Economic crosscurrents are straining the growth outlook

Ongoing tariff dynamics are being complemented by DOGE’s federal government employee layoffs

DOGE head Elon Musk | Alessia Pierdomenico/Shutterstock modified by Blockworks

This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

Often, macro is quite boring for a long time — and then it gets really exciting all at once.

The past couple weeks felt like one of those exciting moments as we’re clearly moving through a regime shift.

Let’s unpack everything that’s going on.

The fear of tariffs has led to a substantial frontrunning of imports, leading to a cratering trade deficit — the exact opposite of what Trump is trying to achieve.

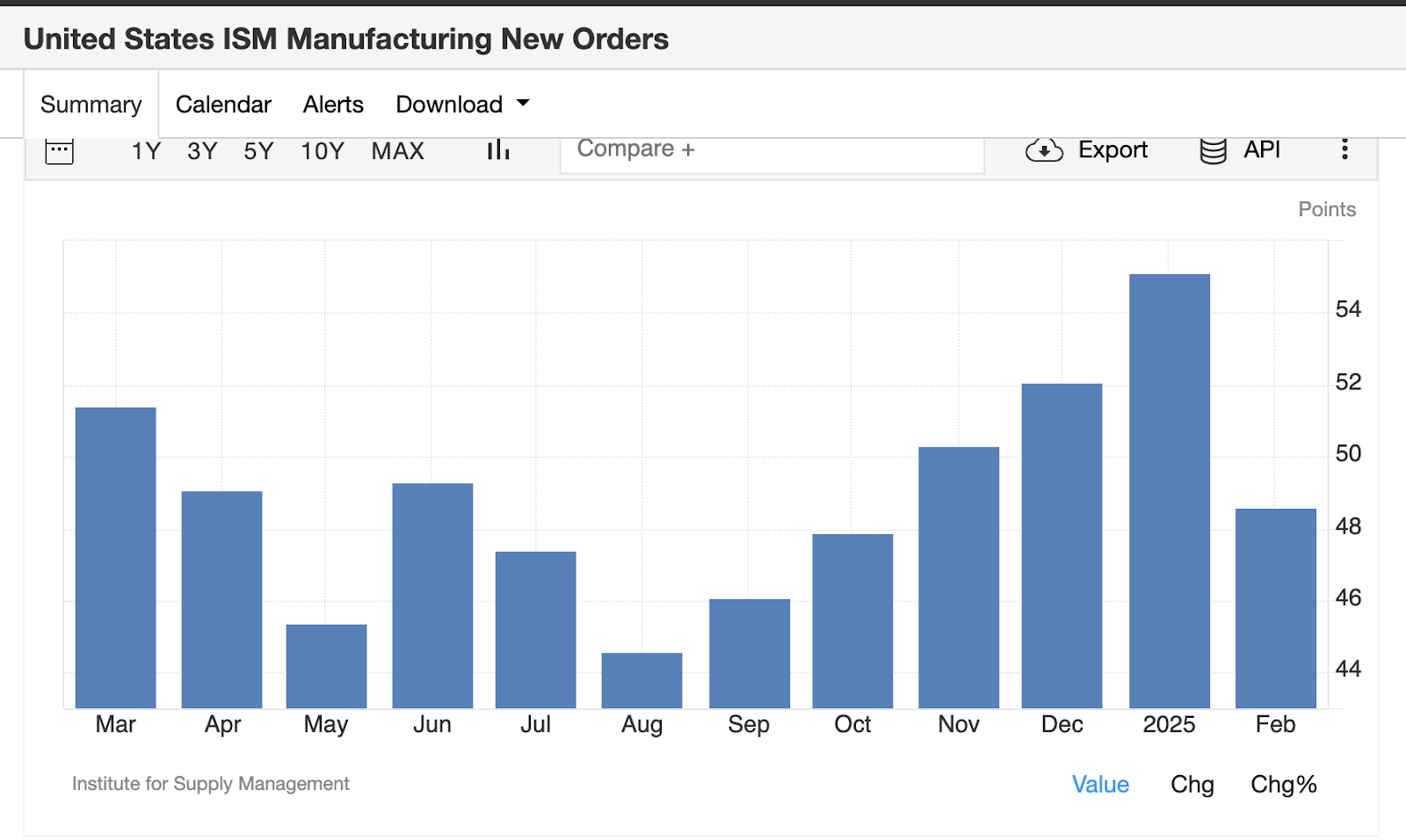

We’ve been able to track this tariff frontrunning through the ISM Manufacturing New Orders index.

As seen in the chart, there was a ratcheting up in order volume right up until the tariffs began to be implemented. With this week’s print, we’ve seen that order volume fall off a cliff:

As discussed previously, this upswing in manufacturing was either the beginning of a new business cycle or simply a headfake due to tariff frontrunning. It’s now clearly evident it was tariff related.

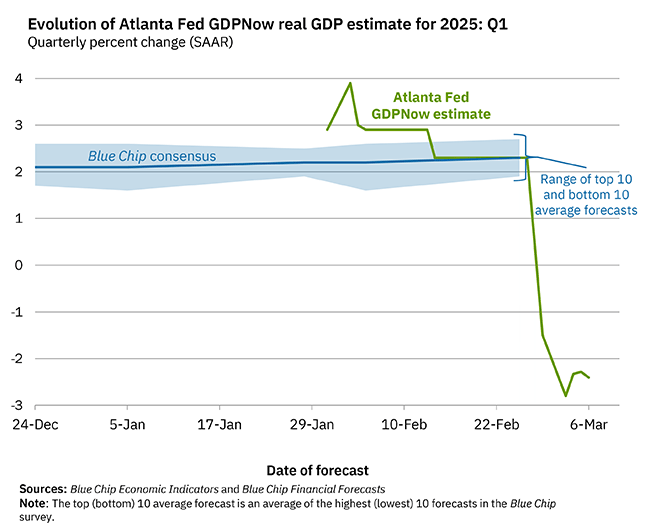

As we move into the impacts of tariffs and the uncertainty associated with their implementation, we’re seeing the Atlanta Fed GDPNow Nowcast project a contraction in the economy.

Although primarily driven by the huge amounts of imports (net exports is a function of imports-exports, so when imports surge, GDP declines), we also see the impact of the uncertainty and import glut trickle into the broader economy:

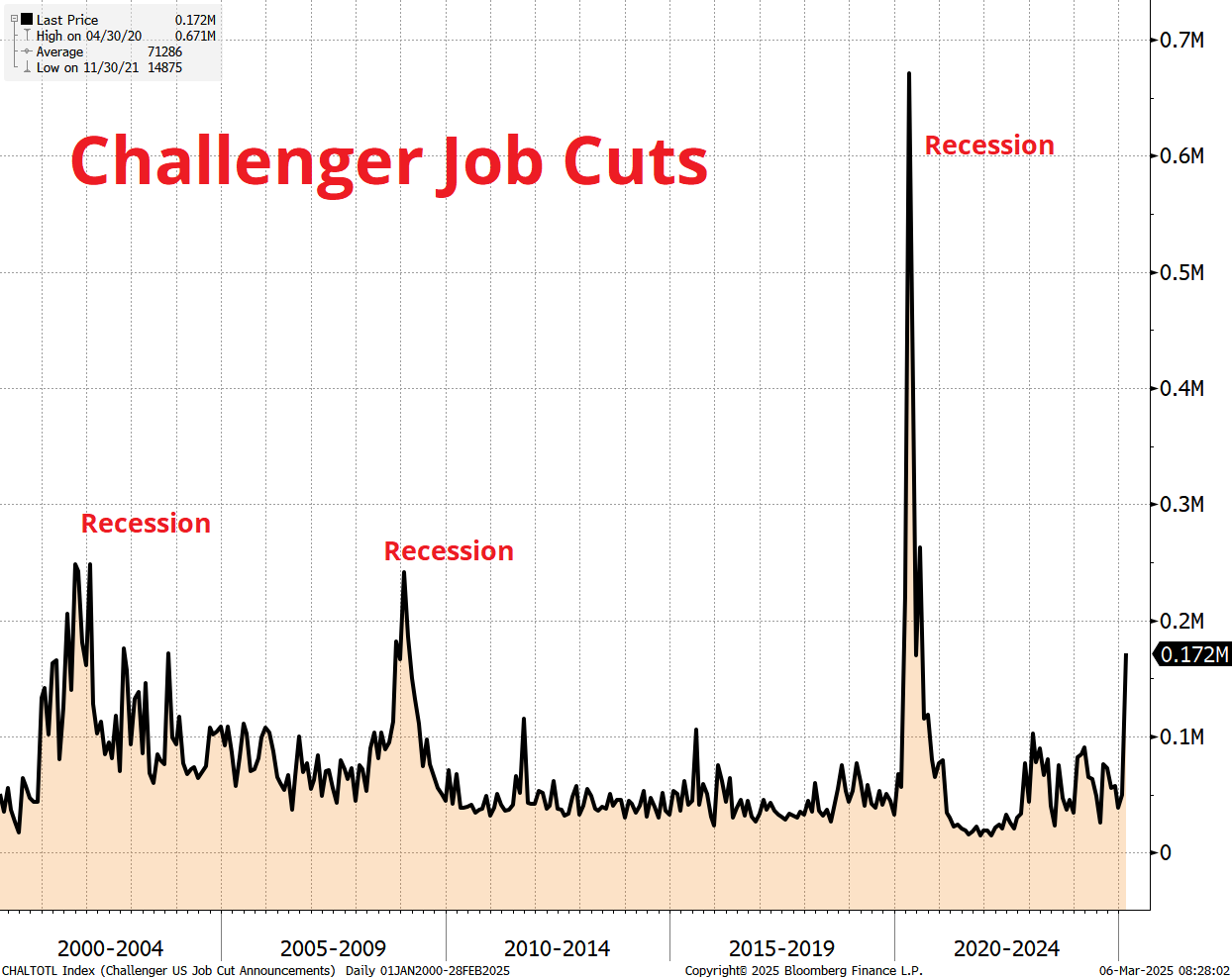

The tariff dynamic is being complemented by DOGE’s federal government employee layoffs. We received the Challenger survey job cuts print today and it was huge:

The dominating factor was, of course, the DOGE layoffs. However, the uncertainty associated with Trump policies is also affecting the private sector:

“The Government led all sectors in job cuts in February. (62.242K), followed by retail (38.956K) and tech (14.554K). So far this year, employers have announced 221,812 job cuts, the highest year-to-date total since 2009.”

With the jobs report out tomorrow, everyone will want to understand how vast this deterioration in the labor market will be. Unfortunately, since the survey window for this jobs report was Feb. 9-15, it will not provide as clean a picture as one would hope as the job cuts have only just begun to trickle into the data.

Regardless, it’s clear the trend is toward deterioration — it’s just a matter of how much.

Putting that all together, here’s where we stand:

- The fiscal retrenchment is real and the primary tailwind to the economy the last couple of years — fiscal dominance — is now reversing.

- Monetary policy remains in a state of pause and the Fed will not be proactive with any change in stance as it was in September. The Fed is in a reactionary tilt as it awaits clarity on the fiscal situation.

- DOGE is having a meaningful impact despite the debate on cutting costs. The layoffs are meaningful and those new job seekers are entering a labor market with an abysmal hiring rate.

The combination of these factors leads to an extremely fragile economic outlook with no signs of change. With all that said, it’s no wonder that risk assets have been having a hard time lately.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.