Bitcoin memecoins pushed fees higher than block rewards for first time

Miners may not have even noticed the halving took place over the weekend, with fees largely making up the difference so far

Shutterstock AI and Adobe modified by Blockworks

After memecoin mania cycles were speed-run on Solana and Base, this weekend was Bitcoin’s turn, and a new network milestone came along with it.

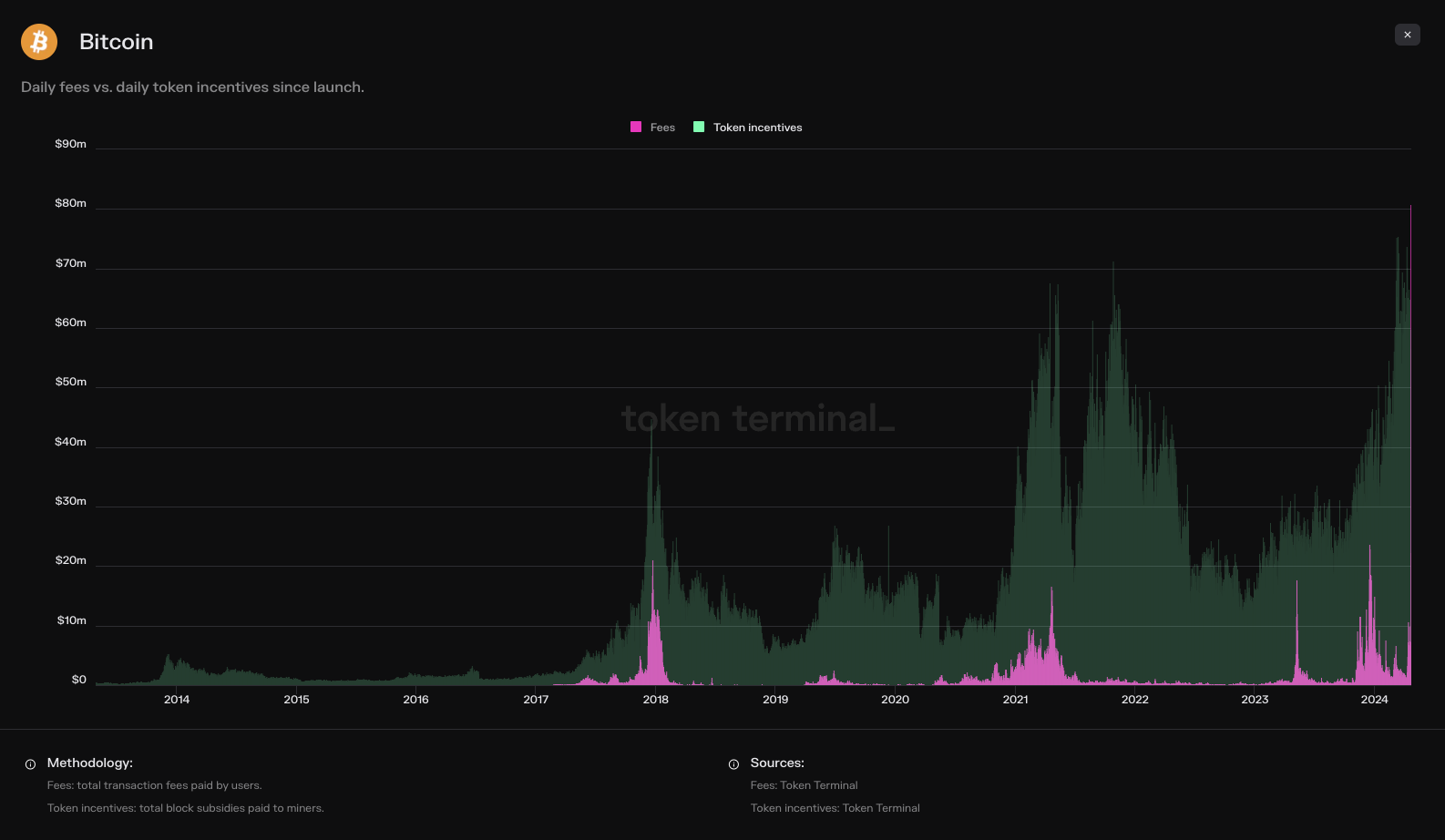

For the first time ever, bitcoin miners in a single 24-hour period earned more in fees than in block rewards. On Saturday — just after the halving and the launch of token minting protocol Runes — miners raked in $80.74 million in fees and $26.28 million in bitcoin.

That has never happened before, according to Token Terminal data. The day after also came close, with fees making up nearly 80% of all miner revenue.

Prior to this weekend, the closest fees that had come to flipping the block reward was during the peak bull market in December 2017: $21.1 million to $27.3 million. It also almost happened on Monday, May 8, 2023, with fees making up 42.6% of the total miner revenue for the day.

Runes, a new protocol for minting memecoins from Ordinals creator Casey Rodarmor, was released at the same block height as last Friday’s halving. Not for any technical reason — just it made for a neat countdown.

A slew of Rune mints immediately came online, and average transaction fees hit an all-time high of nearly $130, per BitInfoCharts, more than double the previous record from the last bull market.

About 53,000 Runes-related transactions were recorded in the first two hours, roughly one-third more than the overall network’s usual numbers across February and March.

Read more: Bitcoin Runes look to spice up the halving party

Runes made up more than half of all Bitcoin activity on Saturday and Sunday, which explains why fees went berserk. People were willing to splurge to use the chain, as long as it meant minting the first Runes to hit the network.

Now, Runes are down to about 30% of Bitcoin transactions and fees have fallen to about $11 for high priority.

The pink columns, representing daily fees paid, are practically off the chart (Source)

The pink columns, representing daily fees paid, are practically off the chart (Source)

Did Satoshi want memecoins on Bitcoin? Who cares

Runes are fungible memecoins that exist entirely on-chain. With Ordinals, special data (images, sounds, videos, text, browser-compilable code and so on) is written to individual satoshis (sats), imbuing them with non-BTC properties to make them unique and non-fungible.

Those sats become Ordinals, which can then be traded on NFT marketplaces alongside other unique digital collectibles on Ethereum, Solana and other blockchains.

Read more: Solana breaks $200 as memecoin and airdrop interest continue

Pseudonymous developer Domo riffed on Ordinals to create an experimental token standard for fungible assets, BRC-20.

Instead of images or videos, sats are inscribed with a JSON list of variables, including a ticker and max supply, technically making those Ordinals part of a larger, independent BRC-20 supply with its own market.

Domo had effectively hacked Ordinals to create lo-fi memecoins — while Bitcoin’s Taproot upgrade had been hacked to create lo-fi NFTs. A cypherpunk tradition.

By contrast, Rodarmor intends Runes to be more lightweight. Instructions for Runes are attached to UTXOs rather than individual sats, which means Runes (memecoins) can be ported to the Lightning Network or other similar projects in the future.

SatScreener, a portal tracking the implied market caps of Runes ($4.5 billion), has listed more than 7,000 different memecoins, most of them practically worthless, including:

- ALL-YOUR-TICKERS-SUCK

- WADDLE-WADDLE-PENGU

- BITCOIN-NETWORK-CONGESTION

- IDK-HOW-TO-SELL-THIS

Fees really can make up for the halving — this time

Bitcoin’s $130 transaction fees, even fleeting, are still absurd in crypto’s current age of low-cost prioritization before decentralization, trustlessness and even liveness.

Whether high Bitcoin fees are bad, however, depends largely on one’s vantage point. There are likely few complaints among miners, who as a cohort just took a 50% haircut on the block reward at the halving. On standard 10-minute block times, miners now earn 450 BTC ($29.7 million) per day, down from 900 BTC ($59.4 million).

A hypothetical trader who spent $50 to mint some Runes, which they then sold for much much more down the line largely wouldn’t care, either.

For someone using Bitcoin to protect their net worth from inflation, $100 fees would be infuriating. It’s practically impossible to know how many people fit into that scenario, but in any case, memecoins are surely pricing out those who need bitcoin most — particularly those with low balances.

Read more: Why is 2140 the end of bitcoin inflation?

And that may always be the reality of Bitcoin. It’s expensive to use. It might have to be to plug lost revenue resulting from the four-year halving schedule unless electricity for whatever reason suddenly becomes much less pricey.

That’s probably okay in a very broad sense; people who want to cheaply move value across borders can send and receive USDT on cheaper networks. And fees might have to rise even higher in future cycles, especially without abundant and low-cost energy.

Ignoring the plight of miners in favor of users, the general consensus is there’s not much anyone can do outside of pushing activity to the Lightning Network, or raising the block size limit, which is still a touchy subject.

Bitcoin layer-2s could hypothetically help, but it’s largely dependent on the trust profiles of those networks, as well as how users operate in the future. Besides, the current crop of Bitcoin layer-2s are all in preliminary development stages, so any potential benefits are far in the future.

Read more: How will the Bitcoin halving impact Bitcoin L2s?

High Bitcoin fees hurt even more with the knowledge that banal stuff like CASEYS-MOM-HAS-GOT-IT-GOING-ON is driving them higher.

But at this point, it just is what it is.

A shortened version of this article was included in today’s Empire newsletter.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.