Financial conditions tightened since the Fed cut rates. Why?

It’s crucial to look at the broad economy and not just the overnight rate that the Fed talks about

Dragon Claws/Shutterstock modified by Blockworks

This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

If I were to tell you that since the Fed’s rate cut of 50 basis points in September, financial conditions tightened (as opposed to loosened), would you believe me?

Well, that’s exactly what has happened. And for those not in the fixed income weeds, it might be a bit confusing how this could have occurred. So let’s break it down.

1. The rates complex

When the FOMC decides to lower interest rates, they’re actually just lowering one of what comprises many interest rates that make up the yield curve. Specifically, they are lowering the interbank overnight rate, otherwise known as the federal funds rate. As you move further out in duration on the yield curve, the less direct control the FOMC has on what that rate is, and the more it is controlled by market forces:

2. Priced for aggressive slowdown

The FOMC can attempt to influence the long-duration parts of the curve through guidance on the path of rates, however. Through this combination of guidance and a summer of soft economic data, the market then moved to price in one of the most aggressive cutting cycles in history:

We effectively were priced to see the fed funds rate reach 3% by the second half of 2025. From this aggressive pricing, the long end of the yield curve moved significantly lower to price in positioning that looked like a recession.

3. The 50bps cut as a trigger

From there, the Fed moved to cut 50bps, which was only priced at roughly 50% odds. This aggressive move helped quell concerns that the Fed was behind the curve and was risking a recession from happening if it moved too slowly and cut by “only” 25bps.

With the context of the near-recessionary pricing in the long end of the yield curve in mind — paired with an onslaught of positive economic data throughout September and October — something weird happened.

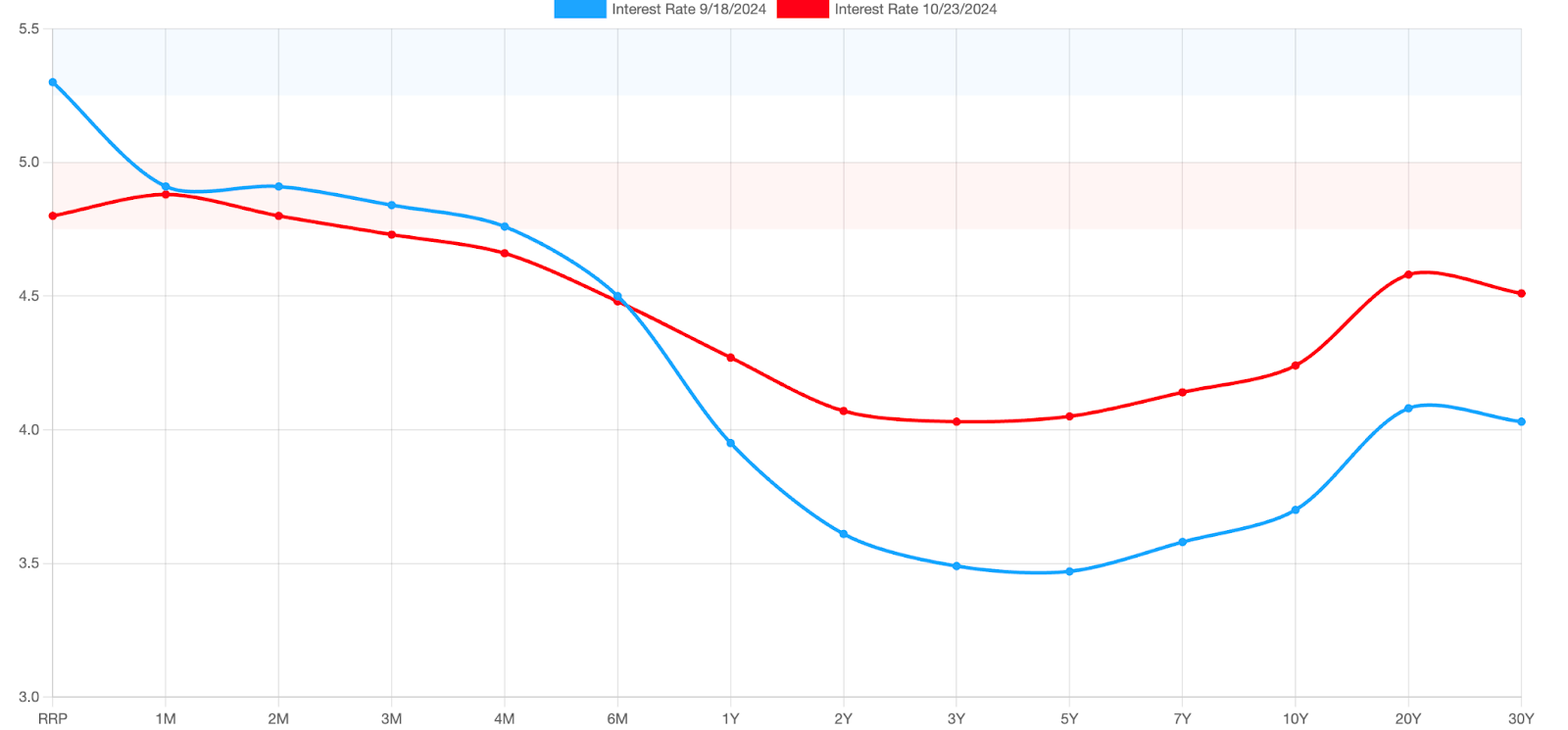

As the Fed cut the fed funds rate by 50bps, nearly every other maturity on the yield curve actually increased, as seen below:

So despite the 50bps cut to the fed funds rate, the vast majority of the yield curve is substantially higher than it was a month ago.

4. The economy operates on the long end

Most borrowing in the economy occurs at the long end of the yield curve as opposed to the short-term money market rates. Therefore, when the price of borrowing on the long end increases, financial conditions tighten, generally speaking. And so, with this recent surge in long bond yields since the 50bps cut, we have seen financial conditions actually tighten.

Term premia has increased, reflecting an increase in opportunity cost for borrowing on longer durations vs. short:

Also, 30-year mortgage rates have actually increased since the 50bps cut, despite the narrative that rate cuts would lead to lower mortgage rates:

This led to the mini mortgage refinancing wave we saw peaking during the week of the FOMC cut. It has decreased ever since, given the opportunity cost to refinance has gotten less alluring as mortgage rates have risen:

And so completes our journey of mechanically unpacking how, despite a cut in the federal funds rate, aggregate borrowing costs have actually increased of late. It’s crucial to look at the broad economy and not just the overnight rate that the Fed talks about.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.