THORChain halts withdrawals amid $200M insolvency

Can THORChain weather the RUNE liquidity crisis?

Shizume and Adobe stock modified by Blockworks

Founded in 2018, THORChain is an OG DeFi L1 chain that rose to fame with its innovative cross-chain swaps (THORSwap). Since then, the chain has expanded to offer lending and savings interest accounts.

As of earlier today, THORChain withdrawals from its Lending and Savers products have been officially halted. THORSwap and the underlying chain are fine.

The halted withdrawals come off the back of the painful decision by THORChain co-founder JP Thor two weeks ago to pause deposits into the Savers and Lending program for a six-to-twelve month period — a decision which was overturned by Thorchain validators.

The chain is sitting on about $200 million of BTC and ETH-denominated liabilities that it cannot afford to pay out, at least not without further crashing the price of its native token, RUNE.

Wait, why does RUNE enter the picture?

THORChain lending works differently to other DeFi money markets like Aave. On THORChain, lent collateral is instantly sold for its native RUNE token, which is then burned after swapping to a borrower’s desired debt asset.

When borrowers repay their loan, new RUNE is minted again to repurchase the borrower’s pledged collateral from the market and repay it to borrowers.

This effectively places RUNE token holders as the counterparty for each loan.

This somewhat roundabout mechanism is nice if you’re bullish RUNE. The mechanism design places RUNE at the center of the value accrual flywheel and increases its demand.

The key risk here, however, is that this depends on RUNE outperforming assets like BTC and ETH that it is borrowed against. Simply put, THORChain’s protocol design is long RUNE against BTC and ETH.

When RUNE depreciates relative to BTC and ETH, more RUNE needs to be minted at the closure of the loan than the amount of RUNE that was burned initially.

This leads us to the unwanted outcome that is happening today: inflationary (and selling) pressure on RUNE rather than the intended effect of deflationary (and buying) pressure.

RUNE’s tokenomics is also intertwined with its yield-bearing Savers product.

THORChain’s Savers uses a kind of wrapped synthetic asset (called synths) to allow single-sided asset exposure. Roughly, it works like this:

- A user deposits one BTC.

- THORChain sells half the BTC for RUNE, and adds the BTC-RUNE pair to a liquidity pool.

- The user receives synthetic BTC, which can be staked for yield (accruing from swap fees and liquidity rewards) without the risk of impermanent loss.

- When the user chooses to withdraw, THORChain sells the previously bought RUNE to form one BTC, which is then returned to the user.

Note the similar “long RUNE, short BTC and ETH” dynamic at play here. This design protects against impermanent losses for LPs, but it also means LPs are taking a leveraged long on RUNE.

Thus, RUNE’s underperformance creates the same kind of downward spiral consequences for Savers, just as it did for its lending product.

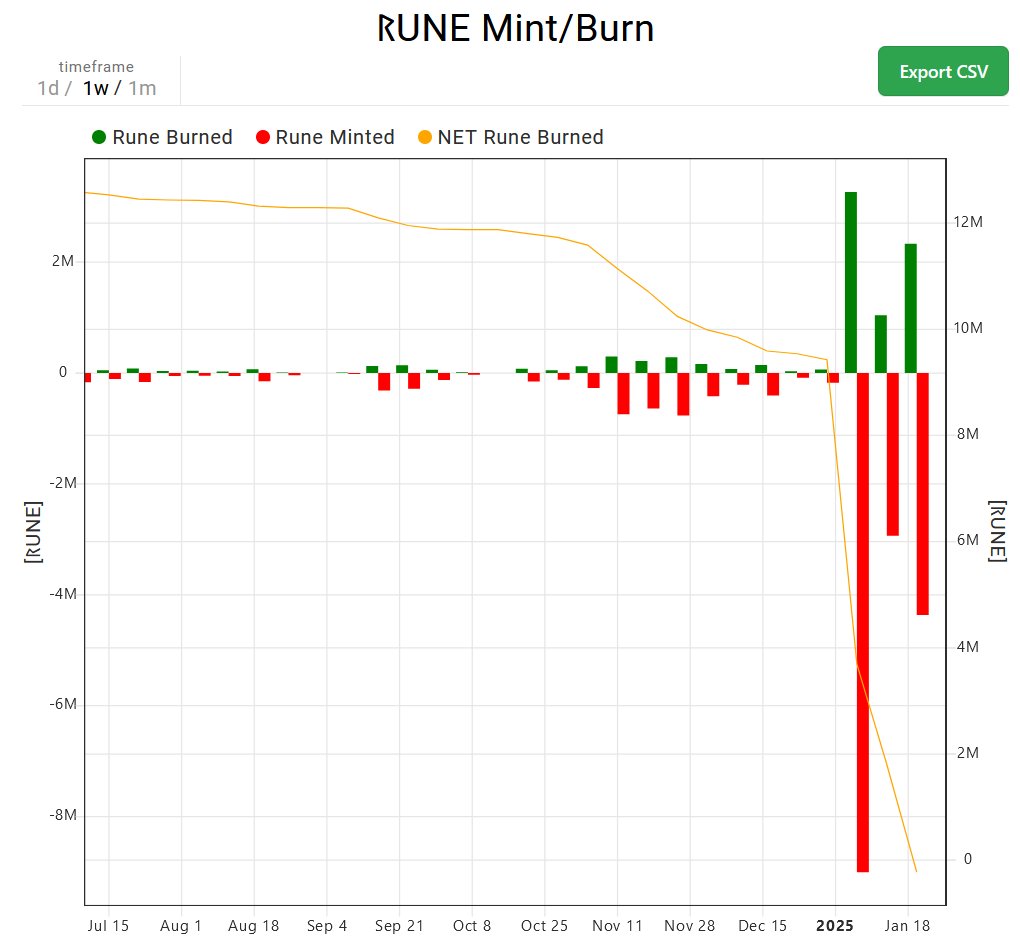

The chart below shows the rate of RUNE mints far exceeding the rate of RUNE burn:

Source: Thorcharts

Source: Thorcharts

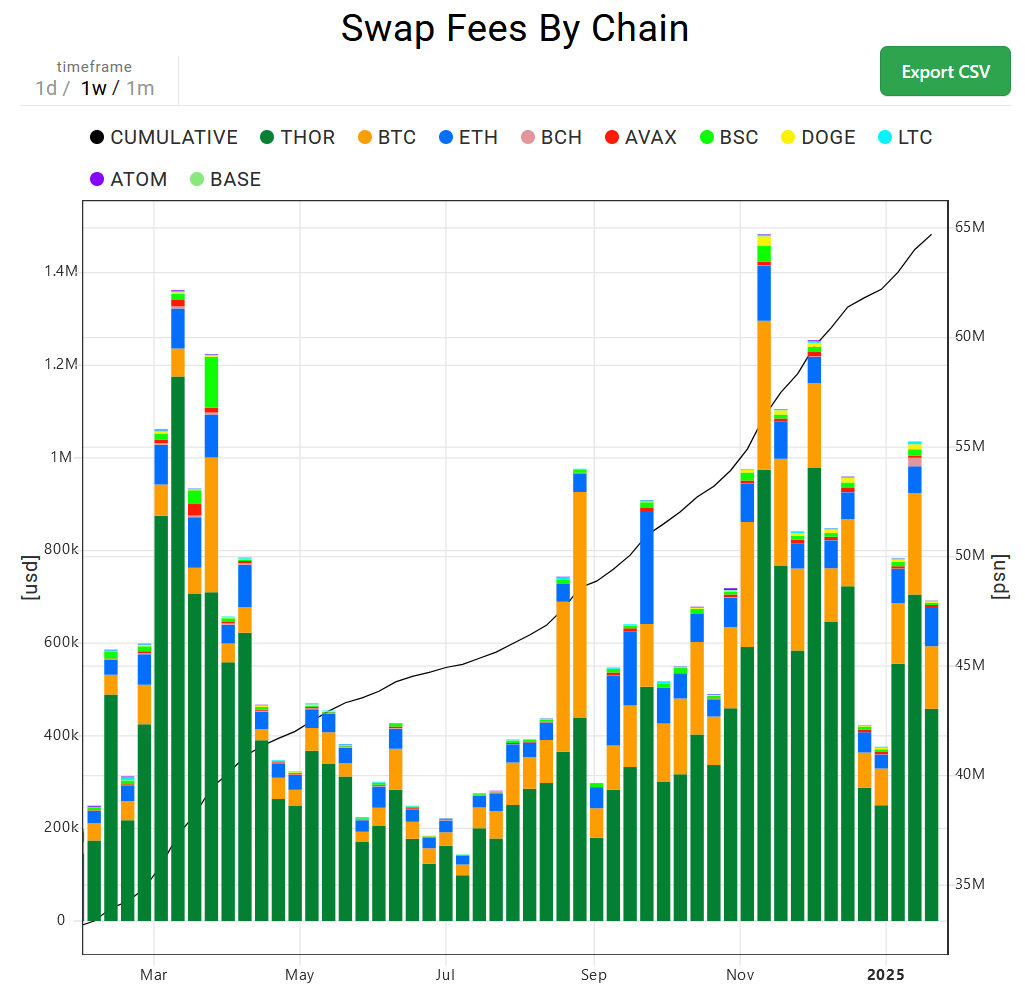

It’s worth reiterating that THORSwap, the original use case of THORChain, is fine. It’s still swapping about $50-60 billion in weekly trading volumes, and generated about $700k in fees over the past week.

Source: Thorcharts

Source: Thorcharts

The RUNE token, however, is down 44% on the week, which is not fine. It’s the asset that needs to be sold to repay borrowers wanting to close their loans, or savers wanting to withdraw, but doing so would accelerate the crash of RUNE’s price, which in turn leads to deeper insolvency.

Osmosis co-founder Sunny Aggarwal said of the THORChain debacle: “The situation unfolding with THORChain is eerily similar to what happened with Terra/Luna implosion in 2022, where the protocol’s solvency was too heavily dependent on the price performance of the native token.”

Next steps? THORChain’s co-founder suggests using protocol revenue and incentives from its sister company Rujira (previously Kujira) to make lenders whole over a 2-3 month timeframe while everything is on pause mode.

“It’s uncertain whether lenders can be fully compensated. Some have suggested that the shortfall could be covered by protocol fees collected over time. But this overlooks an important point: the bulk of THORChain’s liquidity comes from its lending and savers platform, ThorFi. So it doesn’t make sense to consider THORChain and ThorFi as separate entities,” Aggarwal told Blockworks.

For a deeper dive on the mechanics leading to THORChain’s insolvency, see Blockworks Research’s report by analyst Luke Leasure from last week.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.