Ken Wolter/Shutterstock and Adobe modified by Blockworks

This is a segment from the 0xResearch newsletter. To read full editions, subscribe.

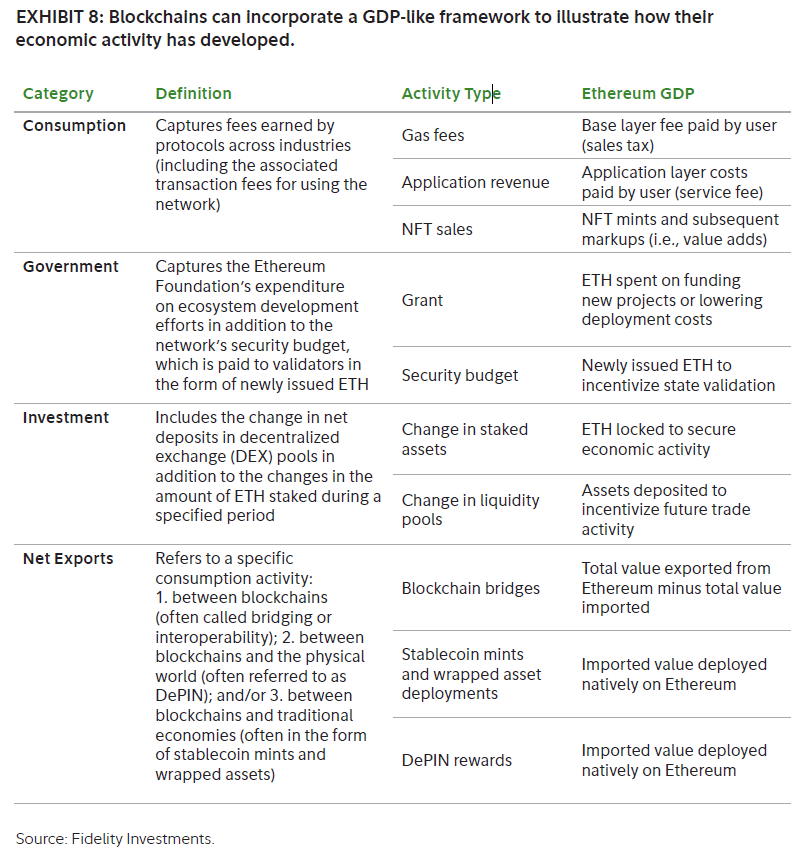

A recent report by Fidelity Investments proposes valuing blockchains on the basis of GDP:

“… it is more appropriate to compare decentralized blockchains to sovereign nations and their economies rather than web2 companies or products because of the embedded currency.”

Here’s the GDP formula: C + I + G + (X-M)

C is consumption, I is business investment, G is government spending, X is exports and M is imports, so X-M is net exports.

Fidelity uses ETH as an example. So, when you transpose the GDP formula onto Ethereum blockchain metrics:

- C = What users are spending as gas, to use Uniswap or mint an NFT.

- I = The quantity of staked assets or capital in liquidity pools.

- G = Ethereum Foundation expenditure, issued ETH to validators.

- X-M = How much stablecoins are minted/burned, bridge flows to/from other chains and DePIN rewards.

You can see the entire table here:

It’s a comprehensive effort by Fidelity, but it provokes some questions.

GDP is a measure of domestic production. Think “the value of everything made here.” When a country exports, that’s domestic production. When it imports, that’s spending. That’s why we “net” imports for GDP.

But if millions of stablecoins are bridged onto (import) or off of (export) Ethereum, that bloats a blockchain’s “GDP” even though nothing productive occurs onchain.

Contrast that to when a stablecoin is minted onchain, or when a Helium miner is paid in tokens for providing a useful mobile cellular service. These are productive “imports” that would rightfully count toward a blockchain’s “GDP.”

So measuring “net exports” by bridge flows is conceptually sound, but it needs to account for CEX cold-wallet sweeps, as Blockworks’ Dan Smith aptly pointed out.

Explicit in Fidelity’s valuation model is also the claim that L1 tokens should be valued on the basis of “money,” or more specifically: a medium of exchange and store of value.

Fidelity argues: “Ether is the dominant trading pair on exchanges and serves as a primary asset to borrow against.”

I think that at best justifies the “medium of exchange” aspect of money, but is silent on the “unit of account” aspect.

Early crypto investors have questioned the ability of L1 tokens to serve as a unit of account. As John Pfeffer wrote back in 2017:

“It is thus overly simplistic to assume that people will hoard that which they use to make payments as opposed to converting their store of value via the payment rail at the time of payment in the exact amount needed and for as little time as possible.”

Account abstraction (ERC-4337) even formalizes this reality, since it enables paying gas fees in any ERC-20 token. That vastly improves the user experience but it removes the need to hoard ETH, thereby undermining the “monetary premium” of the L1 token.

The final aspect of why I think the GDP analogy is somewhat strained looks to accounting for staked ETH under the “Investment” bucket of GDP.

Staking locks up existing assets, but no new productive capacity is created.

In economist jargon, it doesn’t push the “production possibilities frontier” in the same way investment does in the real economy.

So the “I” in blockchain GDP loses its predictive link to future growth.

Even worse: LP deposits can migrate and earn purely extractive airdrops or MEV.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.