On the Margin Newsletter: Are rate cuts bearish for risk assets?

Plus, a look into ETH ETF fees and a spicy exchange from this morning’s Senate Banking Committee hearing

Federal Reserve Chair Jerome Powell | Federalreserve/"Chair Powell participates in the Federal Open Market Committee (FOMC) press conference on July 27, 2022″ (CC license)

Today, enjoy the On the Margin newsletter on Blockworks.co. Tomorrow, get the news delivered directly to your inbox. Subscribe to the On the Margin newsletter.

Welcome to the On the Margin Newsletter, brought to you by Ben Strack, Casey Wagner and Felix Jauvin. Here’s what you’ll find in today’s edition:

- Everyone says they want rate cuts, but what could they mean for stocks?

- Crypto ETF “fee wars” make headlines, though the jury is out on how much investors actually care.

- Fed Chair Jerome Powell started his Congressional rounds this morning. Here’s how markets reacted.

Are rate cuts bearish?

A week never passes without seeing someone claim with absolute certainty that the FOMC cutting the Federal Funds Rate (FFR) is bearish for risk assets.

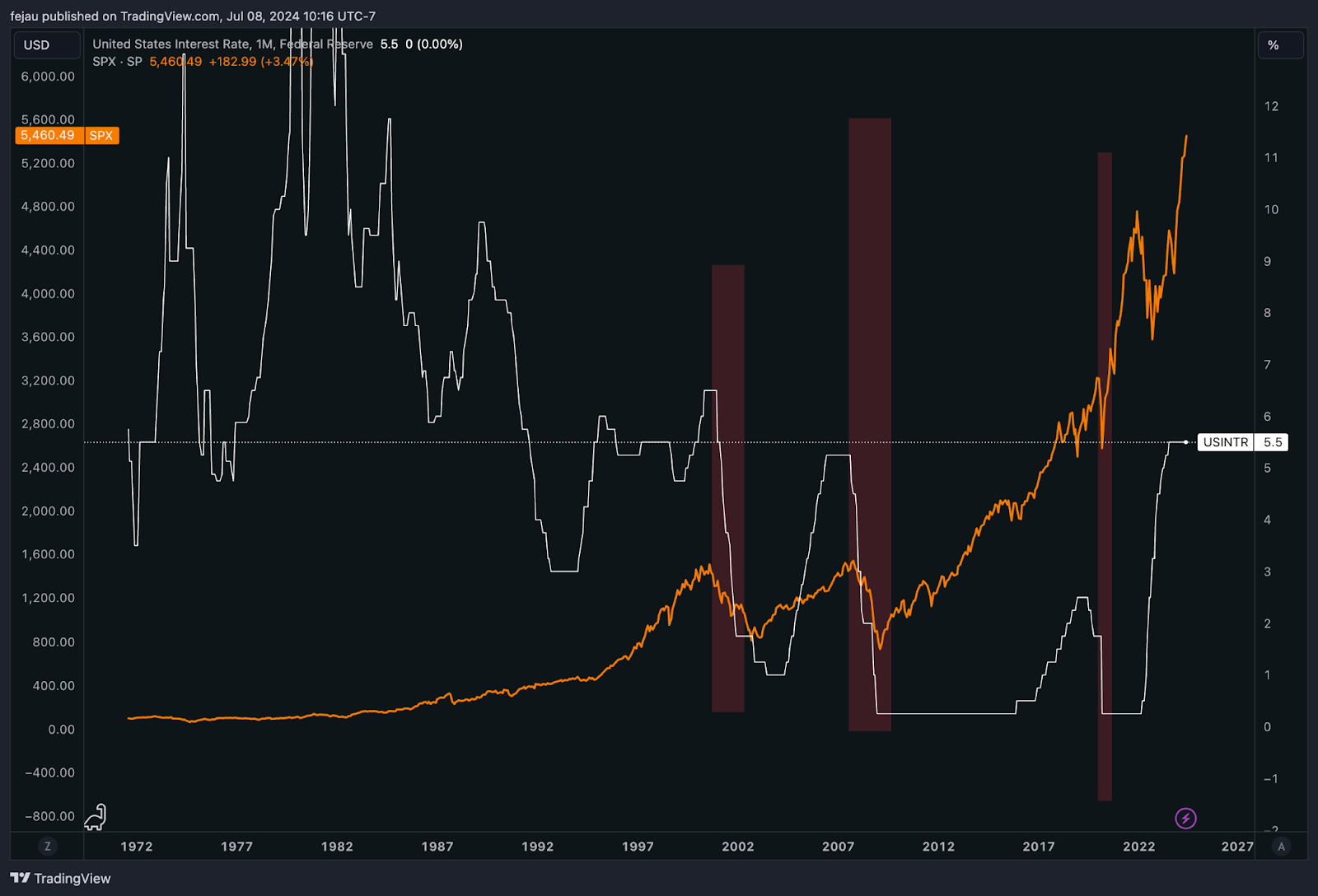

Driving that analysis is a simplistic look at comparing the price action of equities around the time the Fed starts cutting rates:

On the surface, it looks obvious! Clearly whenever the Fed starts a major cutting cycle, equities fall. Just look at the obvious dot com crash, 2008 financial crisis or the COVID crash as proof points, they say!

The validity of this answer is a lot more nuanced than what a quick skim of a chart might infer. At the core of understanding whether rate cuts are bearish for equities or not is the requirement to discern the two types of rate cuts that exist: the normalization cut versus the panic/recessionary cut.

Normalization cut

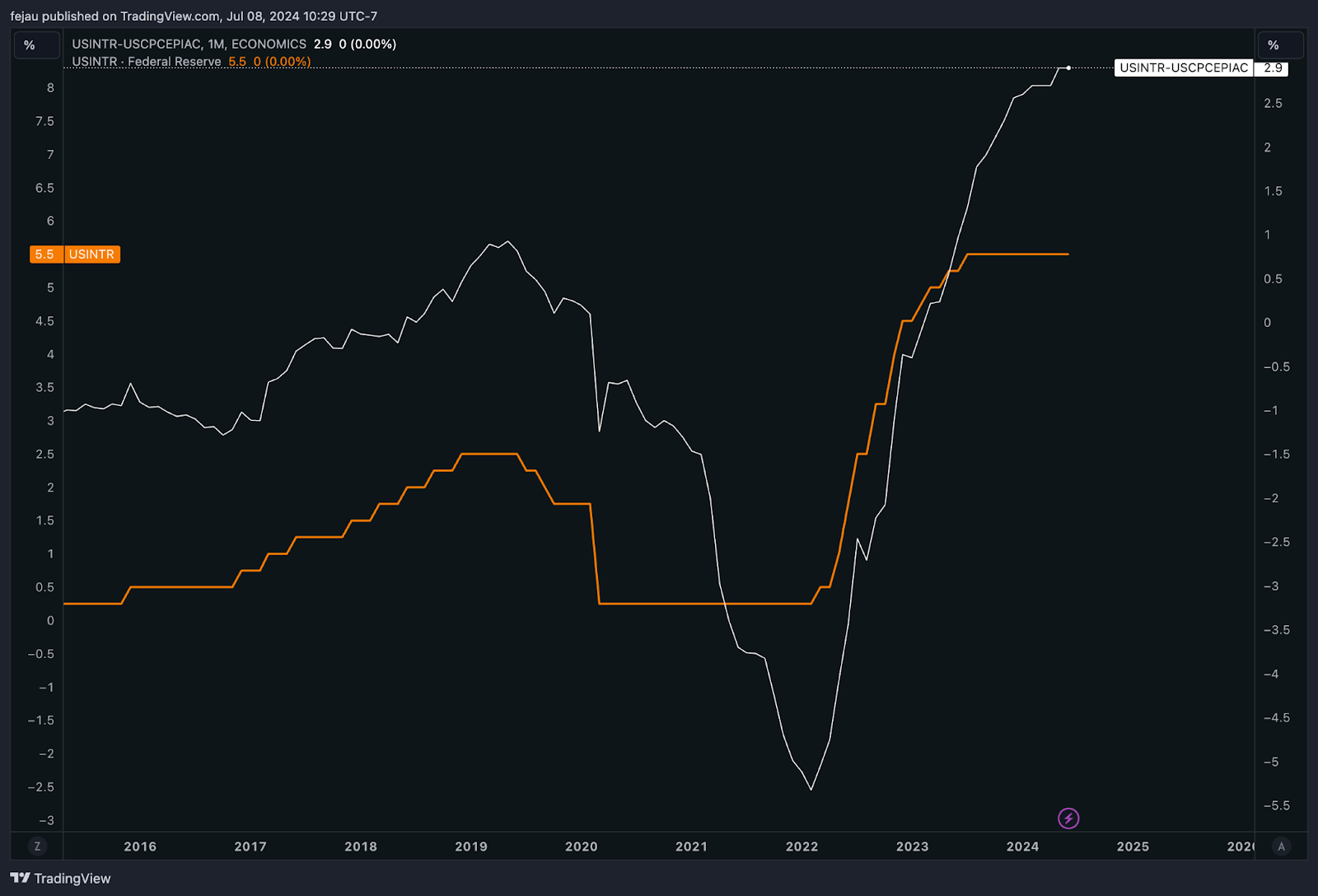

To understand what drives a “normalization” cut, you need to understand real rates. Real Federal FFR is the nominal FFR minus inflation. Since the Fed focuses on Core PCE, let’s use that as our inflation metric.

If we look at this chart, we see that despite FFR (orange) having been held flat for a year now, real FFR (white) has actually continued to increase, which is creating more tightening on the economy on a real basis. What gives?

Well, inflation has been on a steady decline for a while now. And since inflation is subtracted from nominal FFR to get real FFR, as inflation has declined, real rates have increased.

This dynamic means that for the Fed to sustain the same level of restrictiveness as a year ago, central bankers would need to cut rates to remain in line. This is a normalization cut and has nothing to do with cutting rates to ease financial conditions and stimulating the economy during a recession. The last time this occurred was in 2019 before COVID, when Chair Powell announced a “mid-cycle adjustment” rate cut.

Recessionary cut

This is the more well-understood and established type of rate cut where the FOMC quickly and aggressively cuts rates due to concerns about a recession or financial crisis. The 2008 great financial crisis and the 2020 COVID crash are clear examples of this.

Simply put, the Fed is trying to stimulate the economy to minimize the pain incurred from a recession. These types of cuts are often reactions to a crash that is already occurring and therefore often coincidentally bearish.

Panic cut

Finally, there are the panic cuts. These occur when an idiosyncratic event (typically of a geopolitical or financial stability nature) triggers the Fed to ease. During these instances, the economy is not necessarily contracting. Typically, a catalyst occurs that could pose recessionary and financial stability risks, which makes the Fed quickly and swiftly cut rates.

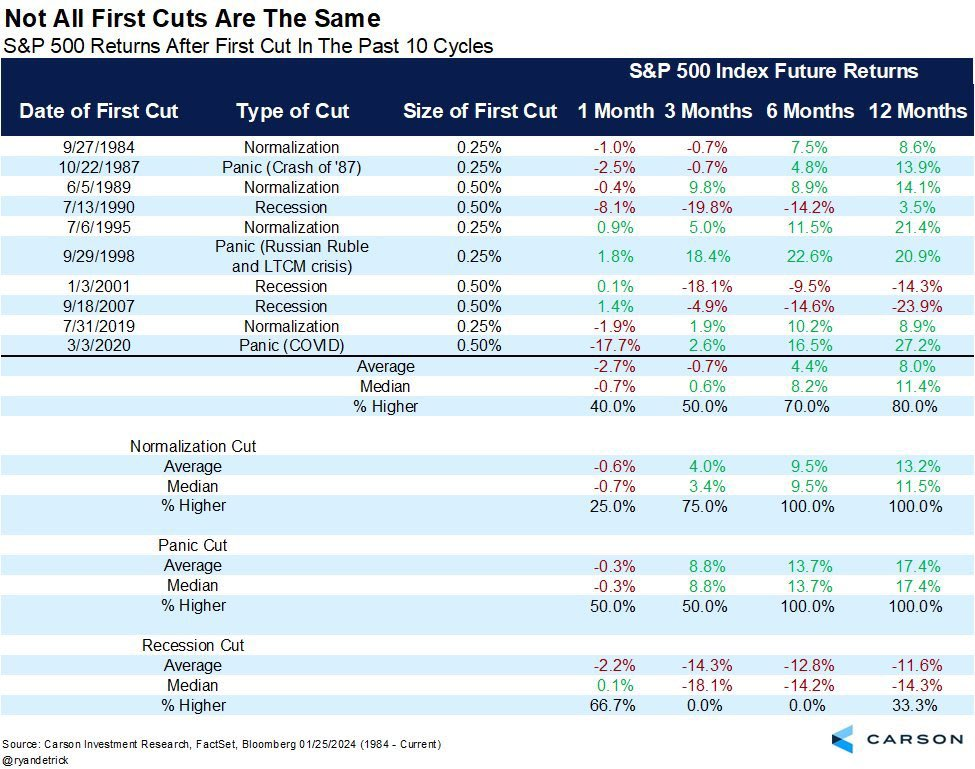

Empirical analysis of the different types of cuts and their subsequent impact on equity indexes is shown below:

Clearly, normalization cuts (and even panic cuts) are not bearish catalysts. Quite the opposite. It is only the recession cuts, where the Fed is trying to stave off a depression, that lead to lower equity prices.

As it stands today, the economy is slowing but still growing, with the Atlanta Fed forecasting a 1.5% real GDP growth rate for this quarter. Unemployment is increasing higher but is still secularly low at 4.1%. We are still far away from any sort of recessionary condition, which makes me believe that any potential upcoming rate cut will be a normalization cut, not a recessionary one.

— Felix Jauvin

233

The number of crypto asset companies (of 344 total) that have withdrawn applications to operate in the UK since 2020, according to data from the Financial Conduct Authority. That’s essentially two-thirds of them.

When it comes to crypto regulation, the Crypto Council for Innovation estimates the UK is at least 18 months behind the EU. As we wrote yesterday, the UK’s latest general election results could only delay further progress as the Labour Party establishes its priorities.

Will ETH ETF fees even matter?

Most of the revised ether ETF S-1s came in yesterday, as expected.

Members of the crypto/TradFi crowd on X (along with this reporter) were on alert, waiting to see if more issuers would share the planned price points.

I reported in my posts that…well…there wasn’t much to report.

Only the planned product jointly filed by Invesco and Galaxy revealed a fee we didn’t know about previously. The firms are set to charge a 0.25% sponsor fee — slightly higher than the 0.19% and 0.20% marks shared by Franklin Templeton and VanEck, respectively, in prior filings.

BlackRock, Fidelity, Grayscale and others chose to not yet show their cards. Those details will likely come in their finalized S-1s, expected very soon.

We watched the “fee war” take shape when US spot bitcoin ETFs launched in January. But now we question how much the fees actually matter.

ETF.com analyst Sumit Roy said distribution and brand name will matter more than small fee differences. A larger difference — such as 10 or 20 basis points — would likely have more of an impact on investor choice, he added.

“BlackRock and Fidelity have huge advantages, which they will exploit, but there is room for smaller issuers like Bitwise to gain a foothold in the space as well with low fees and unique angles,” Roy told Blockworks.

The lowest US spot bitcoin ETF fee — excluding initial fee waivers — was Franklin Templeton’s, at 0.19%. The firm undercut Bitwise’s 0.20% fee a day after the funds launched.

But Franklin Templeton’s BTC fund has attracted just $345 million of net inflows after six months on the market. The Bitwise Bitcoin ETF (BITB) has brought in about $2.1 billion.

Funds by BlackRock and Fidelity lead flows in the category, with $17.9 billion and $9.4 billion, respectively. Both charge a slightly higher 0.25%.

The most expensive fund by far — the Grayscale Bitcoin Trust ETF (GBTC), at 1.5% — has endured nearly $18.6 billion of net outflows.

Industry watchers continue to monitor what Grayscale might charge for the “Mini” versions of GBTC and its Ethereum Trust (ETHE).

The bottom line: Price isn’t everything. And yet, we can’t help but want to know.

— Ben Strack

So, do banks regulate themselves?

Federal Reserve Chair Jerome Powell appeared before the Senate Banking Committee Tuesday morning to kick off his two-day Capitol Hill tour.

The hearing went as expected for the first 90 minutes or so, with lawmakers asking about progress on inflation and when central bankers would bring down interest rates. Powell, as usual, was vague about any timeline — reiterating that additional data would be needed before any policy changes.

“Today [I’m] not going to be sending any signals about the timing of any future actions,” Powell said.

The conversation got a bit spicier when Sen. Elizabeth Warren opted to put Powell in the hot seat for her allotted five minutes.

Here’s a snippet of their exchange:

Warren: Chair Powell, in the six and a half years since you said, ‘Trust the banks to regulate themselves,’ how many of the 10 biggest banks have put policies in place to delay annual bonuses for this broader group of critical employees whose risk-taking could endanger the bank?

Powell: I don’t know specifically. My guess is all of them.

Warren: You think 10 out of 10? The answer is zero out of 10.

Powell: I doubt that.

Warren: Well, go back and look, because we’ve looked at their statements on this.

The two then got into it over whether or not Powell actually said, “Let the banks regulate themselves.” (Spoiler: Powell thinks he was taken out of context.)

The Fed maintains that big bank capital reserve requirement rules should not increase much, Powell reiterated. The original proposal issued last July suggested requirements increase to 20% of invested assets.

Despite the fireworks, equities and cryptos alike seemed content with the hearing overall — at least at first. Bitcoin and ether gained as much as 5% each during the first couple hours, while the S&P 500 and Nasdaq Composite indexes posted early gains of roughly 0.4%.

Everything slipped later in the session, although bitcoin and ether were able to maintain some momentum. The crypto assets were up 2.2% and 2.4%, respectively, at 2 pm ET (from 24 hours prior).

The S&P 500 and Nasdaq were also up slightly — inching 0.1% and 0.08% higher, respectively, at that time.

— Casey Wagner

Bulletin Board

- Crypto got a mention in the GOP’s 2024 platform documents released Monday. “Republicans will end Democrats’ unlawful and unAmerican Crypto crackdown and oppose the creation of a [CBDC],” it states. While crypto-related legislation has gained some bipartisan support recently, more Republican Congress members have historically voiced support for the sector (at least publicly.)

- Cboe on Monday filed what are known as 19b-4 proposals for the solana ETFs previously planned by VanEck and 21Shares. This step prompts the SEC to acknowledge the filing by publishing it in the federal register, at which time a 240-day clock starts for the agency to rule on the products. March 2025 drama, anyone?

- Former Valkyrie Investments CEO Leah Wald is now the president and chief executive of Toronto-based crypto investment firm Cypherpunk Holdings. She seeks to drive innovation at the company by “expanding its investment portfolio,” she noted in a statement. Check blockworks.co for a Q&A with Wald about the new role and the broader crypto space.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.