The cutting cycle is dead. Long live the cutting cycle

A lot has changed in the six months since the Fed decided to cut rates

rarrarorro/Shutterstock modified by Blockworks

This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

A lot has changed in the six months since the Fed decided to cut rates.

If we rewind back to September, things looked very different:

- The unemployment rate was looking weak and had surged to 4.2%, triggering the Sahm rule and causing a cacophony of concerns that a recession was imminent.

- At the same time, inflation looked like it was close enough to the Fed’s 2% target that it could forego concerns about stable prices and hone in on supporting the labor market by beginning to cut the fed funds rate.

With this balance in mind, the Fed went ahead and cut 100 basis points in that time up until today:

During these months, it became easy to be complacent that we were set into an easing cycle and it was time to ride that wave.

However, coming back to the present day, the environment could not be more different. For all intents and purposes, the cutting cycle is over.

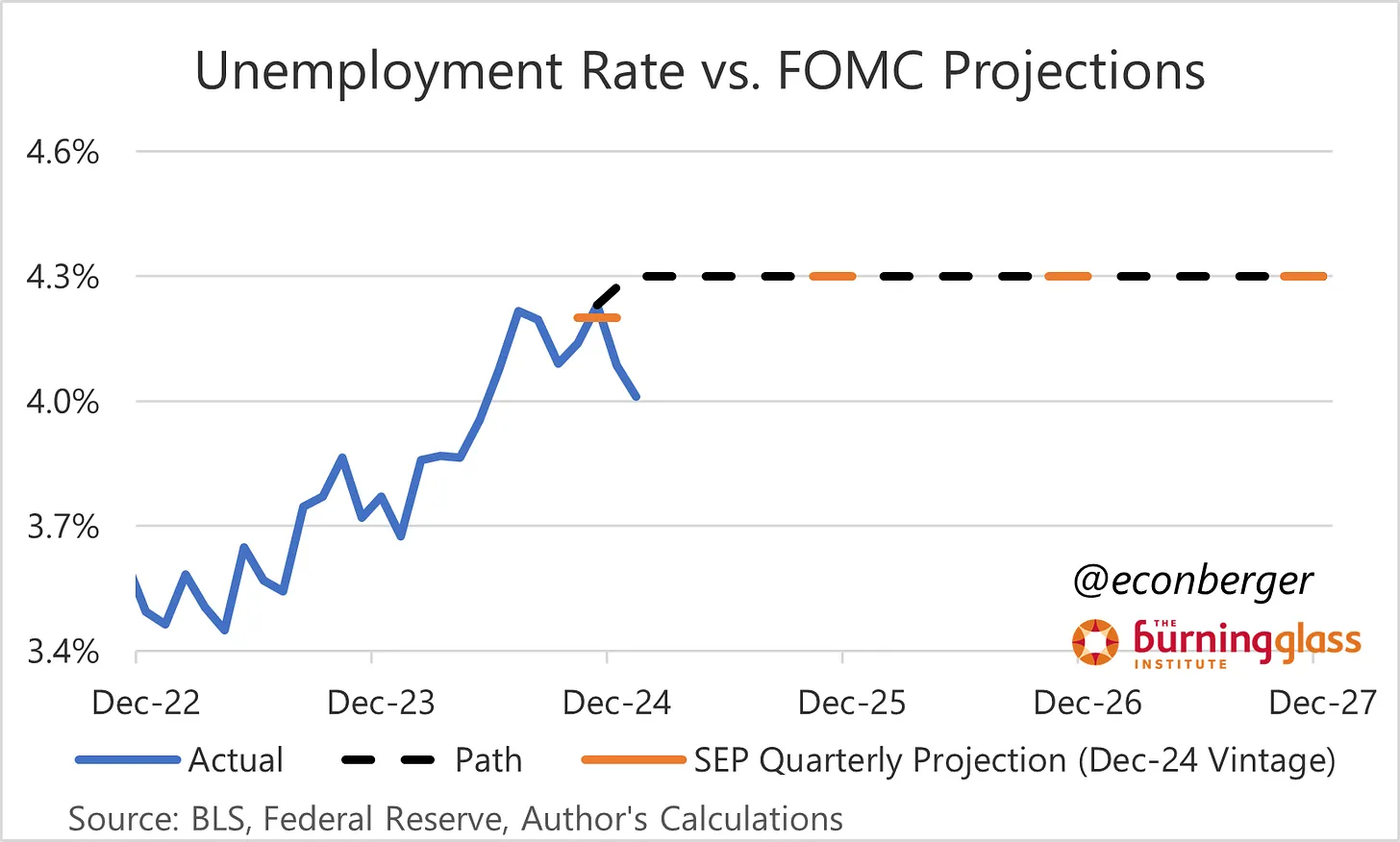

Looking at the labor market, it has improved significantly. Comparing the unemployment rate to the Fed’s forecast from only December, we can see that it has come down significantly.

Therefore, if one is looking to the employment side of the Fed’s dual mandate, there is no reason whatsoever for it to be easing at this juncture.

And so, the onus for any marginal easing from the Fed falls to the inflation side of the dual mandate.

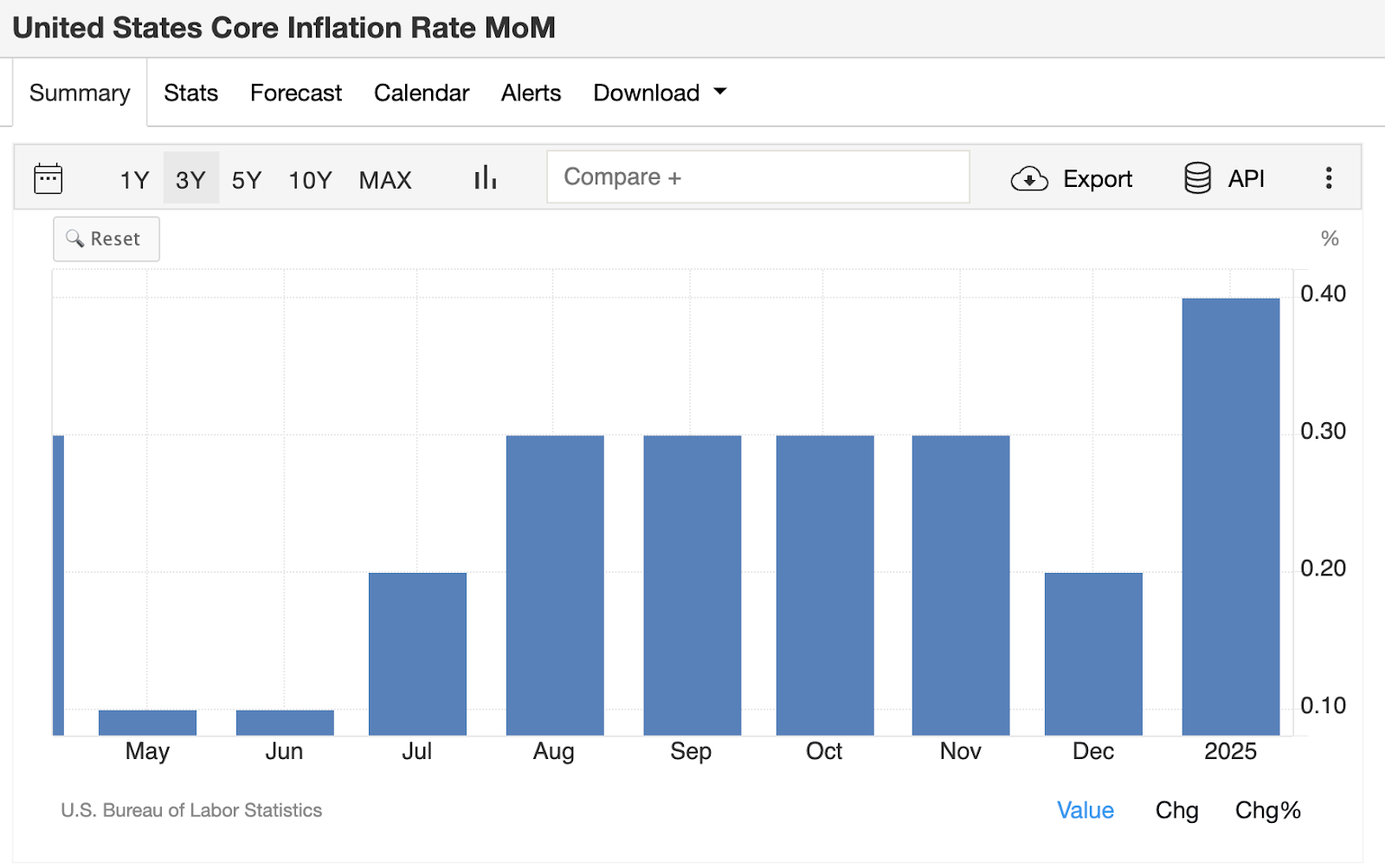

This week we received the CPI print for January, and it was a hot one by all accounts.

Core CPI came in at 0.4%, a notable jump higher from recent data.

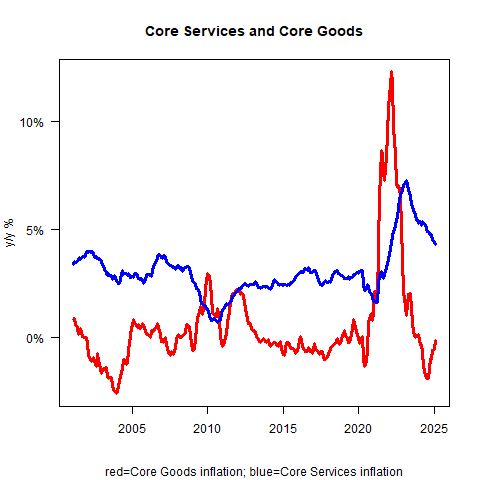

The theme of the inflation story over the last two years has been goods disinflating while services remain stubbornly high. As seen in the chart below, the major issue today is that goods are inflating again and services are refusing to take the baton of disinflation:

The simple takeaway from this granular data is that inflation is remaining above the Fed’s 2% target and bouncing around the 3-4% level. As long as this is occurring, there’s little reason for the Fed to cut rates when both sides of its dual mandate are seeing such strength.

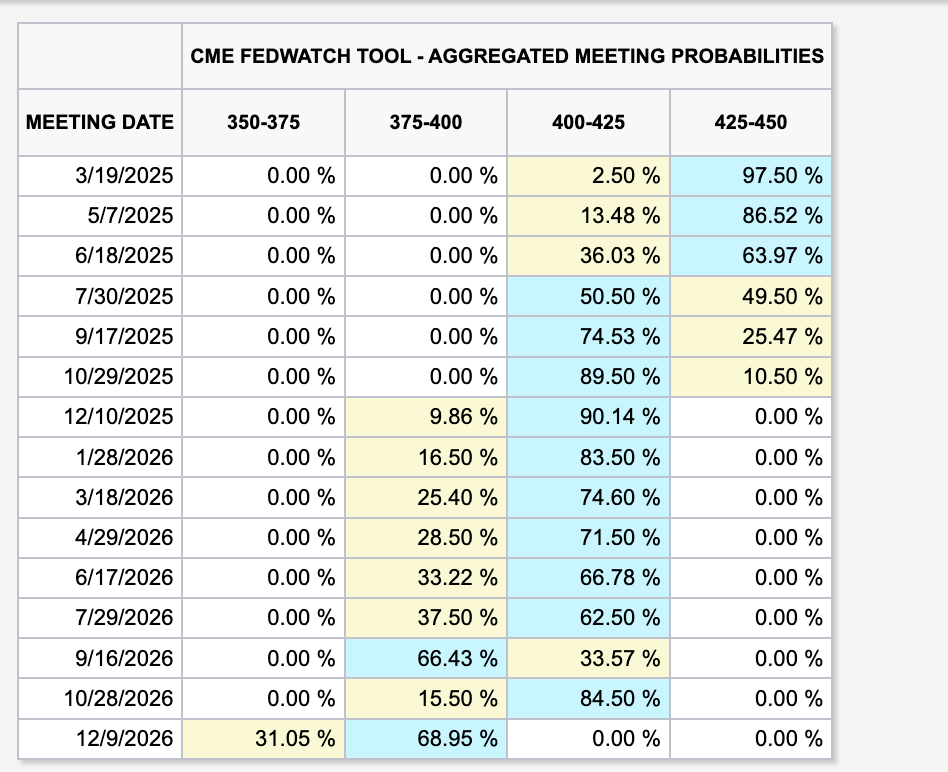

Putting it all together, we are now seeing a rate-cutting cycle that is seemingly over. As it stands today, the market has moved from expecting a rate cut in March to the end of this year instead:

If the data continues to come in above the Fed’s targets, it’s reasonable to think that these cuts will continue to get pushed out until they no longer exist.

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.