How inflation breakevens signal eroding Fed independence

As the Trump administration continues to test Fed independence, markets are beginning to react

Aha-Soft and Ruslan Lytvyn/Shutterstock and Adobe modified by Blockworks

This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

This morning, I had the good fortune of interviewing Jens Nordvig.

The interview will be out tomorrow, but I wanted to give a teaser around something incredibly important: Fed independence.

Nordvig is the founder of Exante Data and was previously managing director at Goldman Sachs, senior investment associate at Bridgewater, and head of fixed income research at Nomura.

At this point, everyone knows that President Trump doesn’t like Jerome Powell very much and thinks interest rates should be meaningfully lower.

Specifically, the lens of criticism has shifted from the traditional dual mandate of the Fed — stable prices and maximum employment — toward what fiscal authorities view as a more relevant mandate, managing the debt load of the US government. One of the key arguments being made is that the Fed should lower interest rates so that interest payments on US debt come lower, thereby lowering the fiscal deficit.

This subordination of monetary policy to fiscal priorities of debt load management is what I view as the more correct definition of fiscal dominance.

Fiscal authorities set policy, and monetary authorities are there simply to make it the least painful. Nothing more, nothing less.

The last time that this happened was in the 1940s, when the Fed formally employed yield-curve control to cap rates at certain levels and its primary purpose was to buy US debt and manage the debt load. This regime ended in earnest with the Fed Treasury accord of 1951, which reinstilled Fed independence. Ever since those accords, we’ve been in an era of monetary dominance.

We are now in the early innings of this transition.

The primary risk associated with dwindling Fed independence is the potential for inflation expectations to become unanchored. In simple words, this looks like inflation concerns being instilled in society and a common realization that the Fed cannot get a meaningful handle on those inflation expectations.

In practice, the traditional goal of central banks having a 2% target for inflation serves as a codified intention to prevent inflation expectations becoming unanchored.

Unfortunately, this slow but steady erosion of Fed independence by the Trump administration is already beginning to percolate into inflation expectations, and the risk of these becoming unanchored is increasing meaningfully.

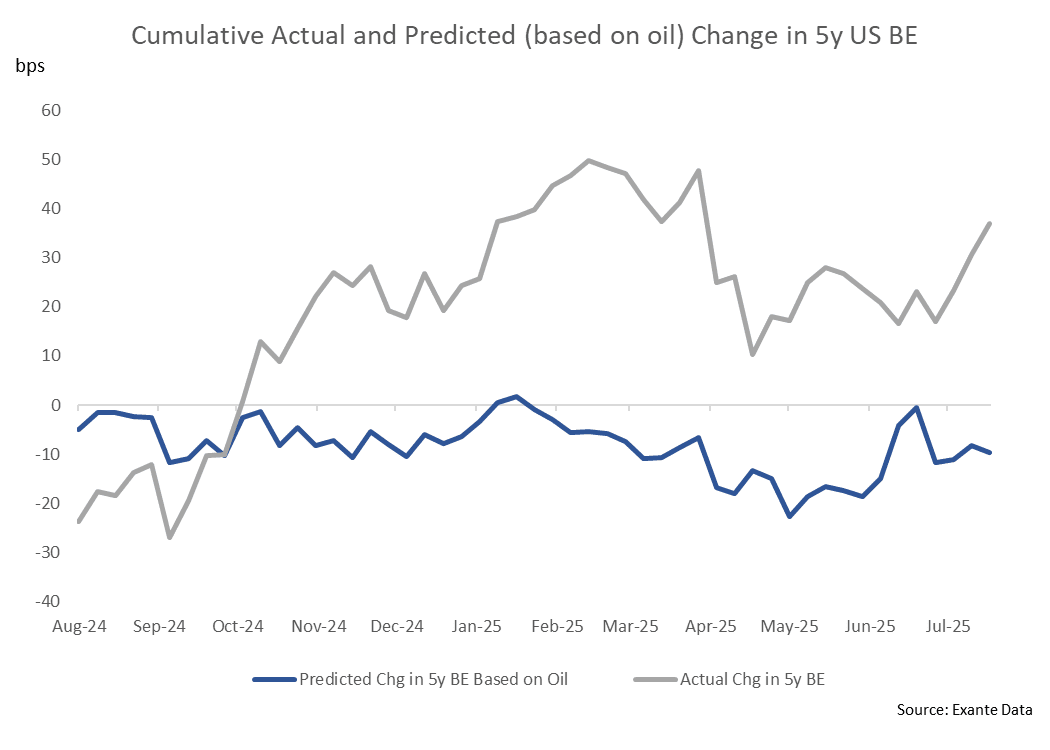

Jens brought a fascinating chart to our discussion that highlights this emerging dynamic.

The chart below shows the cumulative and predicted changes in five-year US breakeven rates, both as predicted by changes in oil and independent variables:

Typically, breakevens track the price of oil since it’s the largest driver of inflation. What’s concerning right now is that breakevens are surging while oil is hardly moving and, if anything, is declining.

In Jens’ view, this is a distillation of the market beginning to price-in, and become concerned with, inflation expectations becoming unanchored as Fed independence erodes.

With Powell’s term ending in the winter of 2026, keep an eye on this market and whether this concern accelerates. The bedrock of the financial system depends on these expectations remaining well-anchored.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.