Is the Fed making a policy mistake?

There’s a lot of confusion as to why the Fed might still be cutting rates despite what looks to be an economy doing pretty well

Pla2na/Shutterstock modified by Blockworks

This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

There’s a lot of confusion about why the Fed might still be cutting rates right now despite what looks to be an economy that is doing pretty well.

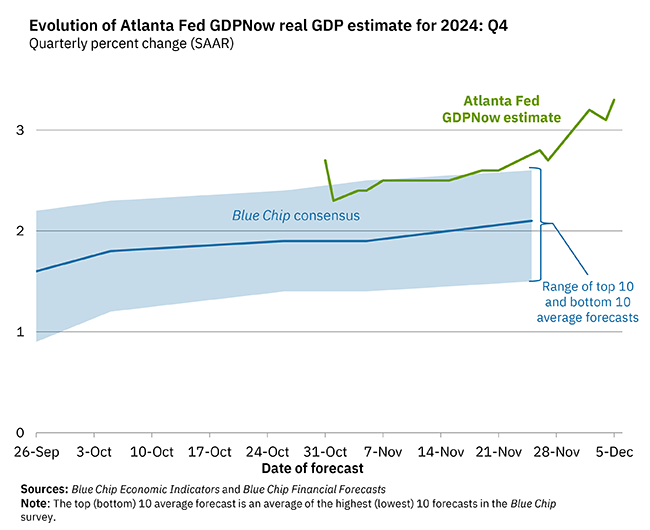

The Atlanta Fed GDPNow is currently forecasting a 3.3% real GDP growth rate for Q4, and it looks to be accelerating:

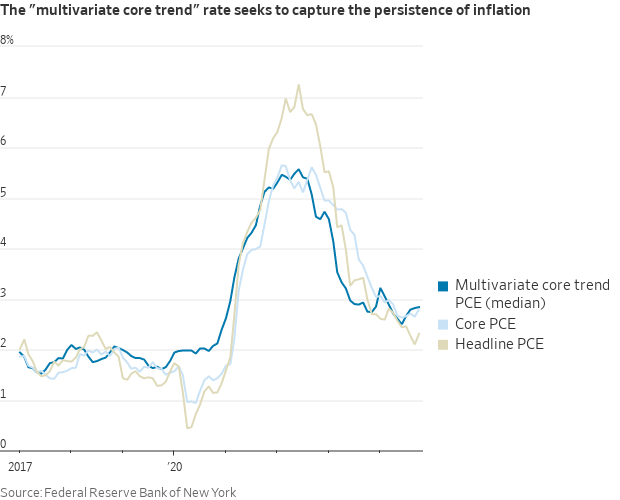

Further, it looks like inflation is beginning to rebound and has bottomed:

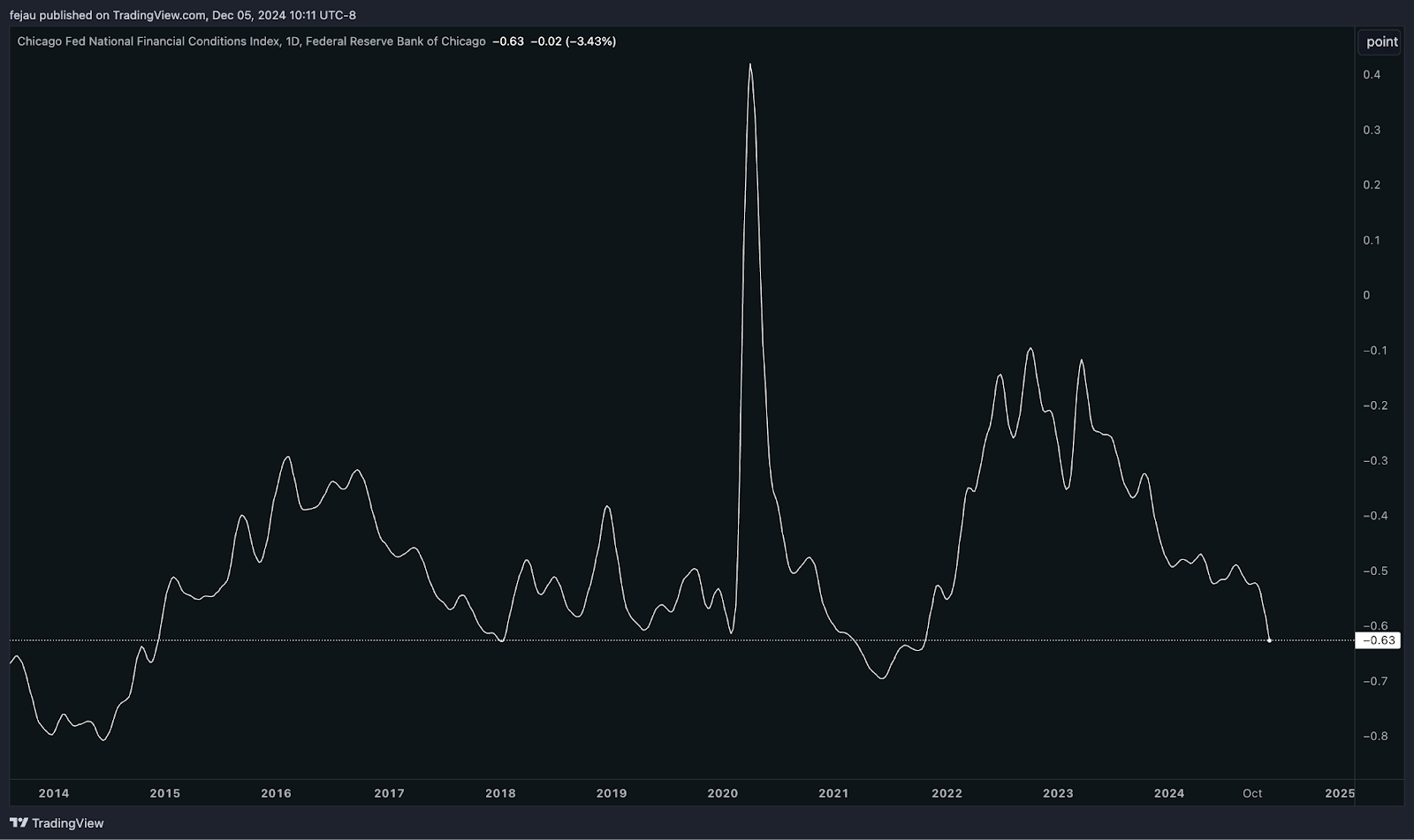

Also, financial conditions are nearly as loose as they were during the frothy 2021 era:

Despite all these metrics characterizing an economy that is doing very well, the FOMC is still sitting at a 70% odds of cutting rates this December. This has many people perplexed as to why they would still cut.

The simple reason is that the committee had already guided the market toward them cutting in December. They would hate to rock the boat, reverse that guidance and skip when the forward curve has already assumed they likely will.

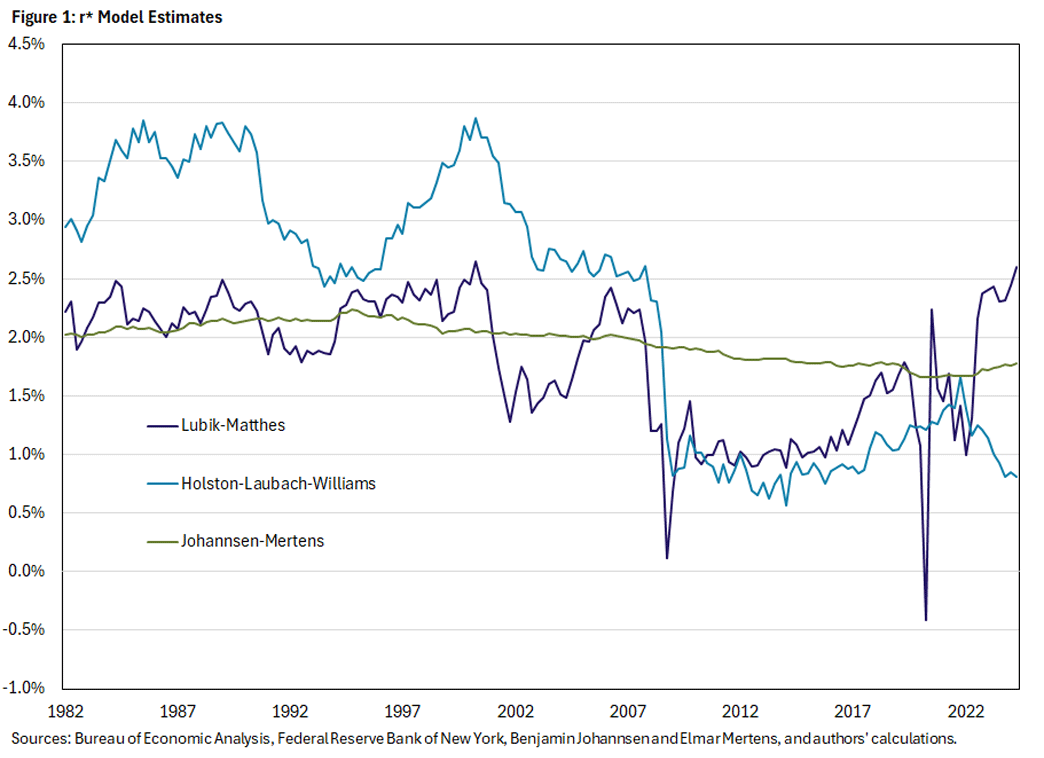

The more interesting answer resides in the rationale behind why they guided toward this cut in the first place. It has to do with r* — the neutral interest rate — and how the Fed measures it.

Because r* cannot be directly measured within the economy, policymakers instead rely on models that do their best attempt at estimating it. There are currently two models well-suited for this job: the Lubik model and the Williams model.

The Lubik model is more dynamic and based on a statistical model approach, whereas the Williams model is based on more traditional macroeconomic models that are less sensitive to major shifts in the drivers of r*.

Considering that the creator of the Williams model — John Williams — is the current NY Fed president, this model is weighted more heavily within the confines of the Fed compared to the Lubik model.

As we can see in the chart below, the Lubik model has picked up a significant uptick in r*, whereas the Wiliams model remains at a secular low.

Because of this adherence to the Williams model, the FOMC continues to strongly believe monetary policy is very restrictive, and that they could easily cut to 4% and remain restrictive.

However, if we use the Lubik model instead, there’s an argument to be made that monetary policy is already at neutral (at a bare minimum).

Empirically (as observed in the charts at the beginning of this piece), market signals are firing off all over the place that we are in a very accommodative environment from a policy perspective. Therefore, it’s reasonable to assume the Williams model is incorrect when compared to what we’re experiencing in markets and the economy right now.

There’s been a lot of talk from FOMC members lately around where they believe neutral might be. This suggests members might be rethinking their adherence to the Williams model. Some FOMC members, such as Austan Goolsbee, are even preferring to “feel their way” to neutral. See how the economy reacts, and go from there.

Considering how markets across the board continue to hit all-time highs on a daily basis, it’s hard to make the argument that we’re restrictive. Regardless, a cut in December still looks to be the base case as the FOMC remains anchored to bureaucratic inertia with respect to the Williams model.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.