keep monetary policy highly accommodative for a long time, really until—really until we reach very close to our goals,” Powell said in December. The Chair’s four-year term ends in February 2022.

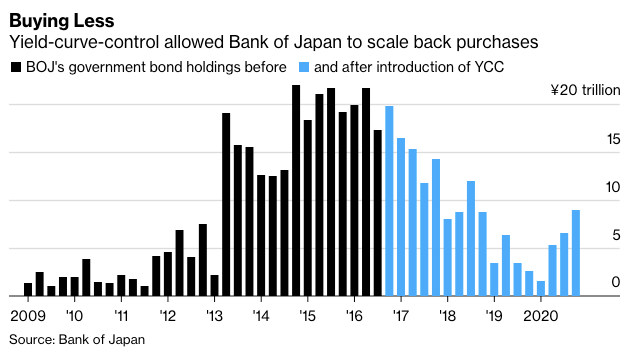

In contrast to the Fed’s approach, the Bank of Japan adapted a yield curve control policy in 2016. Counterintuitively, the implementation of yield curve control allowed the BOJ to purchase less bonds. [Below from Bloomberg, BOJ]

Source: Bloomberg, BoJ

Source: Bloomberg, BoJ

If Powell pulls the trigger for yield curve control, it could be utilizing the political cover of the BOJ, suggesting that Central Banks don’t have to print as much money to buy bonds after the implementation.