The Flippening: Will Ether Flip Bitcoin in the Next Year?

Bitcoin has forever remained the top crypto, but Ethereum’s Merge could mark the beginning of a major divergence

Source: DALL·E

key takeaways

- The potential for bitcoin to flip ether has rarely looked stronger, though some analysts argue that isn’t enough

- Ethereum’s Merge is expected to spur additional outside investment due to a 99% decline in energy consumption

For years, Ethereum proponents have pined for the — hypothetical, as of now — moment when ether eclipses bitcoin’s market capitalization: “The Flippening.”

What better time than Ethereum’s Merge? It’s one of the most significant updates in the history of cryptocurrency yet, converting its energy-intensive, proof-of-work-backed consensus with its own brand of proof-of-stake.

The fusion of Ethereum’s Beacon Chain and its long-running mainnet is expected to trigger in six days time.

But whether it’s enough for ether to usurp bitcoin is another story. Bullish sentiment would propose June as the bottom for both equities and cryptoassets — both have tanked about 70% from their respective November peaks.

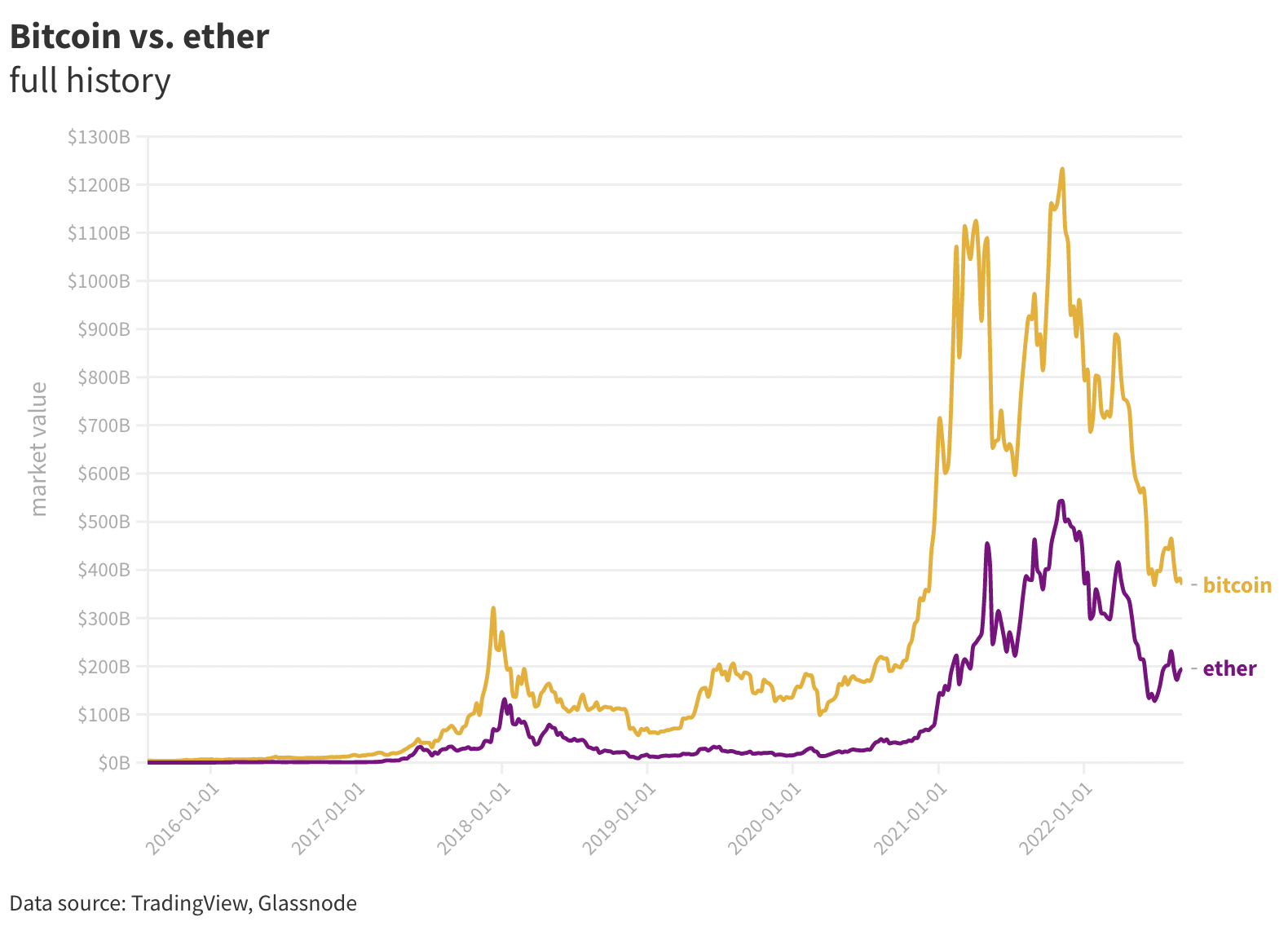

Bitcoin is hovering around $19,000 and its market capitalization stands at just under $368 billion, representing 39% of the total digital asset market.

Ether trades for $1,600, and its nominal value is a touch over half bitcoin’s, at $196.4 billion, a little over one-fifth of crypto’s collective capitalization.

Back-of-the-napkin math shows The Flippening would occur if ether reaches roughly $3,050 — true only in the relatively unlikely event that bitcoin’s price holds steady.

“The ‘flippening’ is only really a symbolic victory for ETH maximalists, but perhaps not overly significant for the industry as a whole,” Bobby Ong, co-founder of data provider CoinGecko, told Blockworks.

It’s unlikely for ether to rise past bitcoin in the next 12 months, Ong said, as both bitcoin (BTC) and ether (ETH) have been moving in similar directions due to the macro environment, dogged by inflation.

Software iteration breeds bulls

Ether is eyeing another run at yearly highs against the price of bitcoin, indicating markets are assigning value to the Merge.

But ether was much closer to flipping bitcoin more than five years ago, the early innings of the last bull-bear cycle. On June 12, 2017, the market capitalization of ETH was almost 84% that of BTC, with just $7.16 billion separating the two, according to TradingView data.

That figure is currently around 52% (with more than 100% indicating a flippening). In January 2020 — at the bottom of the last bear market — the situation was far worse, with ETH at just 11% of BTC’s value ($15.4 billion to $146.7 billion).

Still, market values don’t tell the full story.

Comparing on-chain metrics including transaction count, protocol fees and the number of active addresses across networks can also provide insight into their growth.

Ethereum is ahead in terms of transaction count and protocol fees, CoinGecko’s Ong said, and in major dapp development. It’s also steadily catching up to Bitcoin in terms of daily active addresses.

But the number of total bitcoin users — active or not — vastly outpaced ether’s at the height of the previous bull run.

Bitcoin users grew 37.5% between July and December 2021, from 128 million to 176 million, according to a Crypto.com report published earlier this year. On the other hand, only 23 million users held ether, a statistic which only grew by 1.4% over the same period.

Ethereum’s switch to proof-of-stake could help boost those numbers. Not only is the Merge expected to cut Ethereum’s energy consumption by more than 99% — replacing its GPU miner-based issuance model to one based on crypto-collateralized validator nodes (read: servers) — it also lays the foundations to scale the network’s base layer more effectively, proponents say.

This might help spur further ecosystem development and present an attractive investment opportunity to eco-conscious investors, even institutional ones, so goes the bull case.

“We expect not only renewed interest from building projects on the platform but also from an investment perspective,” Lachlan Feeney, founder of Australia’s largest blockchain consultancy Labrys, told Blockworks.

Yet, big money institutions are still concentrating their exposures, for the most part, to bitcoin.

“This advantage cannot be understated as the influence of institutions grows within the market,” said CoinGecko’s Ong. “Whether ETH, or any other crypto, can challenge its market share in this space remains to be seen.”

Cult of personality

Bitcoin and Ethereum differ significantly in primary use cases, diverging their value propositions. Bitcoin’s application scope is narrow: It’s censorship-resistant money, propelled by peer-to-peer payments.

But Bitcoin’s architecture — by design — does not support smart contracts, unlike Ethereum and a raft of layer-1 competitors. This essentially restricts bitcoin’s usage to micropayments and tips. (Remember the Lightning Network-powered Pollofeed?)

Indeed, even with Lightning, Bitcoin is less applicable to the broader Web3 crypto ecosystem.

This magnetizes Bitcoin to its “store of value” sales pitch — users should rather hold their bitcoin than spend it in the same way as ether and other Ethereum-bound assets.

Some argue the Bitcoin development community prides itself on an unwillingness to iterate as quickly as Ethereum, bucking the “move fast, break things” tradition of Silicon Valley lore.

The early abdication of Satoshi Nakamoto, Bitcoin’s pseudonymous founder, contrasts Ethereum co-founder Vitalik Buterin’s persistent gravitas within Ethereum crowds — another potential boon to its value prop.

“Vitalik actually stepped away from doing a lot of work on Ethereum at the end of the ICO craze, but he still sets the roadmap and he still gets a lot of input,” Katie Talati, director of research at Arca, told Blockworks.

Added Talati: “And obviously, his opinion means a lot. He’s not necessarily dictating the day-to-day, but I think it does help having a bit of a guide.”

Another effect of Ethereum’s proof-of-stake plan is that it will eventually turn the token into a deflationary asset, which industry participants say would likely generate significant interest.

Bitcoin’s supply limit is famously hardcoded to 21 million, while ether’s floats. The protocol modifies ETH’s issuance rate and supply constantly, with the network currently burning transaction fees rather than paying them to validators.

Sometimes, more ether is burned inside a block than issued, temporarily switching the cryptocurrency from inflationary to deflationary — a phenomenon expected to occur more frequently post-Merge.

Tell-tale signs of The Flippening unclear

Bitcoin’s issuance slowly decreases, halving every four years — but its supply will never formally decrease. This, at best, imbues anti-inflationary properties, although they are amplified once block rewards reduce to zero next century.

Vivek Raman, head of proof-of-stake at BitOoda, believes Bitcoin’s faults give Ethereum an edge in creating sustainable monetary policy, complete with high network revenue to inspire longevity.

“It’s almost like a mathematical inevitability,” Raman said about the possibility of Ethereum flippening, estimating it could happen possibly a year after the upgrade. He argued bitcoin enjoys its status due to an early-mover advantage, backed by the idea of a “pristine” digital asset — immaculately concepted by Nakamoto.

According to Raman, Bitcoin’s proof-of-work may ultimately work against its value prop, especially considering mining rewards halve every four years.

While tapering issuance hasn’t threatened its security model so far, with enough miners on the network despite lower rewards, they’re still paid less over time. “This means there’s less and less incentive to mine every four years,” Raman said.

So, what are the tell-tale signs of an impending Flippening? Surging open interest on ether futures has been floated as one indicator: There’s currently $12.8 billion in BTC open interest compared to $8.6 billion for ETH, per CoinGlass.

But Raman suggested open interest is mostly a short-term signal. And in any case, rising levels of open interest on ether futures could simply reflect appetite for Ethereum’s decentralized finance (DeFi) protocols.

“Ethereum has decentralized finance sitting on top of it. So, it has an economy running on it — because of that, there’s more leverage,” Raman said. “If there’s more leverage in the system, you’re gonna see a lot more open interest from futures and options. But that’s just a function of more speculators, more participants.”

With no clear indicators and a suffocating macro backdrop, predicting the Flippening is a tricky undertaking.

It doesn’t seem likely to occur around the Merge — or even within the next year — but it’s clear the two networks, and their native digital assets, are poised to diverge in a big way.

David Canellis contributed reporting.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- Empire: Crypto news and analysis to start your day.

- Forward Guidance: The intersection of crypto, macro and policy.

- 0xResearch: Alpha directly in your inbox.

- Lightspeed: All things Solana.

- The Drop: Apps, games, memes and more.

- Supply Shock: Bitcoin, bitcoin, bitcoin.