Is Bitcoin Mining Still Profitable? The Economics Explained

Today, bitcoin mining is barely profitable. Costs are too high and rewards are too low for most miners.

bitcoin mining

- Public miners sold more than 100% of their production in May, with many citing debt servicing and increased expenses

- Bitcoin miners are generally considered to be the most committed hodlers because their business model relies on bitcoin remaining an appreciating asset

Bitcoin’s bear market has put intense stress on mining profitability. Miners like Compass are being accused of failing to pay electricity bills. And On June 21, when bitcoin was trading close to $20,000, major mining company Bitfarm sold $82 million worth of bitcoin to bolster its balance sheet. And it wasn’t alone. Public miners sold more than 100% of their production in May, and many cited debt servicing and increased expenses as the reason why.

Even as bitcoin’s price has slumped from its all-time high of $69,000 in November 2021, the difficulty of mining the cryptocurrency has continued increasing. That’s because miners haven’t stopped or slowed down production — when the network increases total computing power, the protocol makes mining more difficult and thereby expensive.

At this unprofitability peak, some of bitcoin’s most bullish hodlers are selling bitcoin at a low to fund their mining efforts.

The big question is, why? Is bitcoin mining still a profitable venture, and what is the end game?

We sat down with Blockworks Editor David Canellis to get a better understanding.

How to measure bitcoin mining profitability

Bitcoin (BTC) is only profitable when mining costs are less than the value of BTC rewards and transaction fees. It sounds simple, but the mechanics of determining costs and the economics at play are less straightforward.

Because cost factors vary, it is better to evaluate miner behavior to analyze overall profitability. The fact that many miners are selling BTC at a low is a good indicator that costs are too high.

Bitcoin miners are generally considered to be the most committed hodlers because their business model relies on BTC remaining an appreciating asset. So when miners sell, it is primarily to cover costs. In an ideal scenario, they sell during bull cycles and accumulate in a bear.

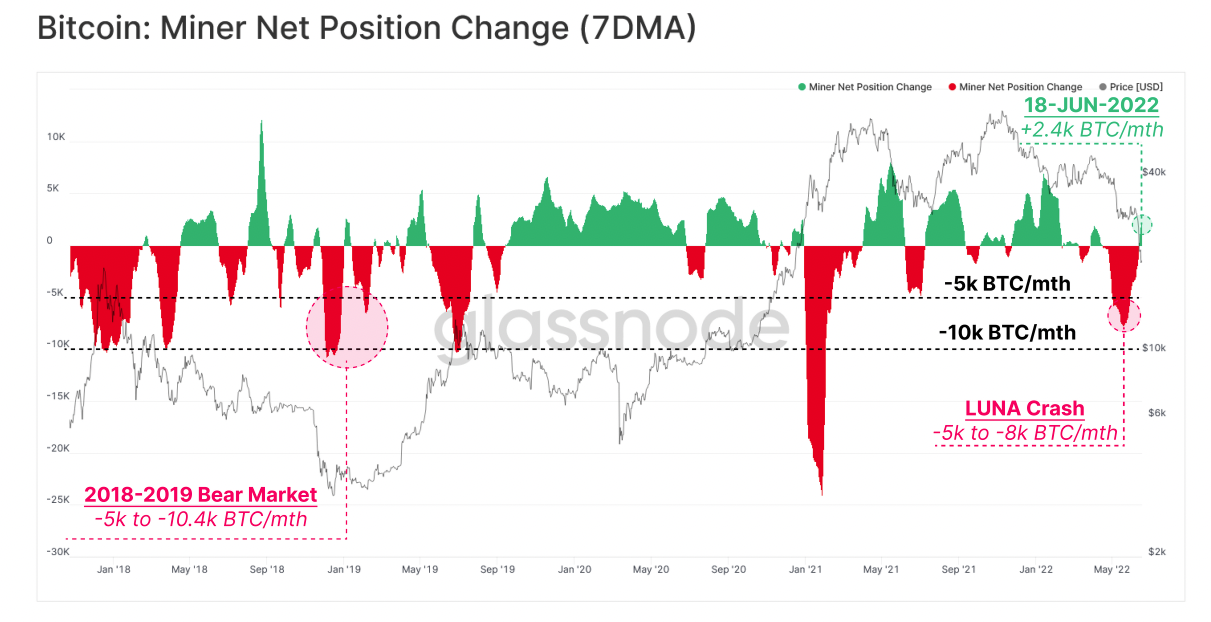

For example, miners took major profits when bitcoin was on its bull run during the winter and spring of 2021. The miner net position briefly dropped to an extreme low of -24,000 BTC per month — indicating that more BTC exited miners’ balance sheets than entered. When bitcoin price is in decline, miner net position is typically positive. This signals that miners don’t need to take BTC profits to cover expenses.

Source: Glassnode

Source: Glassnode

If miners sell during bear cycles as they did in June, it’s a sign that mounting costs forced miners to shift their business plans. But it isn’t necessarily a sign of capitulation — when miners go out of business, exit the network and sell their bitcoin. Instead of just shifting gears, capitulation is total surrender.

A war of attrition

This recent type of selling is a signal that miners are in a war of attrition. At this point in the cycle, they double down on mining efforts — even at a loss. They do everything they can to keep the lights on in the hope they will be among the last hodlers standing.

To understand how and when miners are forced to capitulate, we need to explain hash rate mechanics and its role in determining bitcoin mining costs.

Using hash rate to calculate bitcoin mining costs

When you read “bitcoin hash rate,” just think, “total computing power on the bitcoin network.” Technically, it is the number of calculations, or more specifically hash guesses, the network makes every second.

To understand how and why each computer is racing to guess each block hash, check out our explainer on proof-of-work vs. proof-of-stake protocols.

To understand mining economics, it is crucial to know that as more computers and mining capability enter the network, the protocol makes this guessing game more difficult. As a result, miners need to use more electricity to earn the same amount of rewards.

When computing capability leaves the network, the hash rate decreases along with the difficulty level. A lag often occurs because the network makes difficulty adjustments every two weeks. But the point is that miners can expend less energy for a similar amount of bitcoin when fewer machines are running.

Because hash rate correlates with miners’ energy use, it provides a rough indicator of total cost. Other variables, including location, scale, maintenance and upgrades, also play a part, but the second biggest variable is financing. Many mining institutions have interest payments and debt obligations they need to service on top of operating costs. So even if a calculator states that miners can make a profit at a specific bitcoin price, hash rate and kilowatt price, it doesn’t factor in loan servicing.

For deeper analysis into Bitcoin’s hash rate and financial news concerning public miners, check out our full report by Ryan Swanson on The State of Bitcoin Min(ing).

Leverage addiction and contagion risks

Many miners took out substantial loans during the last bull cycle to finance the expansion of their mining operations. Instead of spending bitcoin, they used their mining equipment and bitcoin rewards as collateral to acquire high-interest loans with as little as a 30% LTV (loan-to-value) ratio. Vera estimates that there is about $4 billion in this type of financing. Lenders such as Galaxy Digital, NYDIG, BlockFi, Celsius, Foundry Networks and recently underwater Babel Finance all accepted rigs as collateral in addition to cash down payments.

This type of financing adds pressure from two different directions. First, with much of their equipment locked as collateral, it is difficult for miners to scale production down when profitability is low. Second, the loan payments increase costs in a way that amplifies the unprofitability.

So if miners are struggling to service their loans, they could be forced to liquidate their bitcoin and hand over their machines to the lender. This would theoretically trigger miner capitulation.

And the loan agreements have contagion risks on both ends. The miners’ payment problems put pressure on lenders’ balance sheets, but miners also risk losing their deposited BTC collateral.

Miners who have borrowed from these crypto lenders face another risk. Many of the lenders had exposure to Terra/Luna when it collapsed, and to Celsius and other companies that have faced liquidity crises. If any of these lenders claim bankruptcy, miners could lose their deposited collateral.

The fragility of some lenders’ balance sheets means they also need the miners to stay in business so they can continue making loan payments. But by keeping unprofitable miners in business, some speculate this act is effectively keeping the Bitcoin hash rate artificially high, meaning the cost of mining bitcoin does not drop to an affordable level.

What do miners gain from being the last hodler standing?

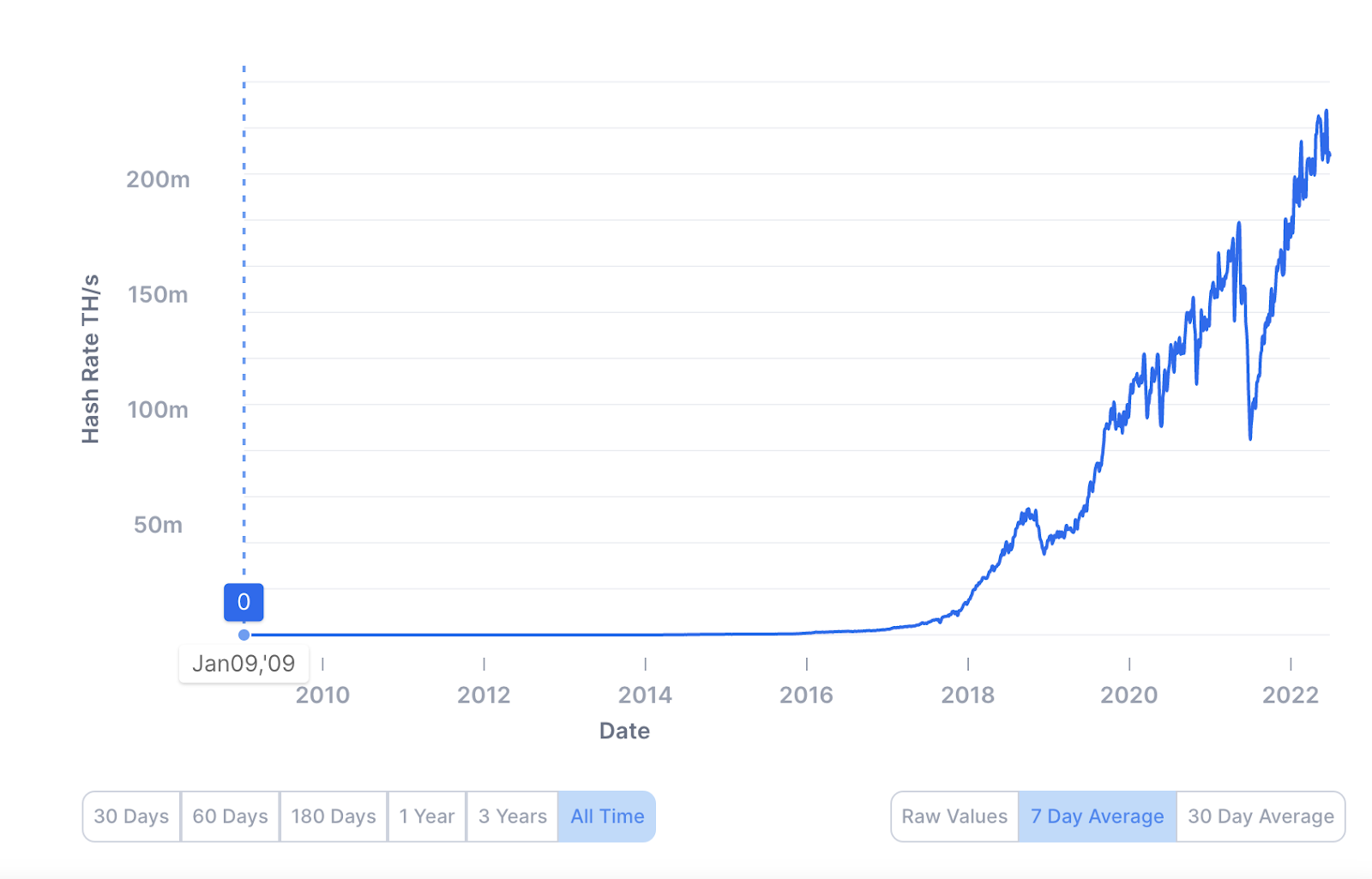

Despite unusually heavy bitcoin selling from miners in May and June, the hash rate reached an all-time high of 266 million terahashes per second on June 7, according to Blockchain.com, and is just over 208 million at the time of writing.

Source: Blockchain.com

Source: Blockchain.com

We have yet to see a major capitulation and hash rate decline like the one that occurred from November 2018 to January 2019. But mere survival isn’t the only incentive keeping miners in an unprofitable position. The players still in the fight hope to acquire a larger share of mining rewards once less efficient or overleveraged participants are out of the game.

Most miners share rewards with a mining pool that distributes revenue based on the hash rate contribution of each participant. This structure makes mining revenue predictable but also increases competition. Miners must continue adding hash rate to maintain and increase their revenue share.

Because the total bitcoin reward is roughly the same every 10 minutes, miners that survive a shakeout get a larger cut. And if you believe that bitcoin is fundamentally an appreciating asset, that extra share of the pie has a multiplayer effect. Miners who remain in the game not only regain a profitable balance sheet, they gain more bitcoin at a discounted price.

[stock_market_widget type=”accordion” template=”chart” color=”#7523CD” assets=”BTC-USD” start_expanded=”true” display_currency_symbol=”true” api=”yf” chart_range=”1mo” chart_interval=”1d”]

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.