Celsius Faces Heat for at Least $1.2B Balance Sheet Hole, Customers Owed $4.7B

The cryptocurrency lender is left with a $40 million claim against Three Arrows Capital, CEO Alex Mashinsky said in a declaration

Source: Shutterstock

key takeaways

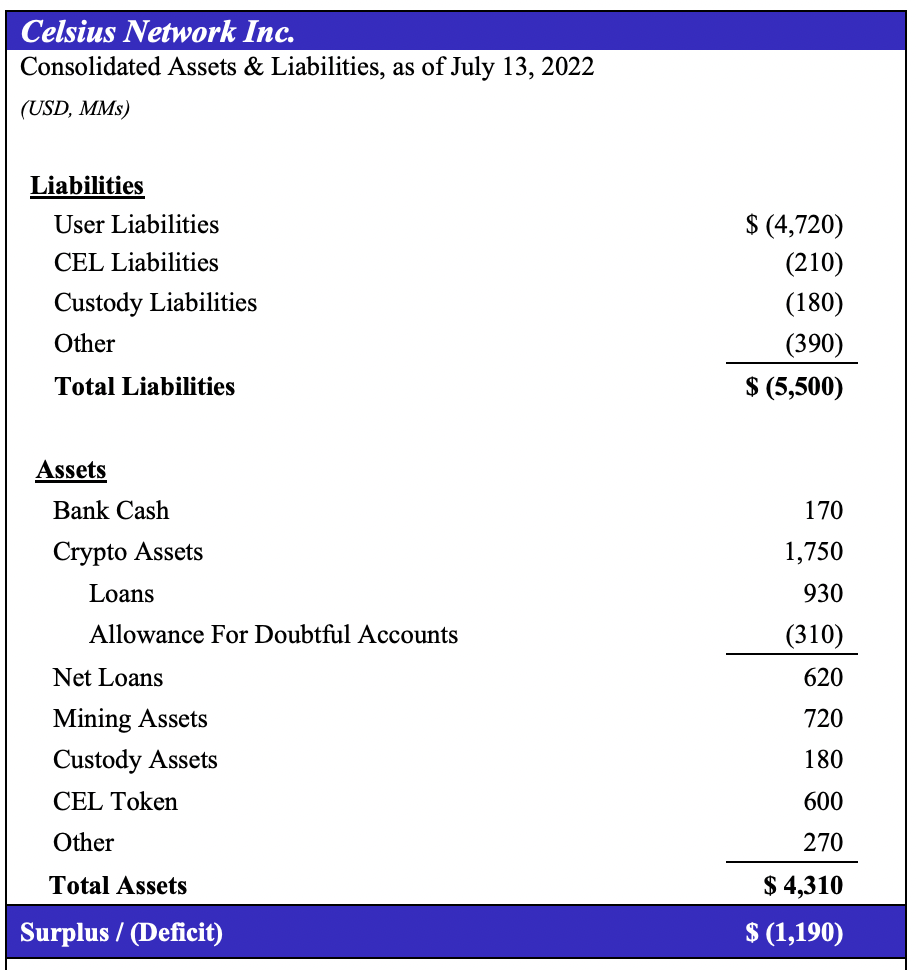

- Celsius has $5.5 billion in liabilities and $4.3 billion in assets, a filing from Thursday shows

- It has 23,000 loans to retail borrowers in the amount of $411 million

A new filing from Celsius lays out why it is unable to meet obligations, showing the cryptocurrency lender’s liabilities exceed its assets.

As of July 13, the company had $5.5 billion in total liabilities and $4.3 billion in assets, according to a declaration made by CEO Alex Mashinsky in the Thursday filing. That leaves it with at least a $1.2 billion shortfall.

But it could be much higher; hundreds of millions of dollars of the assets side of Celsius’ balance sheet are comprised of its own volatile CEL cryptoasset, which the firm values above its present market cap by some $400 million.

The lender owes over $4.7 billion to its users alone, meaning it is unable to repay them unless it finds liquidity from third parties.

The filing, made in the Bankruptcy Court for the Southern District of New York on Thursday, shows Celsius had extended two loans of $75 million to embattled crypto hedge fund Three Arrows Capital (3AC). When 3AC failed to repay the loan, Celsius liquidated 3AC’s pledged collateral, and is now left with a $40.6 million claim against the fund, Mashinsky said.

It owes $81 million to a little-known Cayman Islands-based crypto trading firm, Pharos USD Fund. The filing lists an email [email protected] for the fund, signaling it could be a subsidiary or venture associated with London-based crypto trader Lantern Ventures. Blockworks didn’t receive a response from the email address by press time regarding its loan. Celsius separately owes Alameda Research $12.8 million.

Some of Celsius’ cryptoassets are tied up in illiquid investments such as its bitcoin mining business and a custody technology firm, the filing said, adding that it’s unable to meet user withdrawals and provide additional collateral because of these illiquid assets and the plunge in crypto prices.

Source: Filing made by Celsius’ counsel Kirkland & Ellis

Source: Filing made by Celsius’ counsel Kirkland & EllisCryptocurrency lending has exploded in popularity in recent years, gaining traction for promising high yields on customer deposits and easy access to loans. The aim here is to pocket profits from loaning user deposits to institutional investors.

But post the recent TerraUSD (UST) crash and macroeconomic uncertainty weighing on investor sentiment, many lenders froze customer funds after seeing a heavy uptick in withdrawals. Celsius’ own withdrawal halt on June 12 sparked fears among users about whether they would be able to receive funds that were locked in the platform.

Its terms of use particularly intensify these concerns.

In the Thursday filing, Mashinsky said the user agreement between Celsius and its customer explicitly states that users are required to transfer “all right and title” of their cryptoassets to the lender, including the right to sell, lend and transfer them over any period of time.

The lender had 23,000 outstanding loans to retail borrowers in the amount of $411 million with a market value of $765.5 million in digital assets, the filing added. It is now in talks with third parties about raising potential sources of new liquidity.

Celsius filed for bankruptcy in New York this week, about a month after it first stopped withdrawals on its platform.

Mashinsky also said the firm attempted to overcome the market downturn — which he referred to as the “cryptopocalyse” — and blamed “false information” on social media about its association with TerraUSD’s collapse for causing the CEL token’s decline.

Celsius’ CEL is down 83% so far this year — but up 5.4% in the last month — and traded at $0.73 as of 1:00 am ET on Friday, data from Blockworks Research shows. The company claims it now has about $600 million in CEL, with a market cap of about $170.3 million as of July 12.

A day before Celsius initiated bankruptcy proceedings, financial regulators in Vermont said the company is “deeply insolvent” and would be unable to meet creditor obligations.

But Celsius’ insolvency just might be good news for the industry, as “it’s an important step in allowing the market to move on from the collapse of the borrow-lend market,” said Jay Fraser, head of strategy at BSTX.

This story was updated on July 15, 2022 at 4:55 am ET

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- Empire: Crypto news and analysis to start your day.

- Forward Guidance: The intersection of crypto, macro and policy.

- 0xResearch: Alpha directly in your inbox.

- Lightspeed: All things Solana.

- The Drop: Apps, games, memes and more.

- Supply Shock: Bitcoin, bitcoin, bitcoin.